KEY PILLARS OF PiCTET AM's THEMATIC EQUITY INVESTMENT APPROACH

November 2018

Marketing Material

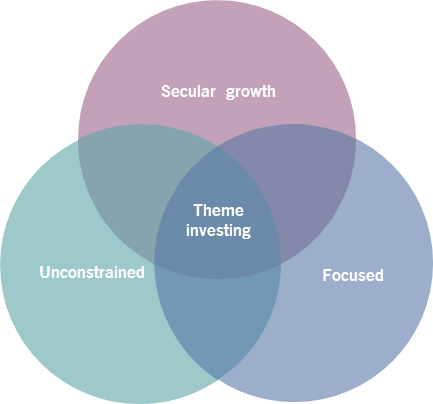

Our thematic DNA

We've built our thematic strategies on three investment pillars.

Written by

Gertjan Van Der Geer

Senior Investment Manager

Share this article

How we invest

What makes our thematic investment approach different is its combination of three key investment principles:

1. our emphasis on secular growth;

2. our focus and specialisation;

3. and our ability to manage portfolios in an unconstrained manner.

Fig 1: our thematic DNA

Source: Pictet Asset Management

1. Secular growth prospects

Thematic equity strategies aim to capitalise on megatrends, the profound changes in technology, the environment and society that are upending the world and will shape it for decades to come.

Examples include the digitisation of the economy, the rapid expansion of cities and the depletion of the Earth’s natural resources

At Pictet Asset Management, we believe these structural trends are a crucial source of long-run investment returns. That's why we use them as the basis for each of our thematic equity portfolios.

Megatrends matter to investors because they don't only disrupt industries, they also give rise to clear and predictable sources of value and profit growth.

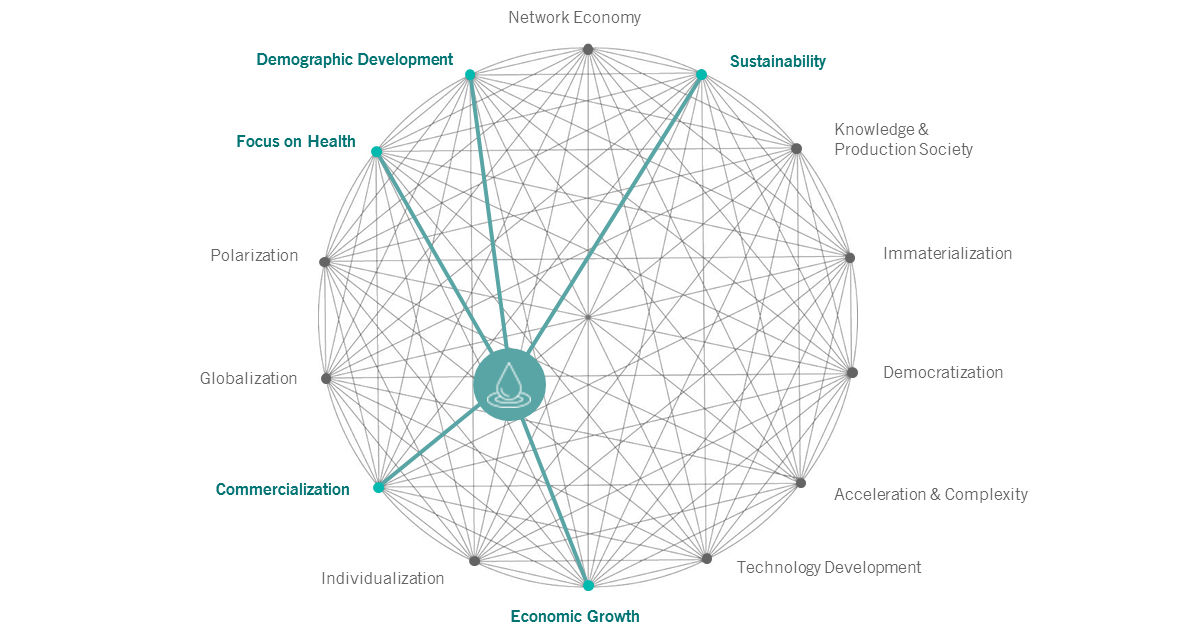

The changes underway in the water sector testify to this.

Fig 2: The Weight of water

As the diagram below shows the water theme is underpinned by 5 megatrends

Source: Pictet Asset Management

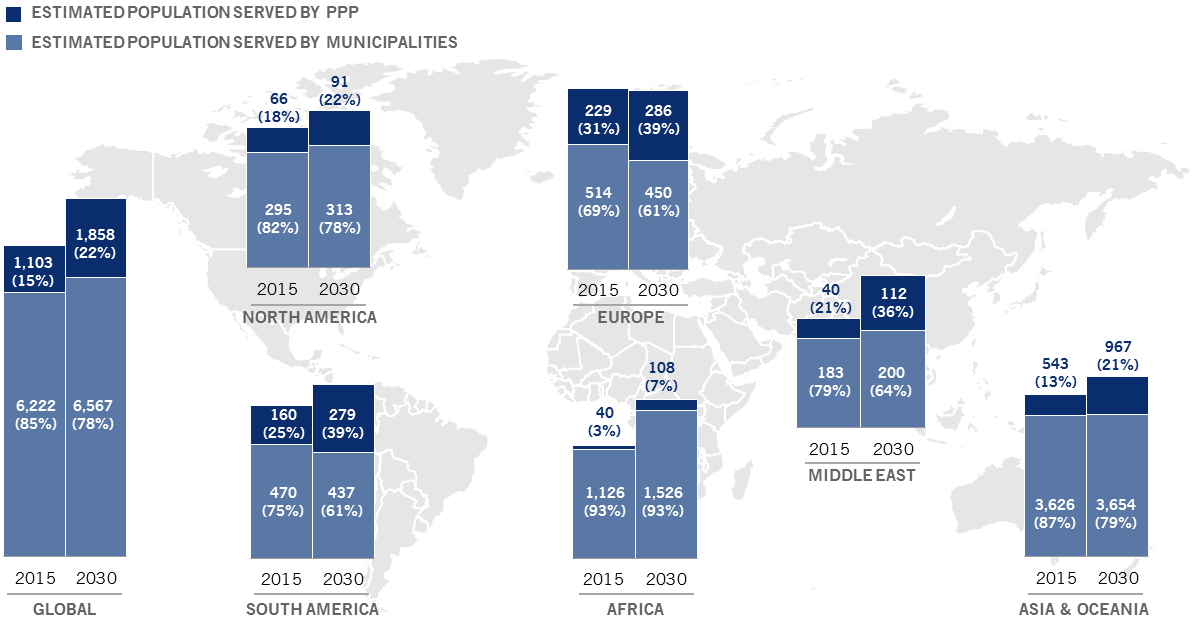

As Fig. 3 shows, the water sector is moving rapidly away from a public sector management model to one with ever greater private participation. This megatrend , which we describe as 'commercialisation' - is not just a US phenomenon; it's unfolding worldwide.

Being able to assess the long-term commercial effects of this megatrend was key to the development and management of our Pictet Water strategy.

Fig 3: The commercialisation of water

Growth in water public private partnership (PPP) across all regions

Source: Envisager 2015

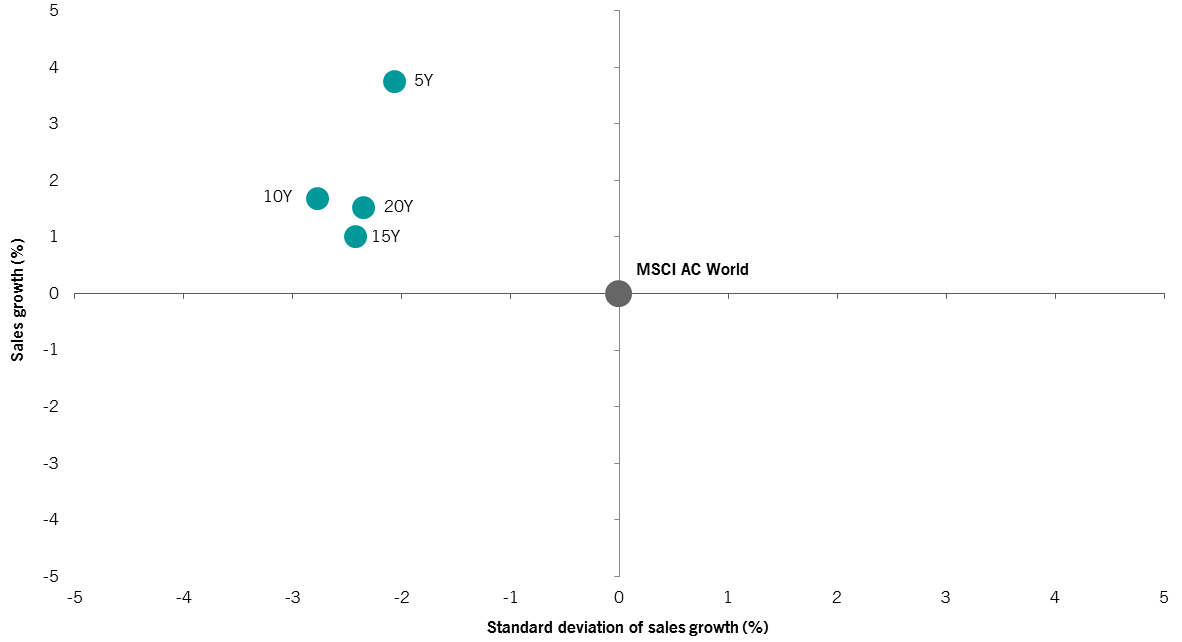

Secular growth makes it easier to predict growth and margins

The structural forces that underpin the thematic companies in which we invest make it easier to understand how they're likely to perform compared to the wider global equity universe.

The green dots in Fig. 4 show the sales growth of companies within our thematic universes to that of firms represented in the MSCI AC World Index over five, 10, 15 and 20 year periods. Companies in our thematic universes have experienced higher and more reliable (ie. less volatile) long-term sales growth than the market in general.

Paradoxically, and fortunately for us and our clients, the best thematic companies, those we target, often trade at a discount to their long-term potential. Indeed, we see evidence that the often short-term mindset of the wider market overestimates the rate at which the cash flows generated by thematic companies 'fade'.

Fig 4: Thematics over the long term

Source: Pictet Asset Management analysis based on backtest of our Global Megatrend Selection portfolio. Data to 31.12.2017.

2. Focus

Successful thematic investment demands several different levels of focus and specialisation.

To begin with, focus means being specialists in the themes and industries in which we invest. Being able to understand the evolution of the megatrends influencing the companies operating within a particular industry demands concentrated effort and years of experience. Which is why we are not generalists covering multiple sectors or themes. Some of us have been following certain stocks in our universe for over two decades. We know the management teams inside-out and have good access to them given the size of our holdings.

Second, the companies we build stakes in also have to be very focused - specialists in their chosen fields –which we measure using a proprietary gauge called "thematic purity”. Only companies whose activities predominantly lie within the scope of a particular theme/industry become candidates for investment: pure plays are always favoured over more diversified companies.

Portfolios made up of pure plays can be expected to do better than a portfolio that contains conglomerates.

In part, that's because a large body of research suggests specialist companies make for better long-term investments than larger, more diversified firms. This academic literature, which appears to have been overlooked in recent years, points to the existence of a “conglomerate discount” – i.e. that big firms are worth less than the sum of their parts.1

By extension, portfolios made up of pure-plays – firms that specialise in activities in which they have a distinctive competitive edge – can be expected to do better over time than a portfolio that contains conglomerates. And although mega cap companies are no longer called conglomerates, a large number of such firms pursue the same wide range of activities. Unsurprisingly our strategies are tilted towards smaller- and mid-cap companies. We believe therefore that our focus on purity is a tailwind for our equity strategies.

Focused investment teams with combined portfolio manager and analyst functions

Thirdly, our focus extends to how our investment teams are structured. Each team member is not only a portfolio manager, sharing responsibility for the management of the strategy, but is also a stock analyst. By dedicating all their attention to a clearly-defined universe of stocks, our investment managers develop distinctive, specialist expertise.

We believe this gives them an advantage over the typical active global equity team, which works rather differently. Most mainstream global equity funds are run by managers supported by several analysts, whose task it is to generate lists of their best ideas within their assigned sectors. The portfolio construction team then chooses stocks from among those recommendations.

A typical global equity manager tends to have to cover a very large universe of stocks and are thus less focused than analysts. This can make it very difficult for them to add value in the portfolio construction process, as successfully picking stocks from a list of analyst recommendations is difficult.

3. Unconstrained, forward looking portfolios

The third component of our investment DNA can be defined simply as taking an unconstrained or benchmark-agnostic approach. We devote ourselves to finding the best companies within our investment universes on a bottom-up basis. As long as companies meet our minimum liquidity requirements, we're not concerned which indices they sit in. We want a portfolio of companies that will do well in the future, whatever club they belong to.

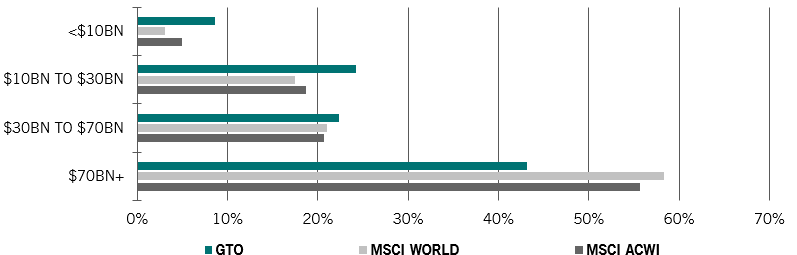

For example, as Fig. 5 shows, our Pictet Global Thematic Opportunities strategy has a greater allocation to small- and mid-cap stocks than either the MSCI World or MSCI AC World indices. This is purely a residual of our stock selection - our focus on firms that are specialists in their fields.

Fig 5: Dare to be different

Pictet Global Thematic Opportunities portfolio market cap breakdown vs global equity indices

Source: Pictet Asset Management, 30.09.2018

Low overlap with global equity indices

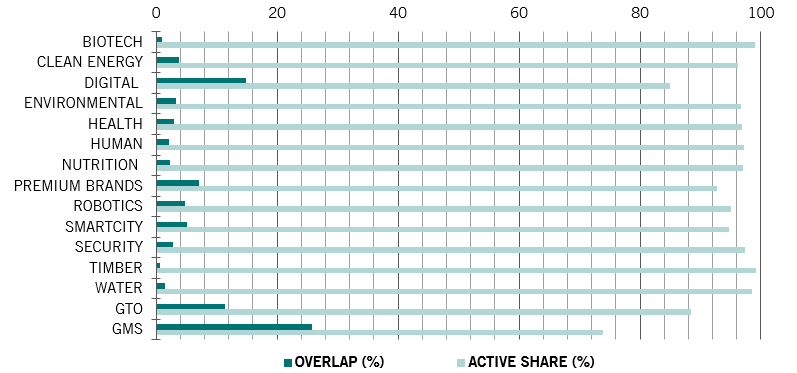

Further evidence of our unconstrained approach is in Fig. 6, which shows the active share and overlap with the MSCI World of all of our main thematic equity strategies.

Fig 6: Dare to be different - Part 2

Overlap and active share of Pictet thematic equity strategies versus MSCI World

Source: Pictet Asset Management, MSCI, Bloomberg, 31.08.2018. Overlap = sum of all overlapping fund holdings with index, adding up the min of the two weights

Written in our genes

That, then, is the 'DNA' of our thematic strategies: investment themes based on secular sources of growth; an investment approach centred on focus and thematic purity; and portfolios that are unconstrained and forward-looking.

Of course a thematic approach is not for every investor. It won't suit anyone with a shorter investment horizon. Nor for those investors who find it difficult to tolerate significant bouts of portfolio volatility as there are inevitably periods when thematic equities lag equity indices.

But for investors willing and able to escape the herd and take a longer-term view, we think a thematic approach offers highly attractive prospects.

Gertjan van der Geer joined Pictet Asset Management in 2008. He is Head of Thematic Solutions in the Thematic Equities team and a Senior Investment Manager responsible for the Global Thematic Opportunities strategy.

Before joining Pictet, Gertjan worked for two years at Robeco in Rotterdam as a senior portfolio manager for the Food & Agriculture strategy. Gertjan began his career in 2000 at Fortis MeesPierson as an asset manager in the Private Banking division.

Gertjan graduated with a degree in Business Economics and Financial Economics from the Free University of Amsterdam. He is a Certified European Financial Analyst (CEFA).

Share this article

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user navigation and to collect statistical data. To refuse the use of cookies, change your settings or for more information, please click on the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.