Asset allocation: balancing risks

There are few certainties when it comes to investing. Take Covid-19. Just when many parts of the world looked to have got to grips with the coronavirus pandemic, the US, South Korea and Beijing re-imposed lockdowns to contain a surge in new cases. A standing reminder that virus infections could – as the World Health Organization points out – ebb and flow for up to five years.

Still, there are some things investors can be certain of in 2020. Corporate profits will fall precipitously, and central banks will move mountains to support the economy. The task is to determine which of these will have a stronger bearing on financial markets.

Corporate earnings prospects are clearly a concern. The consensus among analysts is that profits will decline by about 20 per cent this year following the deepest recession in more than a century. Our models paint an even more pessimistic picture. Globally, earnings could drop some 30 to 40 per cent year-on-year.

But that does not mean equity and corporate bond markets are due a sharp fall. Central banks are committed to containing the damage. According to our calculations, the US Federal Reserve will inject another USD1.3 trillion of additional monetary stimulus this year while the European Central Bank will unleash an extra EUR1.1 trillion.

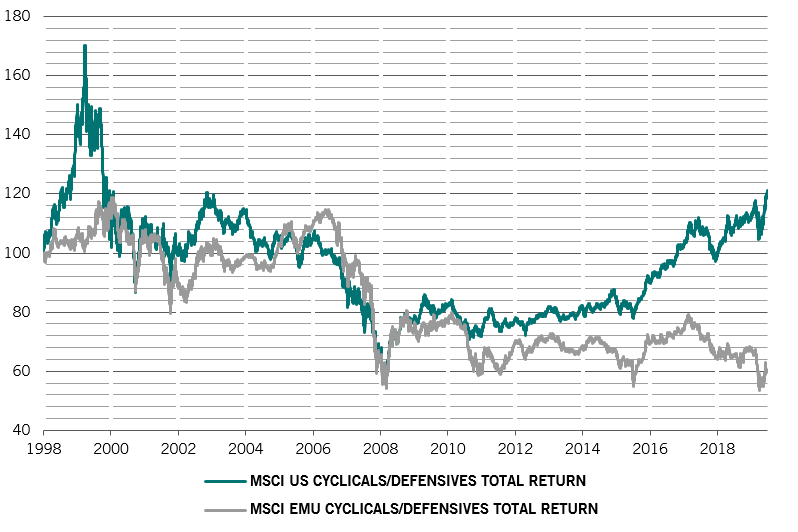

Broadly speaking, this suggests the decline in earnings per share will be offset by a central bank-inspired expansion in price-earnings multiples. Crucially, however, stocks that trade on cheaper multiples, such as European equities, should see stimulus hold sway. Which is why we have raised our exposure to European stocks to overweight. We retain a neutral stance on most other stock markets.

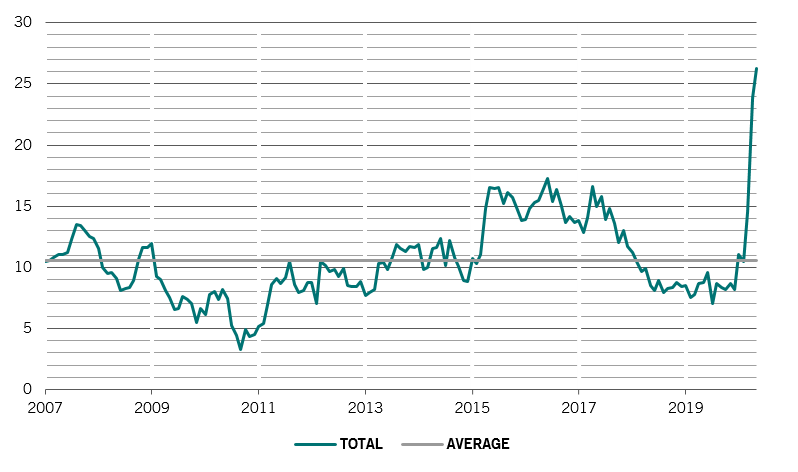

Our liquidity indicators flash green for riskier asset classes. Both the Fed and the ECB are set to deliver vast amounts of new stimulus. Bank lending is also very strong globally as banks’ capital positions are solid and government loan guarantees are helping direct credit to businesses hit by the crisis. The ECB’s targeted long-term refinancing operations (TLTRO) have proved especially effective in channelling much-needed credit to the economy. China is bucking the trend, however. With the economy recovering, authorities in Beijing will look to rein in stimulus. Interbank lending rates – Shibor – have risen by some 60 basis points over the past month to above 2 per cent.

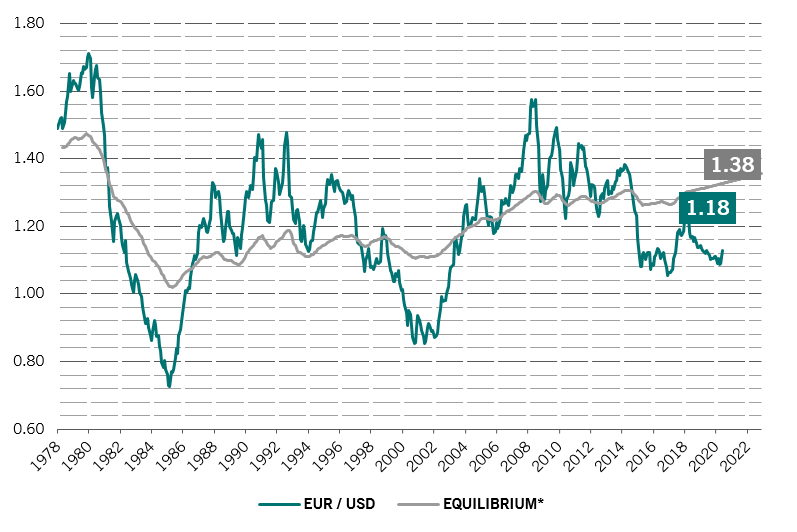

Our valuations gauges show equities are, in aggregate, fairly valued. Compared to bonds, though, they remain cheap – provided the pandemic does not weigh on profit growth over the long run. European markets look attractive relative to others. While the discount at which European stocks trade to their US peers has narrowed in recent weeks, there is scope for it to tighten further. US bonds, while cheap heading into the crisis, are approaching expensive levels.

Our technical readings show investors have turned less bearish on stocks – the indicator has moved from oversold to neutral. That increases the scope for a correction over the near term. High yield bonds also look vulnerable to a sell-off as flows into the asset class have been unusually strong.