Asset allocation: no recession panic (yet)

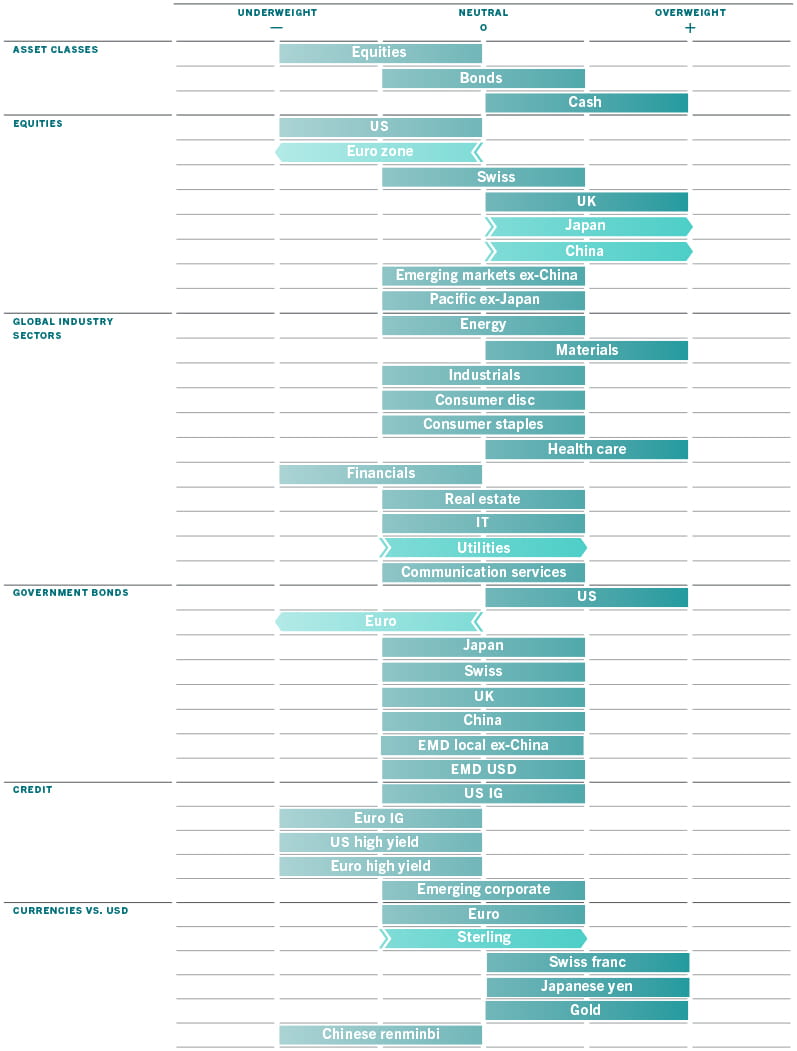

The risk of a recession is rising as central banks put the squeeze on monetary conditions across much of the world. That and the fact that valuations aren’t yet sufficiently cheap despite this year’s steep selloff, mean that we maintain our underweight on equities.

Indeed, with the exception of commodities, assets of all stripes have suffered hefty losses since the start of the year, largely to the same order of magnitude, generally down some 10 per cent to 15 per cent making it exceptionally difficult for investors to avoid being caught in the general riptide. A portfolio composed equally of US stocks and bonds has lost more in the first six months of the year than at any point since the Great Depression.

Economic conditions, however, are managing to remain resilient for now, so we keep a neutral stance on bonds overall – our leading indicators suggest central banks won’t tip major economies into recession this year as they seek to control inflation.

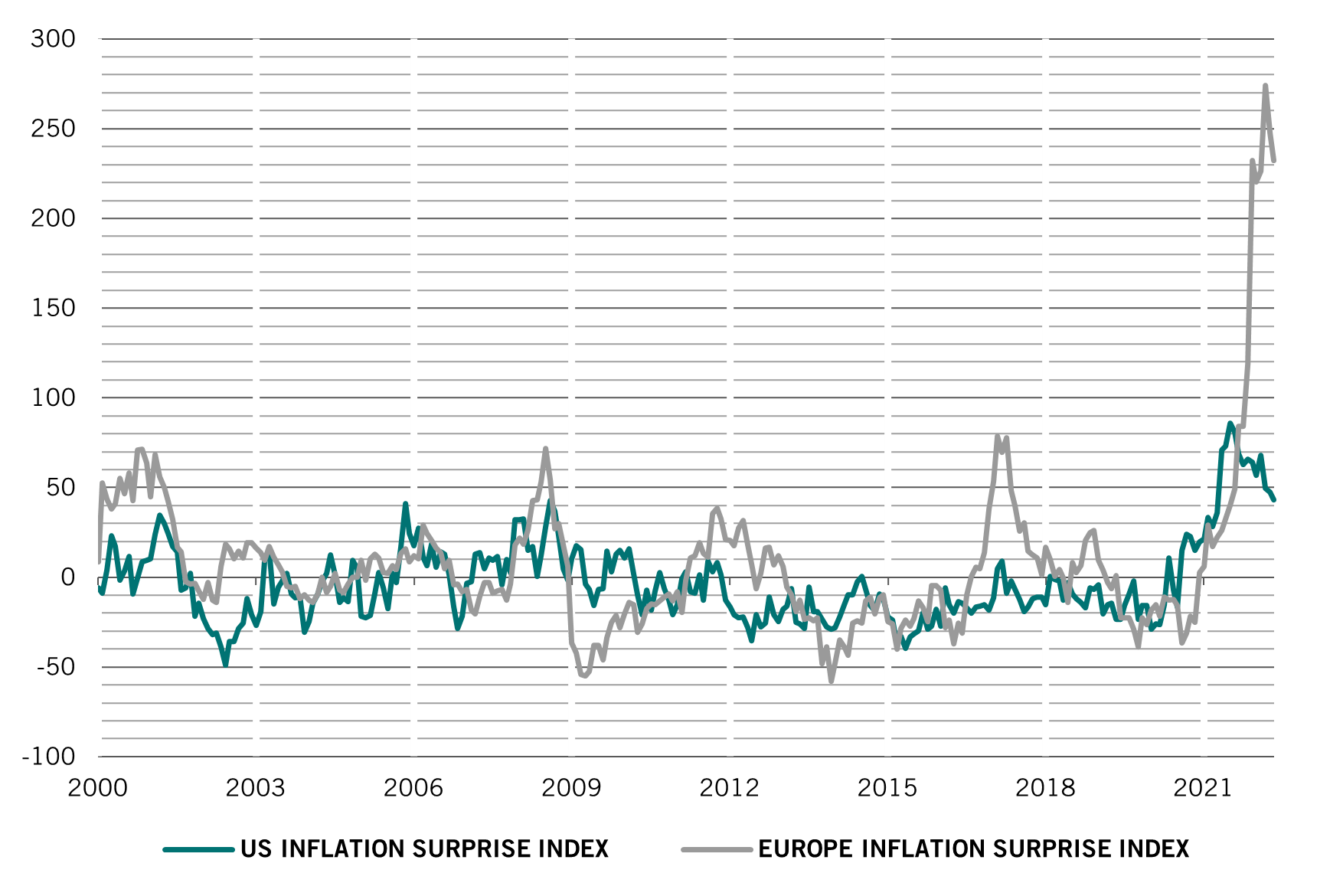

The question for the markets now will be whether central banks relent on rate hikes before they have inflation fully under control. So far they appear to be fixed on their policy course. But with signs that inflation has peaked, some of the pressure on them to make ever more extreme moves is easing, reducing the risk of a policy mistake.

Our business cycle indicators suggest the world economy will expand at a modest 2.9 per cent in 2022. Within that broad forecast, we have trimmed our expectations for the euro zone and Australian economies while upgrading our expectations for emerging markets, thanks to strength in both India and Russia. Emerging Asia's recovery looks particularly encouraging, thanks in part to China’s resurgence.

Notwithstanding the US economy’s marked slowdown, we believe the risk of a full-blown recession for this year is overstated, though the odds are high for 2023. Excess household savings amount to USD2.3 trillion, some 12 per cent of income, and, together with a solid jobs market and the post-Covid recovery, should be enough to offset a squeeze on consumers from rising prices and interest rates. One worry, however, is the downturn in housing: construction activity is down some 30 per cent, with surveys suggesting more to come.

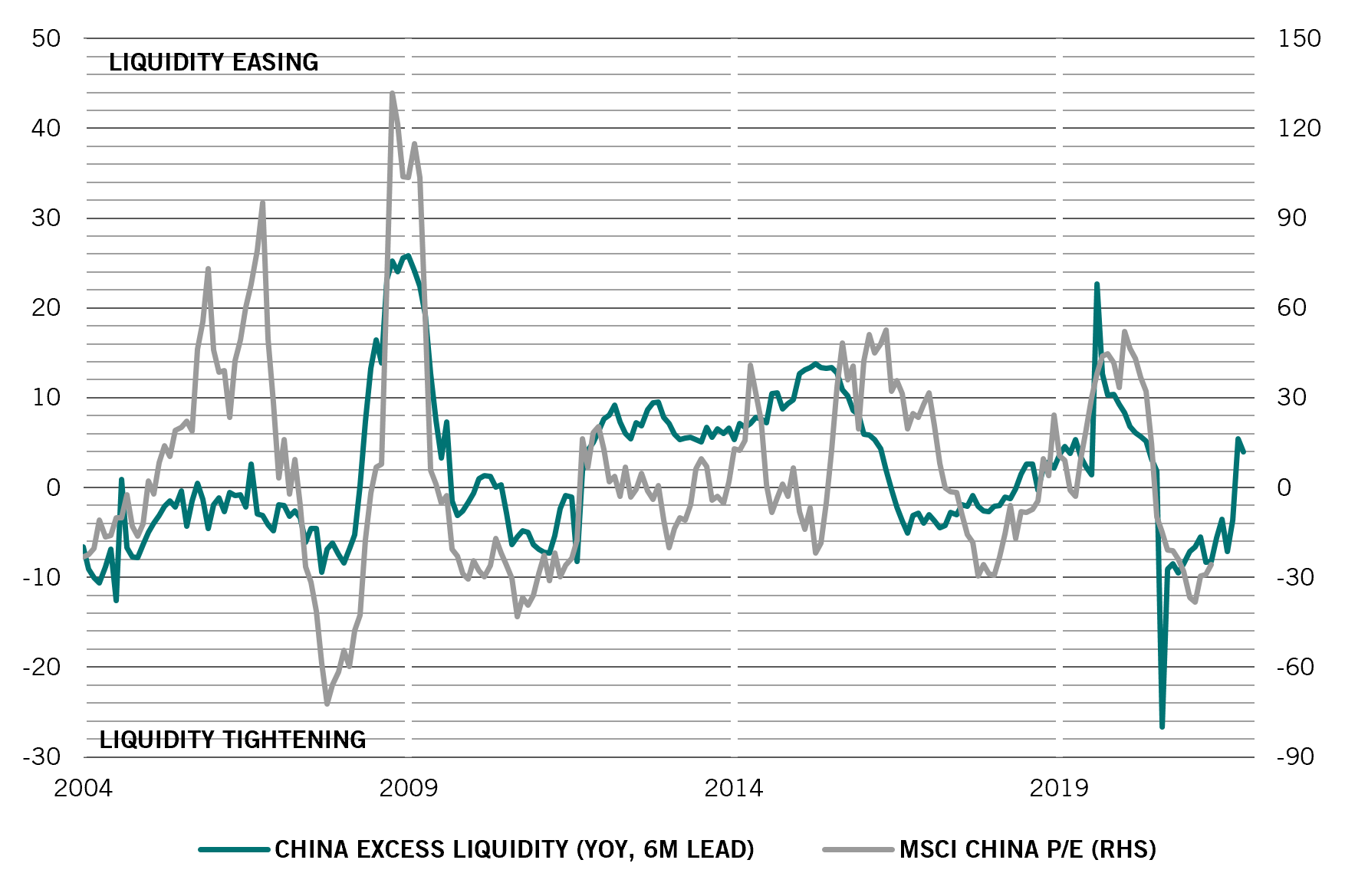

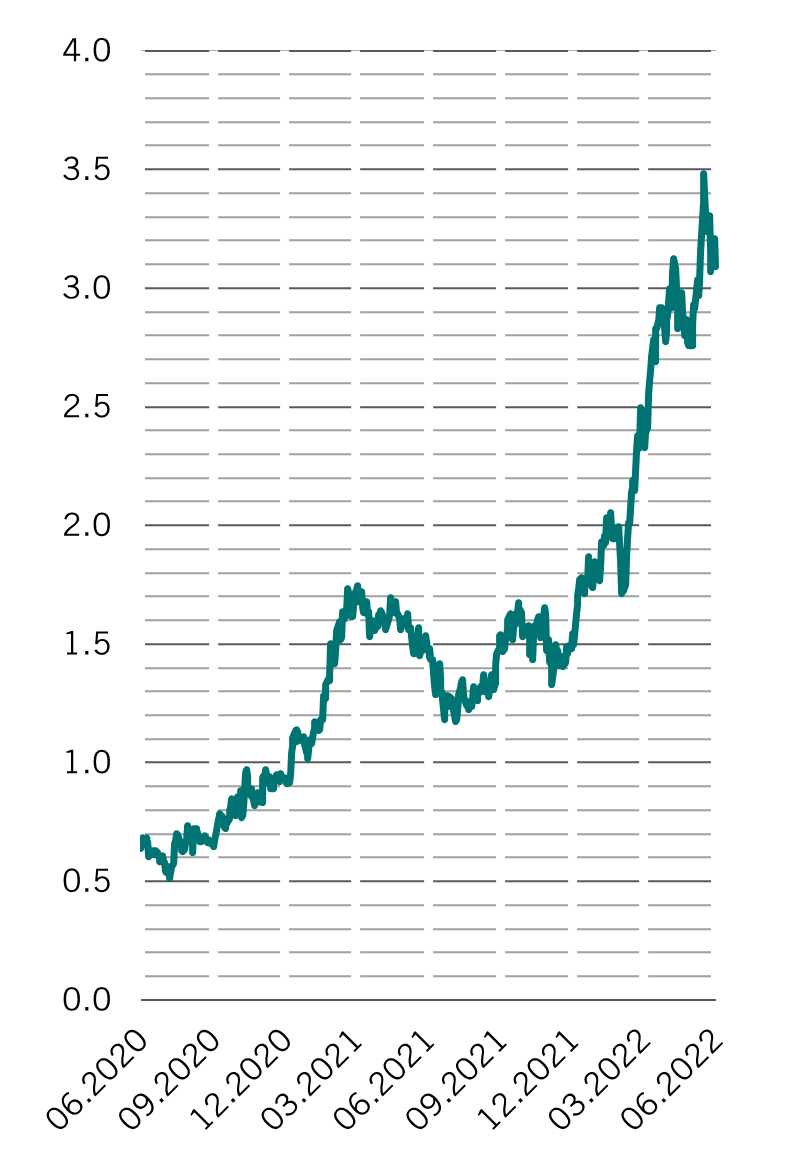

Our liquidity indicators show a continued squeeze on monetary conditions outside of Asia. Financial markets are pricing in some 200 basis points of cumulative interest rate hikes from the major central banks over the coming 12 months. What is more, some central banks – with the Bank of England in the lead – are poised to launch quantitative tightening. That’s to say they are not only going to be allowing existing bonds in their portfolios to mature but will also actively sell their holdings. In all, central banks are removing close to USD1.5 trillion in liquidity per quarter, our calculations show.

Partially offsetting this tightening is the People’s Bank of China, which is now easing on all fronts, while the Bank of Japan is sticking to its yield curve control strategy, which has forced it to step up bond purchases.

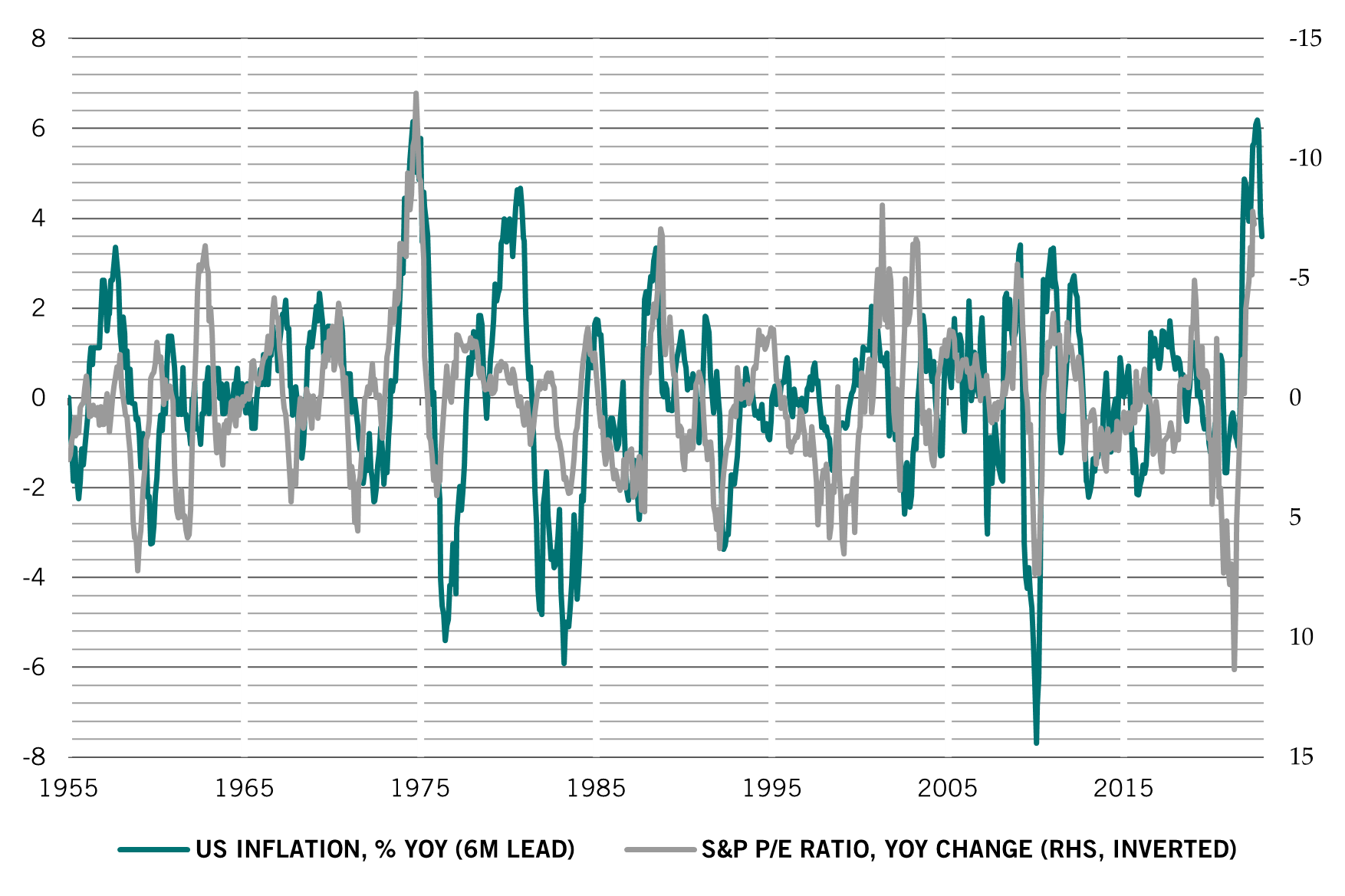

After the heavy losses bonds and equities have suffered, valuations are starting to flash green again. But they are not close to being cheap enough to encourage investors to ignore fundamentals. Among sovereign bonds, UK gilts look particularly attractive. Wider spreads and hefty drawdowns leave US high yield and European investment grade credit looking attractive. On the flip side, index-linked bonds are looking expensive – investors are paying a lofty premium for inflation protection.

Our technical indicators show that the trend signals are negative for equities and even more so for bonds. However, seasonal trends should prove supportive for bonds over the coming two months. Sentiment indicators no longer flash panic, though remain depressed – risk appetite appears to have troughed for now and investors have trimmed their cash and defensive positions. At the same time, positioning on S&P 500 futures was net short for the first time since 2016.