In recent months, most major emerging market central banks have sharply cut their policy-rates to alleviate the negative economic shock of the pandemic. But is this sustainable and what can we expect going forward?

Written by

Nikolay Markov

Senior Economist

Share this article

Estimating equilibrium

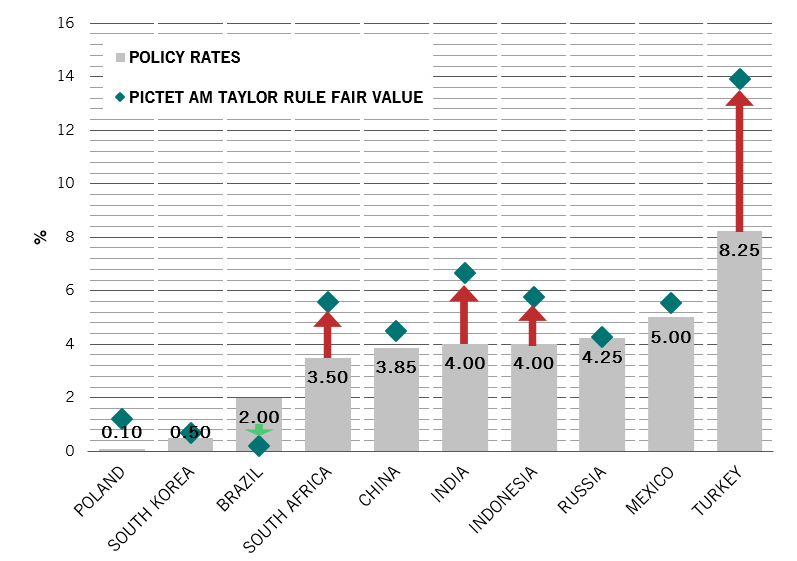

According to our proprietary calculations, four major EM central banks have cut their policy rates too aggressively: South Africa, India, Indonesia and, by some margin, Turkey.

That sinking feeling...

Fig.1 - Policy rates in select emerging market versus our fair value estimates of equilibrium using our proprietary Taylor Rule mode

Source: Pictet Asset Management, Refinitiv, CEIC, August 2020

Using our proprietary Taylor Rule model, we calculate the fair value for Turkey's policy rate as 14 per cent, not 8.25 per cent. This is based on the recent upsurge in inflation and domestic currency depreciation. By contrast, the Bank of Russia and Bank of Korea appear to have made appropriate policy responses.

What about the next 12 months?

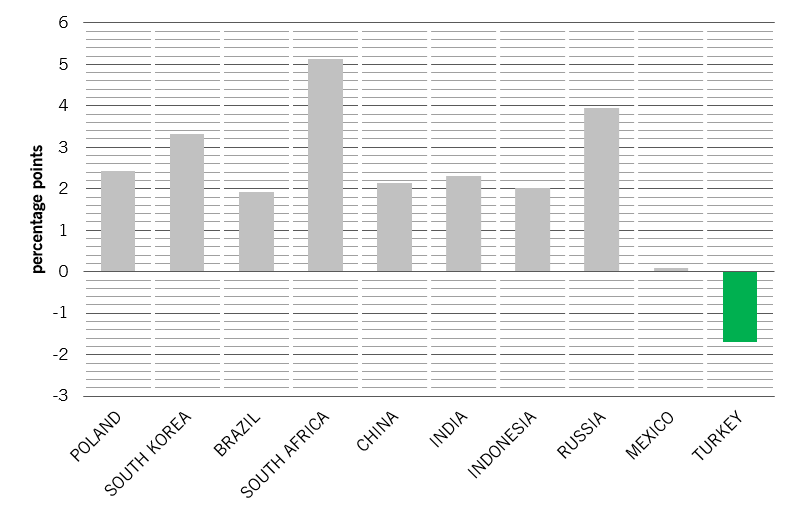

Fig.2 shows our expectations for policy-rate changes in the year ahead based on our fair value estimates. For most emerging markets the estimated policy-rate fair value is much higher in 2021. This shows that most central banks have no room to cut further and should gradually revert to higher rates as the economic shock of the pandemic subsides.

The road back...

Fig. 2 - Implied policy rate changes in 2021 based on our estimates of changes in fair value in 2021 and the actual policy rate in Q3 2020

Source: Pictet Asset Management, Refinitiv, CEIC, August 2020

The most striking cases are in South Korea, South Africa and Russia. While we think these markets have appropriately cut their policy rates during the outbreak, we believe they will need to start raising rates more quickly in 2021 as their economies are expected to rebound at a stronger pace.

For other central banks however, it might be appropriate to keep their monetary policies broadly unchanged in 2021. This is particularly true in Mexico.

Turkey is once again an interesting case as our model calls for significant rate cuts in 2021, in sharp contrast with the policy recommendation for the current quarter.

This is explained by the significant disinflationary process and expected gradual recovery in economic growth which should take place in the coming year if the authorities take the appropriate policy measures to stabilise the lira, thus avoiding a full-blown balance of payments crisis. If this positive scenario materialises, it should be positive for Turkish risky assets in the coming year. Bottom line: it will get worse before it gets better.

Time to look beyond rates?

But if the scope to move EM policy-rates is increasingly limited, what about unconventional monetary tools to stimulate the economies?

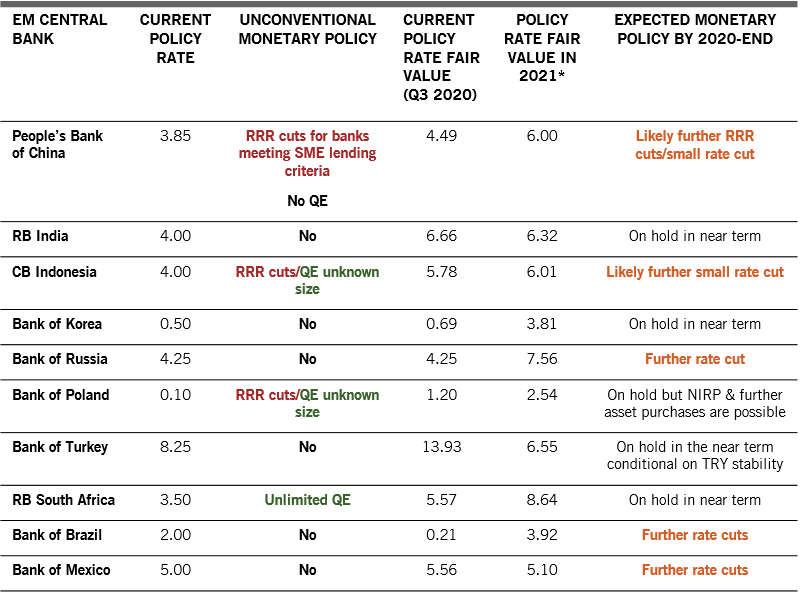

The table below shows that only the central banks of South Africa, Indonesia and Poland have opted for an asset purchase program (QE) of government bonds in the secondary market (and in the case of Indonesia possibly covering corporate bonds).

Most of the major EM central banks (China, India, Korea, Turkey, Russia, Brazil and Mexico) do not have a proper QE program yet. Still, those countries have introduced different refinancing facility schemes to provide ample liquidity to the interbank market thus supporting bank credit activity and the real economy.

The state of play

Fig. 3 - Our views on policy of select emerging market central banks

Source: Pictet Asset Management, Refinitiv, CEIC, August 2020. *Based on our Taylor Rule model.

Close to half of the major EM central banks are expected to ease monetary policy further in the coming months. This is the case in China, Indonesia, Russia, Brazil and Mexico, suggesting that market participants and possibly even the central banks themselves do not think they have actually run out of ammunition. But as suggested by our model, we believe further monetary policy easing will be very challenging in particular for South Africa and Russia, as well as for Turkey in the near term.

About

Nikolay Markov

Nikolay Markov joined Pictet Asset Management in 2013. He is a Senior Economist, Lead on CEE and Other advanced economies.

Before joining Pictet, he was working in the Monetary Policy Analysis Unit of the Swiss National Bank where he performed research on monetary policy rules for Switzerland. Prior to working at the Swiss National Bank he was a teaching and research assistant at the University of Geneva and participated in international academic conferences.

Nikolay holds a PhD in Economics from the University of Geneva and obtained a PhD program certificate from the Swiss National Bank doctoral institute in Gerzensee.

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user navigation and to collect statistical data. To refuse the use of cookies, change your settings or for more information, please click on the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.