Select your investor profile:

This content is only for the selected type of investor.

Individual investors?

Dispatches from India: money à la Modi

India has bounced back from November's shock demonetisation part of a strategy to wean people off cash and cut corruption.

Written by

Venkatesh Sanjeevi

Senior Investment Manager

Last November, Narendra Modi triggered an economic earthquake in India. By suddenly making the country’s whole stock of 500 and 1,000 rupee banknotes worthless and giving people only a short period during which to convert them to new notes, India’s prime minister brought about the monetary equivalent of a seismic event. But as so often happens with natural disasters, once the shock of the initial upheavals and uncertainty had passed, Indians rallied and adapted to their new circumstances. India’s recovery has been much quicker than most pundits expected.

When I took my most recent trip to the country, last month, the economy seemed to have almost completely returned to normal. The data bear out my impressions. For instance, in December following the demonetisation, our leading economic indicator for India registered its largest monthly decline since 1987. But by February it had already normalised. Car sales showed a similar pattern. They slumped 18 per cent year-on-year in December but were then back up 0.9 per cent on the year in February. In retrospect it appears to have been a short, sharp shock, a bit like the slump that followed the global financial crisis, whose effects on India were equally transient.

Why the Indian economy is bouncing back so smartly is down to how demonetisation has and hasn’t worked.

One major reason to cancel bank notes was to undermine the black economy by destroying black market wealth. In theory, people who couldn’t justify where their money came from wouldn’t be able to convert old notes to new ones. Some 86 per cent of the USD253 billion of cash in the economy, or USD218 billion, was subject to demonetisation. With around a fifth to a quarter of that cash likely to represent black market proceeds, that would have been a significant potential destruction of wealth in the economy.

However, Modi’s government appears to have underestimated Indians’ ingeniousness in getting around rules on currency conversion. In the end almost all the existing banknotes were exchanged or deposited, with the result that there was almost no wealth destruction, just some redistribution within the economy as people paid to have their cash legitimised.

At the same time, the Reserve Bank of India was able to print enough new banknotes notwithstanding worries it would leave the country short of cash for a long time. Cash availability appears to be back to normal. I didn’t see any queues at ATM machines and only one or two machines seemed not to be stocked with cash.

In another sense, though, Modi’s currency reform is working—by encouraging people to move to digital transactions.

I was in Mumbai, Bangalore, Chennai and Mysore both for work and holiday and everywhere I looked there was a big push to shift the economy away from cash. This too is part of the government’s broader goal of driving the black economy into the open and generally cutting corruption, which also includes the mass digitisation of Indians’ fingerprints and irises to cut welfare fraud and theft.

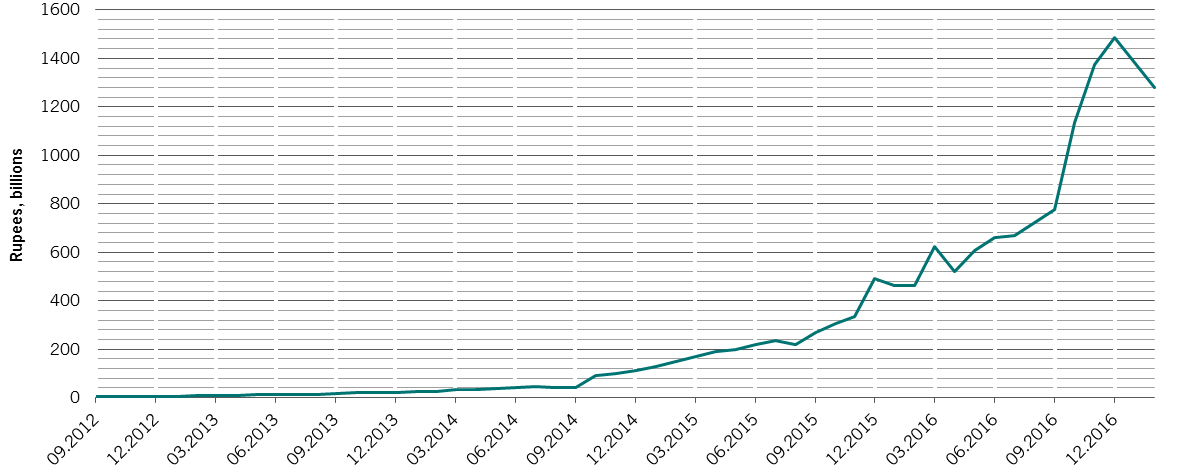

Moving money

Value of mobile banking transactions

Indians have an ever increasing number digital payment options. Almost all the banks are pushing card-based transactions, whether mobile swipe cards or credit cards. The government has launched Bharat QR, a QR code that allows people to make cashless transactions.

The most high profile payment system, however, is Paytm, which is owned by an Indian entrepreneur and has had substantial funding from Alibaba. It’s advertised everywhere. It is marketed aggressively with strong incentive schemes to get people to use it, like cashback deals. Recently, Paytm was awarded a banking licence so that it can pay people interest on the balances they transfer to it. It is acquiring customers fast and certainly seems to be establishing itself among retailers. The owner of one small shop told me that he’d been struggling to get a Paytm system installed because the company has been so busy, though so far it still isn’t making money.

Of course the digital revolution has only just started. It’s barely touched street traders, who still overwhelmingly rely on cash. One snack vendor I spoke to said he didn’t have a bank account and had no knowledge or awareness of digital payment systems. Of course this shouldn’t really be a surprise given many of these traders’ regular transactions are worth less than a dollar. They suffered initially from the demonetisation but business is now back to normal, though conditions have been more volatile for big-ticket items.

There are reports that Indians are using new notes to avoid tax on property transactions – historically, they’ve paid about a fifth of the purchase price with bank notes – though the fact that the real estate market is weak could mean Modi’s measures are taking effect.

Indeed, although demonetisation has so far had mixed results, overall, it’s helping to push forward Modi’s efforts to clean up India’s economy. For example, the traffic police are notoriously corrupt. But now, when they stop motorists for infractions they are increasingly having to take fines in the form of digital payments, making it harder to pocket the cash. In Mysore, I saw them photographing licence plates of offending vehicles without stopping them, so that owners are fined automatically.

If anything, demonetisation has made Modi more popular, particularly among the middle classes and people think he’ll succeed with his reforms. He’s brought a sense of optimism to the country. His political party, the BJP, won major victories in recent state polls, suggesting he’ll keep his prime ministership after the next general election in 2019, which would give him tenure to 2024.

That optimism now needs to translate into more corporate investment. Job creation is below par, while most of the capital expenditure is being done by the government. On its own, the government can’t do enough to sustain an economy that ought to be growing by around 7.5 per cent a year. But even here the signs are hopeful: Indians have increasingly been putting money into domestic equities.

India has a long way to go before it becomes a cashless economy, but demonetisation has resulted in Indians using less cash. It’s compressed three to four years of economic evolution into as many months. And with an ever greater number of transactions being recorded digitally, it has also taken a bite out of tax evasion. Modi’s drive to shake things up, to cut corruption and bring more of the economy into the open is bound to reap rewards over the longer term.

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer. This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.