Emerging market assets perform well in an environment of rising inflation and strong growth, even when yields are going up and developed market economies are outperforming.

Written by

Patrick Zweifel

Chief Economist

Share this article

After emerging markets’ strong run over the past year, two big worries confront investors. First, the likelihood that over the next six quarters or so emerging economies look set to underperform their developed counterparts – a rare development in recent history. And second, that US Treasury yields seem poised to rise, a factor that can unsettle markets more generally.

Normally either of these factors might suggest that emerging markets’ (EM) fortunes are likely to turn. But not now. That’s because the economic environment looks set to stay very favourable for EM assets. And if history is a guide, EM equities and bonds should continue to perform exceptionally well.

Inflation is EM's friend

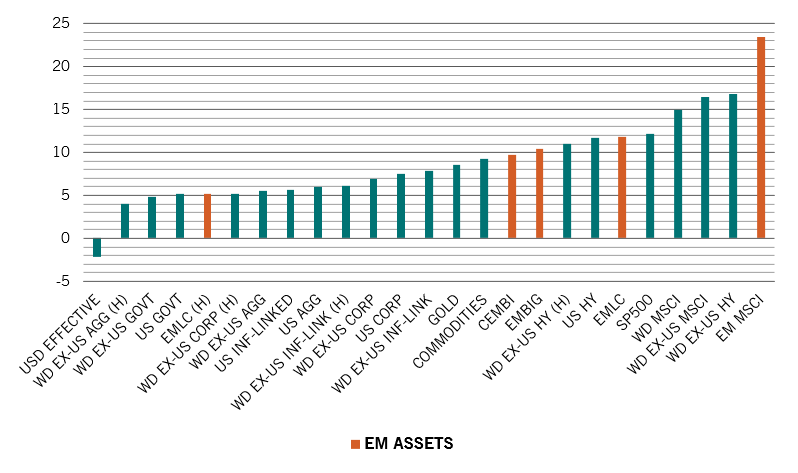

EM asset classes perform best in periods of high inflation and strong growth. Indeed, they’re among the best performing of all asset classes. In periods since 1950 when global inflation was above 2 per cent and rising and global GDP growth was above its four-year average, EM equities were significant outperformers in a list of 25 major asset classes, generating average annual returns of well above 20 per cent (see Fig. 1).

Fig. 1 - Boomtime winners

Average annual total returns by regions and assets in inflationary expansion, %

Source: Pictet Asset Management, CEIC, Refinitiv Datastream. Data for periods of above average global growth and high or rising inflation since 1950 to 01.04.2021.

That EM equity markets fared especially well in such an environment might not come as a surprise. But EM debt did too. Unhedged EM local currency bonds generated average annual returns of some 14 per cent, more than double what US Treasury bonds delivered and significantly above all other debt instruments apart from high yield credit, which tends to be more equity-like in terms of performance. And while EM dollar denominated sovereign debt lagged local’s performance, it still did better than developed market government bonds and investment grade credit.1

Our forecasts suggest the world is entering one of these favourable high inflation, strong growth environments in which emerging market assets flourish.

Inflating the world

Investors have grown so used to deflationary fears during the past decade that many seem unconvinced inflation could ever make a significant return. And yet all the signs are inflation could be about to return. Global CPI inflation climbed to 2.1 per cent in March from a trough of 1 per cent in November last year.

The world is entering one of these favourable high inflation, strong growth environments in which emerging assets flourish.

To be sure, most of the recent jump in prices was down to supply-side shocks – lockdowns have caused bottlenecks and lengthened delivery times, squeezing up the prices of commodities and other essential production inputs. But though some of these inflationary pressures will fade as economies are reopened, heavy doses of stimulus, not least in the US, will continue to support demand. Weighing the ultimate impact of these various effects is challenging, but, on balance, it seems increasingly likely that the era of low inflation has passed. In which case it makes sense to position against such a risk.

There is a worry, however, that the case for emerging markets might not be quite cut and died. That’s because over the coming quarters, developed market economies are set to outgrow emerging markets. At the same time, there is the risk of rising US Treasury bond yields – and since these represent the market’s risk-free rate, such a move would tend to portend ill for other assets.

A question of growth

It’s rare for developed markets to expand faster than emerging economies during periods of generally strong economic growth. But there was one such period in 2010, and in that instance both EM bonds and equities did well – local currency debt returned an annualized 12.7 per cent while the MSCI emerging market index generated a return of nearly 19 per cent, outperforming developed markets by more than 6 percentage points.

The more significant issue is whether emerging economies will continue to grow strongly, rather than whether or not developed markets do better. And here the data are positive. The four main drivers of emerging economy growth are all favourable: global trade is booming; as are commodities; China remains robust; and the dollar looks destined to weaken (which is also a plus).

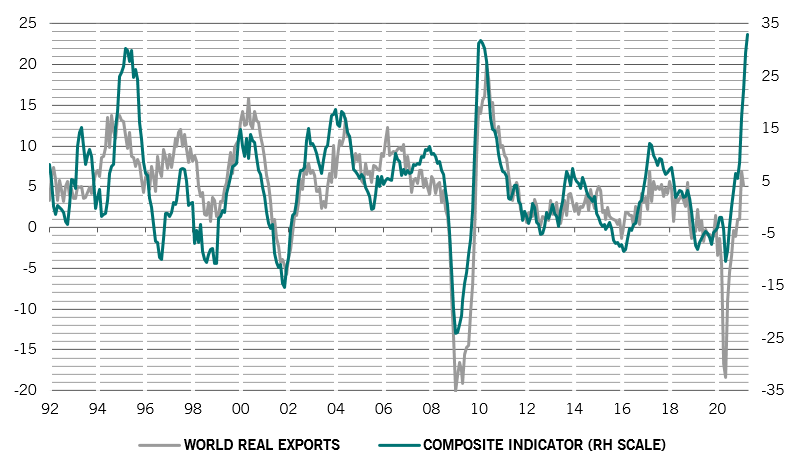

Fig. 2 - Growth's on the cards

World real exports and global trade indicator, year on year % change

Four world export indicators: Taiwan new export orders; Korea first 20 days exports; Baltic dry price index; world PMIs new export orders components. Source: Pictet Asset Management, CEIC, Refinitiv Datastream. Data from 01.01.1992 to 01.04.2021.

Real exports were already back to their long-term average in February, rising 5.2 per cent on the year – and this has almost entirely been an EM story. EM exports were up 17 per cent in the first two months of the year – those in developed markets actually shrank slightly – and are now 9 per cent above pre-pandemic levels (see Fig. 2). That trend looks set to continue. Our global trade indicator suggests this will be the strongest cycle in almost 30 years thanks to extraordinary levels of US fiscal stimulus, a boom in investment spending thanks to rising corporate profits and the fact that China’s recovery is becoming more domestically driven and therefore has triggered a jump in imports.

Global demand points to a double digit rise in commodity prices over the coming twelve months. President Joe Biden’s American Jobs Plan alone is expected to deliver some USD1.3 trillion in direct demand for commodities. What’s more, commodities are likely to benefit from their status as inflation hedges if the upward trend in consumer price remains sticky.

Meanwhile, although the pace of Chinese growth has peaked, the nature of its expansion should continue to be supportive of emerging economies generally. That’s because China has been shifting from last year’s exports-driven surge to being more domestically focused, which, in turn, should keep driving import demand – for example, imports of copper and iron are, respectively, 33 per cent and 78 per cent above trend.

And finally, we expect the dollar to weaken, giving a further boost to commodity prices and also reducing emerging borrowers’ debt servicing costs.

The risks of risk-free yield

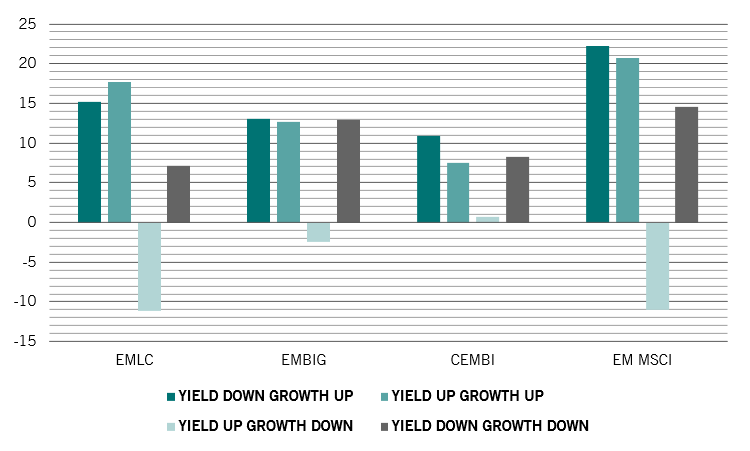

Strong US growth and higher inflation are likely to drive US Treasury bond yields higher, especially those with longer maturities. Investors worry that these rising yields will hurt risky assets everywhere. And historically they have often been damaging to EM assets – but only when growth in these countries is relatively weak or decelerating. That, however, is not the situation now.

Fig. 3 - Rising yields needn't hurt

EM asset class performance under different EM growth and US 10 year Treasury yield environments, median monthly annualised returns, %

Source: Pictet Asset Management, CEIC, Refinitiv Datastream. Data from 1950 to 01.04.2021

Typically, rising US yields would drive up the cost of borrowing for emerging economies, which then tends to hit their currencies. Eventually, this currency depreciation restores competitiveness and leads to higher exports, and thus stronger growth, which makes it easier for them to service their debt. This was the adjustment mechanism that was triggered in the wake of the 2013 US taper tantrum, when the US Federal Reserve’s decision to pare back its quantitative easing programme caused ructions across global markets. Which is why in past periods when rising US yields coincided with soft emerging market growth, EM assets tended to underperform by a significant amount.

This time, however, growth in emerging economies remains strong, which means there’s no reason for EM currencies to depreciate and thus cause a panic among foreign investors. In fact, historically, the best environment for EM assets was when emerging economies were generating strong growth at a time of rising US bond yields (see Fig. 3).

The currency question

EM currencies are no different from other EM assets in terms of how they perform in different economic environments. Weak growth at a time of rising US yields is associated with currency depreciation. Strong growth, even in an inflationary environment, leads to appreciation, particularly in the case of Asian and Latin American currencies.

In which case, currency developments during the taper tantrum is a poor guide for what’s likely to happen over the coming quarters. Then, growth was weakening and current account deficit countries in the emerging universe were hit hard – depreciating 18 per cent between January 2013 and February 2014. Now, the depreciation has been modest and mostly concentrated in the Turkish lira, which is subject to some special circumstances. At the same time, external financing needs of the biggest current account deficit countries is considerably smaller than it was then.

About

Patrick Zweifel

Patrick Zweifel joined Pictet in 1997. He is Chief Economist at Pictet Asset Management, having assumed the position in 2009. Before that, he was head of the “Macro Research Team” at Pictet Private Wealth Management, where he was responsible for emerging markets and Japan, and for the development of quantitative models on major asset classes. Before joining Pictet he was a research assistant in econometrics and monetary theory and worked on international research projects for the World Bank and the European Union. He holds a PhD in Econometrics from the University of Lausanne.

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user navigation and to collect statistical data. To refuse the use of cookies, change your settings or for more information, please click on the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.