Powering the green transition with semiconductors

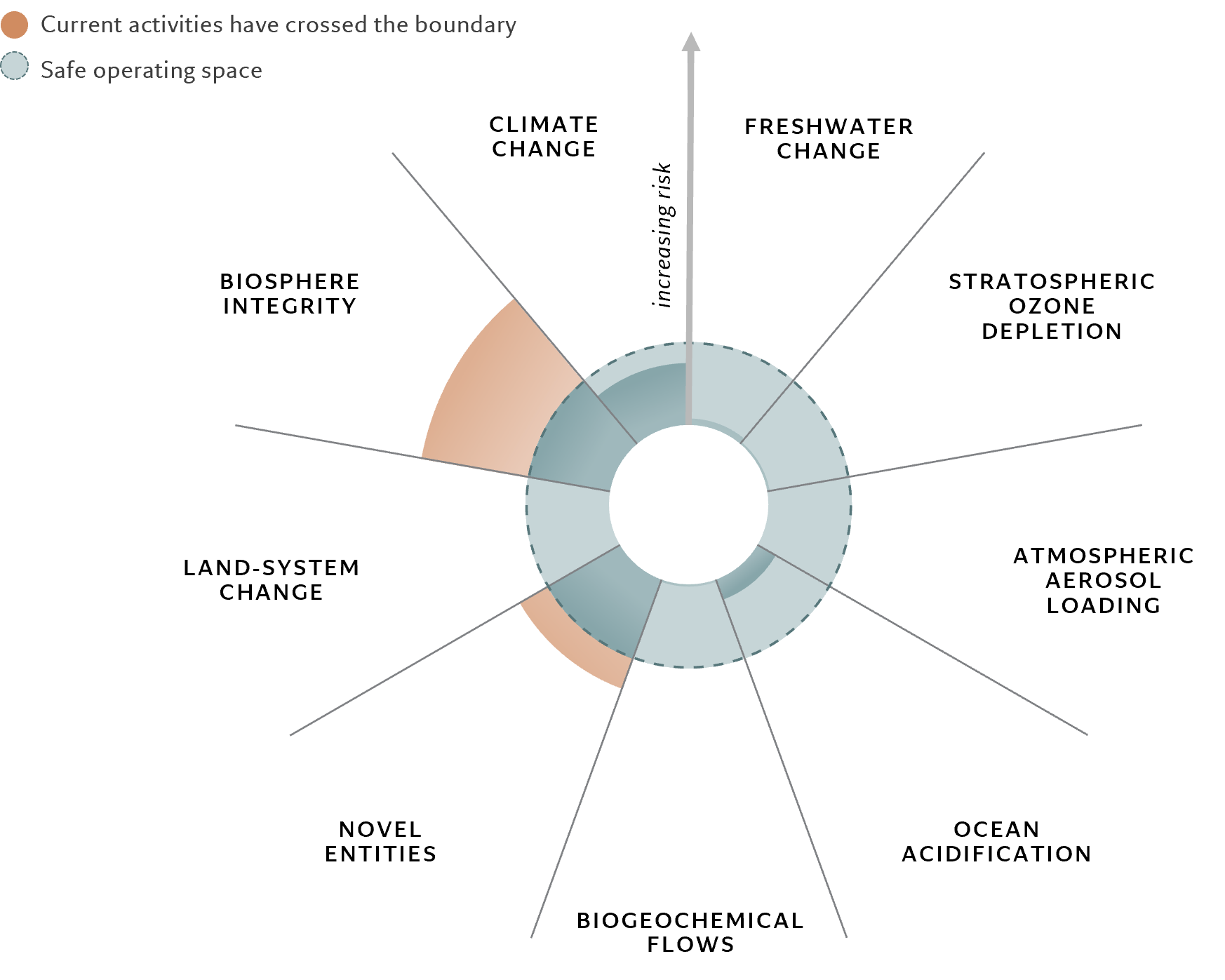

As long-term, responsible investors, we place great emphasis on the environmental credentials of industries and companies when building portfolios. But this also needs to be measured against the crucial role that semiconductors play in the green transition. In other words, it is essential for climate-oriented investors to look beyond the industry's carbon footprint and assess what experts call the ‘handprint’, or the positive impact that it has on the rest of the economy.

For semiconductors, that positive impact is particularly large when it comes to electrification – a key element of decarbonisation.

If we want to reach net zero by 2050, the International Energy Agency estimates that the proportion of electricity within total energy use will have to increase to 50 per cent from the current 20 per cent, replacing fossil fuels.3

That also means that the share of renewable electricity has to rise to 90 per cent from 30 per cent. We need to electrify first, in order to be able to decarbonise. And we also need to cut total energy consumption, which will require a 3 per cent annual improvement in energy intensity of the economy, double the current rate.4

We believe semiconductors are critical enablers of the green transition.

None of this can happen without semiconductors.

One category of specialised chip, “power semiconductors”, is crucial to facilitating electrification. These chips are used mainly to control the supply of electric power, as well as its conversion (from direct current to alternating current and vice versa), transfer and storage.

Although they represent only around 5 per cent of the overall semiconductor market, or USD40 billion, they have a crucial role to play.5

In solar power plants, for example, efficient and reliable power semiconductors are required to convert electricity from direct current to alternating current and transmit the power with minimal losses.

Semiconductors are also essential in the modernisation of electricity grids, enabling them to become more responsive to shifts in power supply and demand.

Chips are just as vital for the auto industry. The semiconductor content required for cars is now several times greater than a decade or two ago due to the switch to electric vehicles and the development of smart cars.

Semiconductors are therefore crucial across the whole electrification value chain, from the development of renewables to grid storage to electric cars and their chargers.

This leaves investors with a conundrum to resolve. How to reconcile semiconductor companies' impact on the natural world with the positive systemic impact of their products?