Opportunities in short-dated investment grade credit

January 2023

Marketing Material

First steps back into credit

As renaissance dawns for the fixed income market, short-dated investment grade bonds offer a good re-entry point into credit.

Written by

Ermira Marika

Head of Developed Markets Credit

Share this article

Bonds are back! After being starved for yield in the era of low interest rates and quantitative easing, the tide finally seems to be turning for fixed income investors. With central banks hiking rates to combat inflation, the resulting sell-off in bonds has seen valuations return to attractive levels. The aggregated Bloomberg Global Investment Grade Corporate Bond Index, for example, now yields over 5 per cent, hitting levels not seen since the global financial crisis.

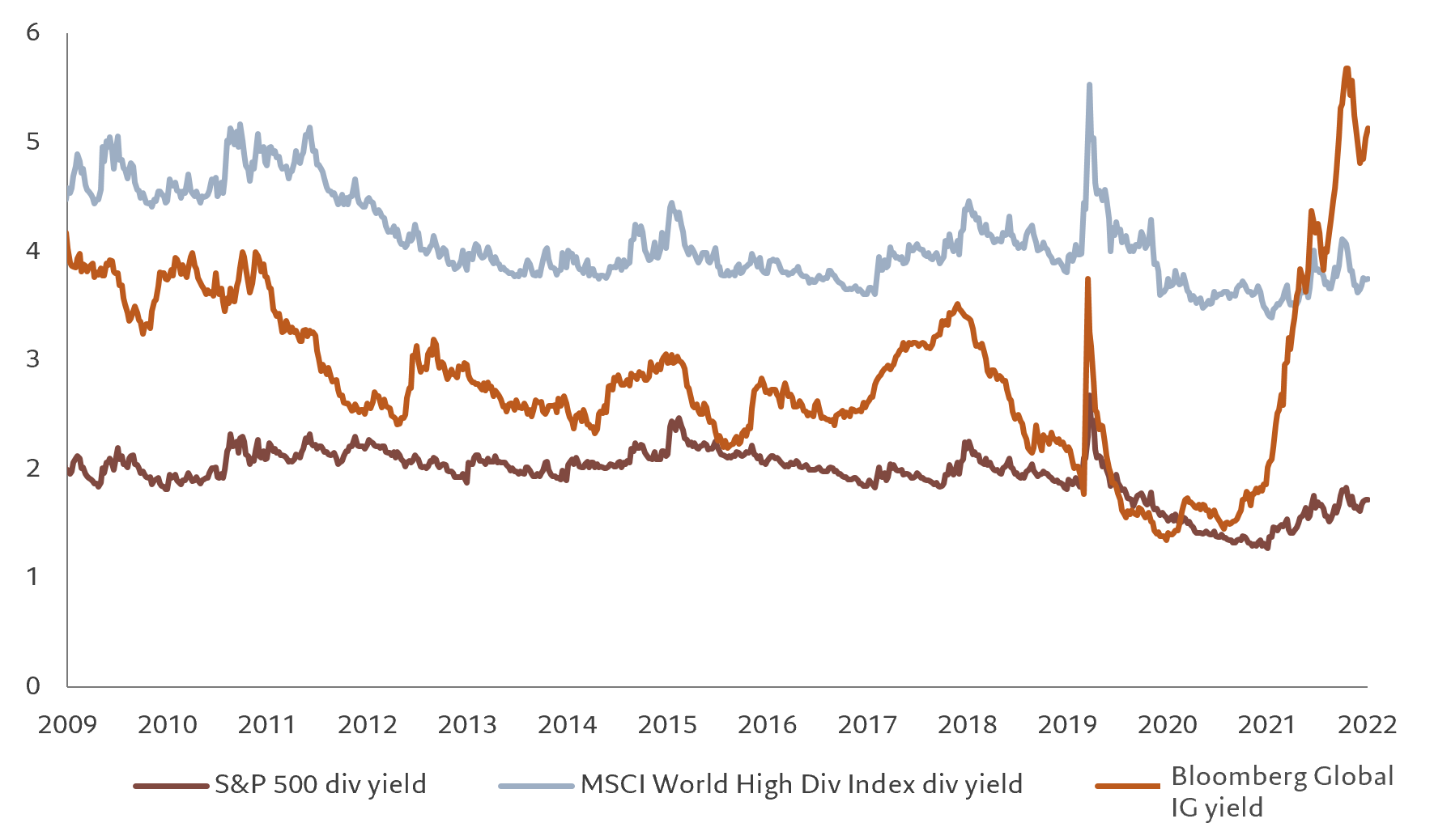

Consequently, investment grade bonds have also once again become competitive on a relative value basis, offering income that exceeds the pay outs from some of the world’s highest dividend-paying stocks (see Fig. 1).

Fig. 1 - "Income" is back in fixed income

Dividend yields versus bond yields, %

Source: ICE indices, Bloomberg, Pictet Asset Management. Data covering period 31.12.2009-31.12.2022.

But today’s complex macroeconomic and monetary backdrop requires prudence from capital allocators. Inflation could prove sticky, and it is not yet clear when the US Federal Reserve or the European Central Bank might call time on their monetary tightening campaigns. Furthermore, the global economy is still relatively weak, which could put pressure on company fundamentals in the more stressed corners of the market, notably low-quality, CCC-rated high yield bonds.

Superior compensation

So where should investors go for their first steps back into corporate bonds? One area where yields offer superior compensation against risks is developed markets short-dated credit.

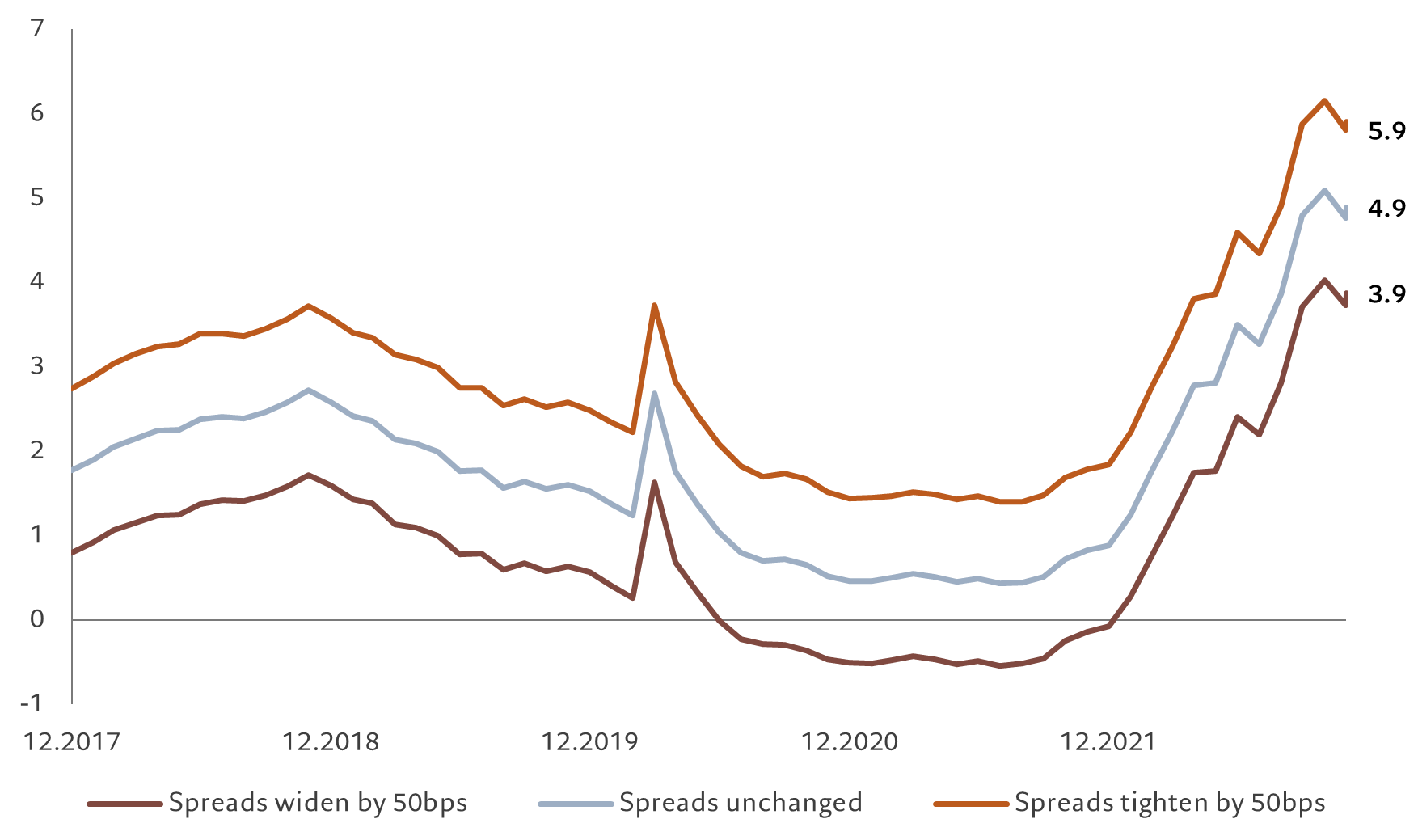

Fig. 2 - Flattening curves

Spread between 10+ year and 1-3 year EUR IG bonds, bps

Source: ICE indices, Bloomberg, Pictet Asset Management. Data covering period 31.12.2012-31.12.2022.

Rising interest rates and tightening monetary conditions have resulted in the flattening – and in some segments the inversion – of investment grade yield curves.

That means investors can secure higher yields for shorter-dated maturities than for longer-dated ones, whilst reducing exposure to duration risk.1 This is crucial in a volatile and uncertain rate hiking cycle.

Although shorter-maturity high yield credit also exhibits attractive valuations, the potential for economic distress in the months ahead suggests investors should perhaps focus on high quality bonds and more defensive industry sectors.

Even within investment grade credit, there certainly is a case for avoiding the more cyclical sectors, such as retail. Defensiveness and a focus on quality are key to navigating today’s environment.

Spread protection

The investment case for 1-3 year investment grade bonds is all the more compelling as this segment is well-placed to deliver attractive returns even if spreads widen further thanks to elevated yields and a lower duration (see Fig. 3). Such resilience is particularly valuable in an uncertain monetary and macroeconomic environment.

Fig. 3 - Elevated yield plus low duration

Expected 1-year returns on global 1-3yr IG, %

Source: ICE indices, Bloomberg, Pictet Asset Management. Calculated using index yields and spread duration (G1BC Index). Data covering period 31.12.2017-31.12.2022.

Sovereign benefits

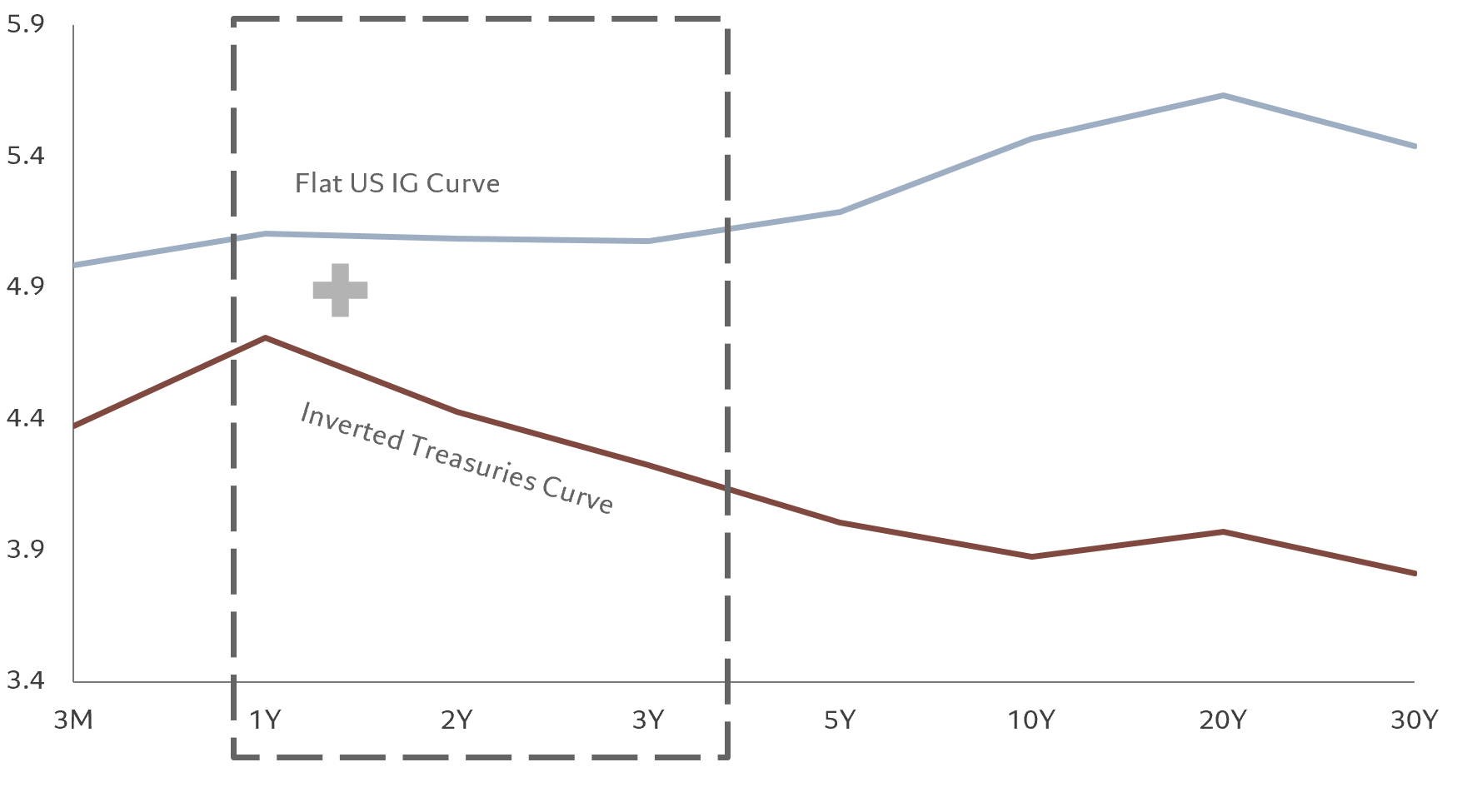

Value can also be found at the short end of sovereign curves. In the US, for example, 2-year Treasury bonds are yielding some 70 basis points more than their 10-year peers – a gap not seen for 40 years. Similar trends are in play in euro zone and Swiss government bond markets.

Fig. 4 - A blended approach

Yields versus maturity for US IG and Treasuries, %

Source: Bloomberg, Pictet Asset Management. Data as at 31.12.2022.

As credit investors, adding short-dated government bonds not only enhances diversification – and thus reduces risk – but crucially creates additional sources of return amidst inverted sovereign curves.

Adopting a blended credit-sovereign approach enables investors to lock in elevated yields whilst maintaining a lower duration. We believe this is an attractive risk/return proposition during this volatile phase of the credit cycle. Short-dated bonds can therefore act as the perfect starting point on the road back into credit.

Pictet's short mid-term bond strategies

Simple, short-dated, pure investment grade strategies with roughly 50/50 splits between government bonds and carefully selected corporate bonds.

Plain vanilla investment grade: no high yield, no hybrids, no subordinated debt, no emerging markets, no ABS or MBS.

Average duration typically around 1.5 years, with no positions in maturities of over 4 years. USD, EUR and CHF strategies.

Ermira Marika is the Head of the Developed Markets Credit at Pictet Asset Management since 2022. She has been working in Fixed Income for over 20 years.

Before her current position she was the Head of the CHF Bonds team since 2013.

Prior to that Ermira was a quantitative analyst in the Fixed Income team responsible for developing fixed income solutions.

She started her career at Pictet Asset Management as a quantitative analyst in equity strategies.

Prior to Pictet Asset Management, she gained experience in various companies including UBS and Morgan Stanley Capital.

Ermira Marika holds degrees in Business Administration and Economics and Finance from the University of Geneva and is a Chartered Alternative Investment Analyst (CAIA).

Ermira is member of the International Capital Market Association Regional Committee Switzerland and the Swiss Exchange Bond Index Commission.

Share this article

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user navigation and to collect statistical data. To refuse the use of cookies, change your settings or for more information, please click on the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.