Asset allocation: better than feared?

It’s early days, but so far 2023 is shaping up better than predicted even a few weeks ago.

US inflation has clearly peaked, the European economy is proving more resilient than some had feared, energy price dynamics are benign and the re-opening of China’s economy has progressed at a pace that has exceeded even the most optimistic expectations.

Clouds are clearly starting to lift, but we believe it’s too soon to make a decisive move into equities – after all, valuations are not particularly cheap, corporate earnings are stagnant and global growth is tepid at best. Also, the all important US consumer is not out of the woods yet.

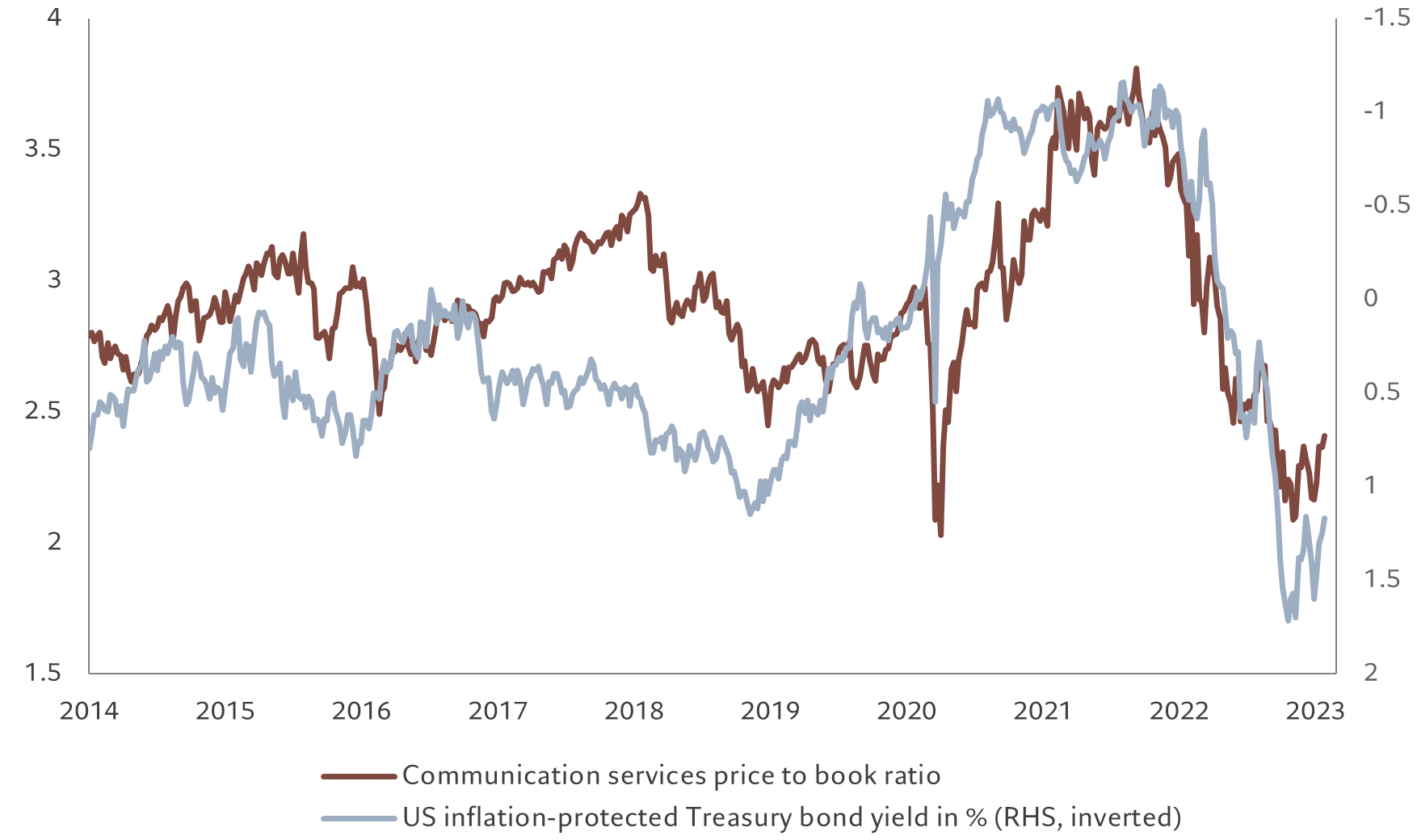

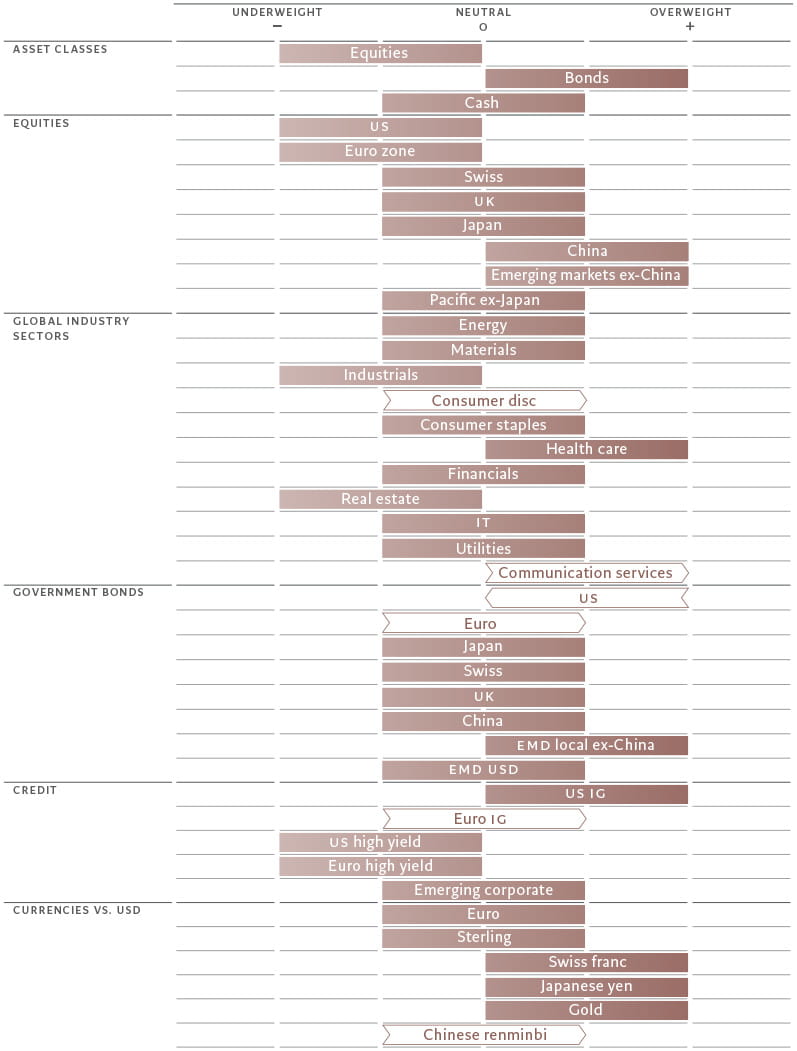

We therefore retain an overall underweight stance on equities and an overweight position in bonds, while tactically increasing exposure to sectors such as communication services.

Our business cycle indicators remain negative for the world economy as a whole, but the picture is less gloomy than it was a month ago. The outlook for China has turned positive, with the economy expected to benefit from an increase in consumption. As the country emerges from its Covid-induced lockdowns, there is some RMB5 trillion (USD740 billion) of excess household savings that can potentially be spent.

That will have wider repercussions through increased goods trade, a pick-up in Chinese tourism and higher demand for commodities, particularly base metals. The key beneficiaries from China’s economic revival include Hong Kong, Singapore, Korea, Vietnam and Taiwan, as well as Japan and Australia.

Crucially, we don’t expect China’s resurgence to feed global inflationary pressures, as was the case when US and Europe re-opened. The key differences between China’s re-opening and that of the developed world countries are that there were no fiscal transfers to Chinese consumers during the pandemic (in stark contrast to the cheques handed out in the US), global supply constraints have eased, the output gap in China is larger and the Chinese labour market shows no signs of wage pressure.

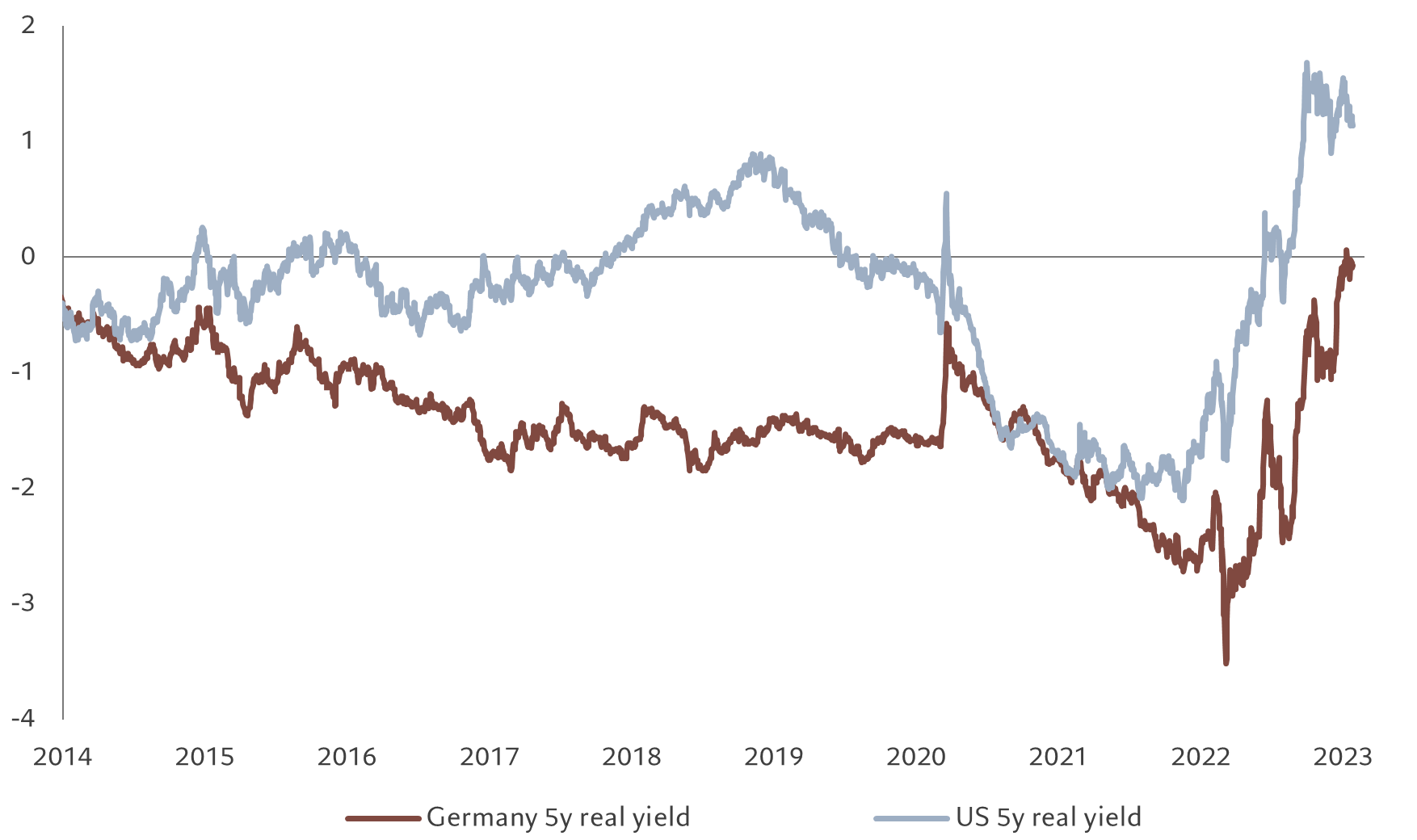

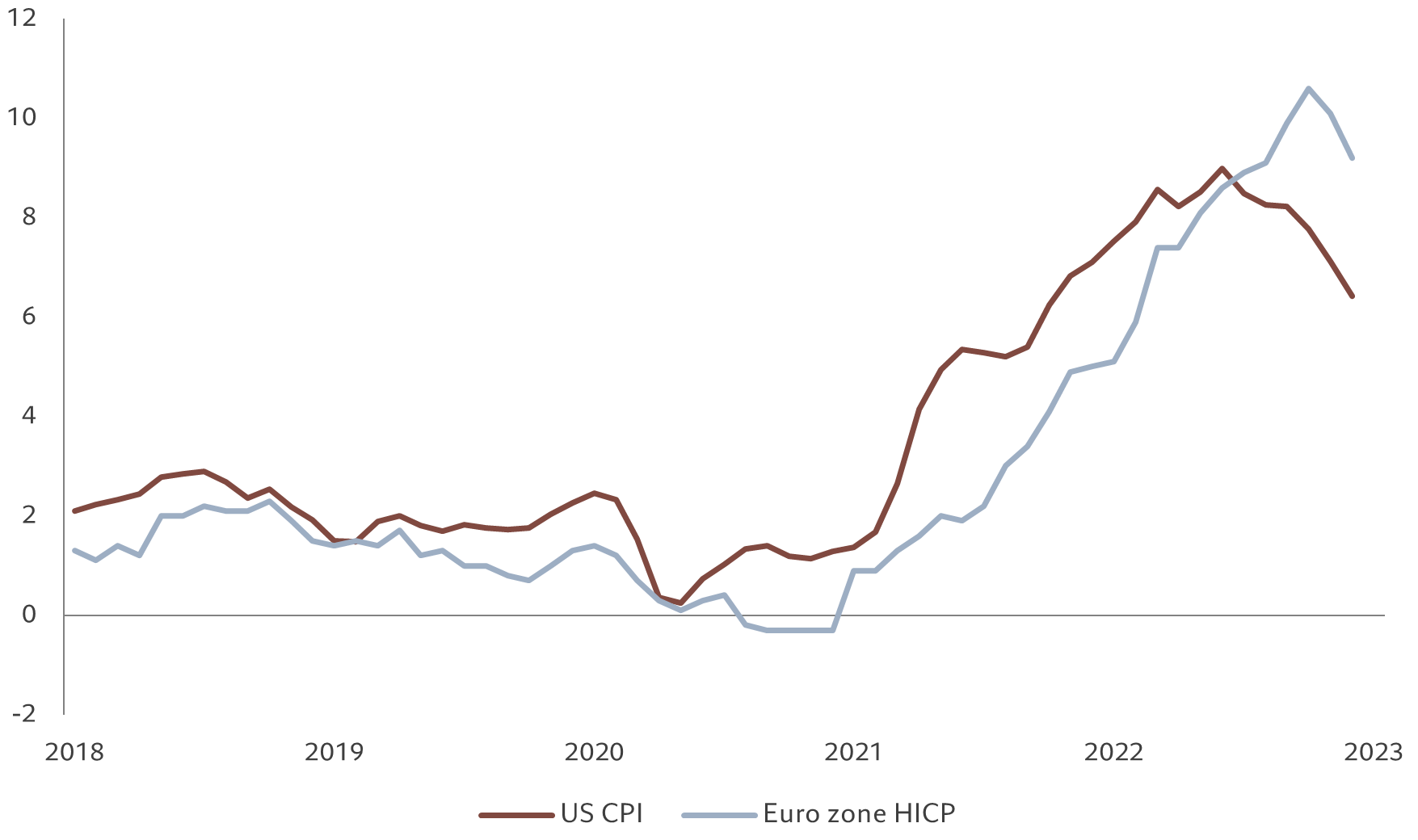

Our expectations for a worldwide moderation of price pressures have been reinforced by ever more proof that inflation in the US and Europe has peaked (see Fig. 2), which is good news for riskier assets. In Europe this has translated into a brighter economic outlook than previously expected, with the improving inflation dynamics boosting consumer confidence.

Source: Refinitiv DataStream, Pictet Asset Management. Data covering period 01.01.2018-31.12.2022.

Our liquidity scores show Europe having the tightest credit conditions of any major region.

Conversely, mixed US data has nudged up the probability of a recession on the other side of the Atlantic, although this is still not our base case scenario. Our model suggests the US Federal Reserve’s tightening is near completion, but easing is likely still a long way off due to fear of re-igniting inflation.

In the developing world, meanwhile, liquidity is ample, supporting our positive stance on emerging market assets.

Our valuation indicators flash green for emerging market equities too, with emerging Europe and Latin America looking particularly cheap.

More broadly, our valuation analysis suggests that any meaningful upside for equities will need to come from corporate earnings growth rather than an expansion in earnings multiples. Stocks’ price/earnings ratios have already increased as inflation has ebbed; they consequently exhibit no more upside over the next 12 months according to our fair-value model.

Yet, the picture for corporate earnings is similarly uninspiring: we expect global profits to be flat this year, with growth in emerging markets offset by a decline in Europe.

In the US, there are early signs that analysts’ downward earnings revisions are easing. However fourth quarter expectations are already very low, which means that companies that end up beating profit forecasts are unlikely to see analyst upgrades. Corporate guidance remains downbeat, with the pessimism shifting from margins to revenue. Until we see this situation improve, we are unlikely to raise our allocation to equities.

Technical indicators point to a rapid rebound in risk appetite. Weekly inflows into emerging market equity and bond funds hit a record high of USD13 billion, and there was also strong appetite for investment grade and high yield credit.

Implied volatility for equities fell to its lowest level in nearly a year, and demand surged for single stock call options. In contrast, sentiment on the dollar deteriorated.