Select your investor profile:

This content is only for the selected type of investor.

Individual investors?

Economic bumps shouldn't derail the recovery in global travel.

The travel and tourism industry has struggled with Covid, but they're reviving as the impact of the pandemic fades.

Written by

Pictet Thematic Advisory Board

The global travel industry’s post-Covid revival is unlikely to be derailed by an economic slowdown – though some corners of the market will fare better than others, according to the Pictet Premium Brands Advisory Board. So while businesses might turn more cautious in the near term, travel for leisure is likely to remain robust.

Pent-up demand from years of Covid travel restrictions, considerable savings built up during the same time and tight labour markets are all sustaining the travel industry, notwithstanding high inflation and rising official interest rates. Occupancy rates among a number of major hotel chains are already running above their pre-pandemic levels, with only Asia lagging behind. And there, Beijing’s decision to reverse its draconian zero-Covid policy should prove a boost to regional tourism, not least Thailand, as Chinese consumers dig into their considerable excess savings.

Although central banks are determined to clamp down on inflationary pressures, the resulting downturn is expected to be considerably more modest than prior recessions. This should help keep momentum going for leisure travel in particular.

The fact that hotels have been able to increase prices substantially underscores the strength of demand. Global hotel prices are expected to have risen 18.5 per cent in 2022 with a further 8.2 per cent to come in 2023, having dropped by more than a cumulative 20 per cent during 2020 and 20211. Rates are already above their 2019 levels in some areas and are expected to be so globally by 2023.

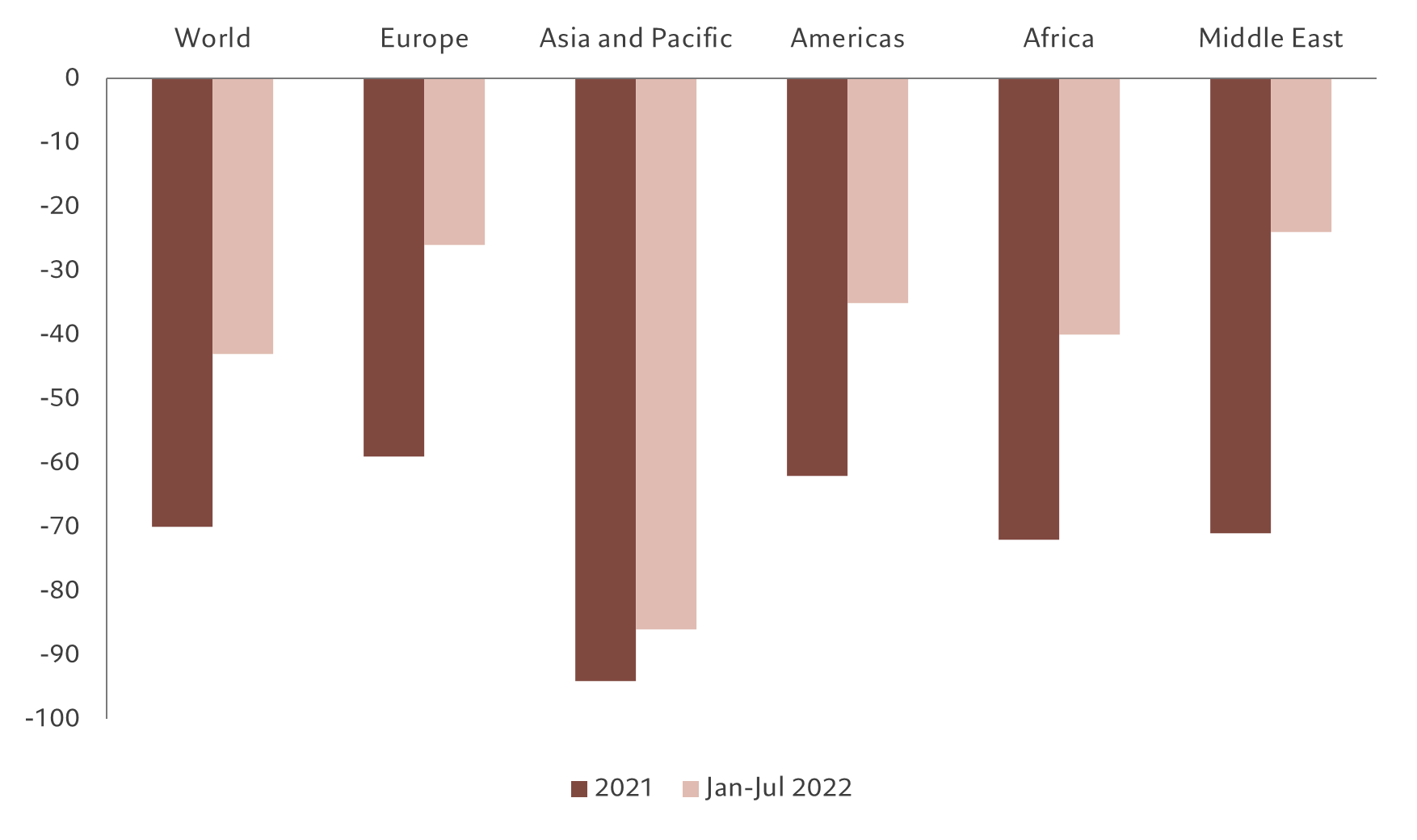

Rediscovering the world

International Tourist Arrivals vs 2019, % change

Demand may have rebounded strongly, but it has scope to rise further. Travel from the US to Europe more than trebled in the first half of 2022 on the same period a year earlier and remained strong through the year, though total numbers were still likely to have been only two-thirds of 2019 levels.

While leisure demand has been the key driver of the recovery in 2022, prospects for business travel longer term are positive – notwithstanding near-term risks associated with a possible economic slowdown. Some segments of business travel are doing particularly well. The meetings and events industry is experiencing an unprecedented recovery, and all signs point to a busy 2023. More meetings and events, more attendees, higher budgets, and higher rates are all expected.

Bringing staff together for training and team building is no longer optional with a dispersed workforce. Companies now recognise the vital role that in-person meetings play in strengthening culture, onboarding staff, increasing employee engagement and communicating corporate values and goals.

Events prices have increased in all regions across most categories of spend, fuelled by pent-up demand. The average cost-per-attendee in 2022 is expected to be around 25 per cent higher than 2019 levels and is likely to rise a further 7 per cent in 20232.

One of the major long-term forces affecting the travel industry is the development of sustainable, regenerative and socially responsible modes of transport. These, together with the rise in fuel prices will push travel brands into investing in cleaner technologies and fuels, including a move towards electric transport. New technologies are likely to include electric vertical take-off and landing, battery or hydrogen-powered fleets of aircraft, some of which will be unmanned. Innovators are looking to launch these vehicles commercially by the mid-2020s. So whatever the economy brings over the short-term, the travel and tourism industry’s longer-term prospects look positive.

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer. This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.