Select your investor profile:

This content is only for the selected type of investor.

Individual investors?

The battle against inflation: are emerging markets ahead of the curve?

As Covid's impact fades, inflation has become a major worry for policymakers. Surprisingly, emerging market central banks are moving faster than their rich country peers to contain the threat.

Written by

Nikolay Markov

Senior Economist

Developed economy central banks have fallen behind the inflationary curve, despite increasingly hawkish guidance. The UK, Swiss and Canadian central banks in particular have to tighten monetary policy aggressively if they are to regain control over price pressures, according to Pictet Asset Management's proprietary models.

By contrast, a number of emerging market central banks have been paragons of prudence and will be able to start cutting rates as early as next year – a state of affairs that turns historic norms on their head.

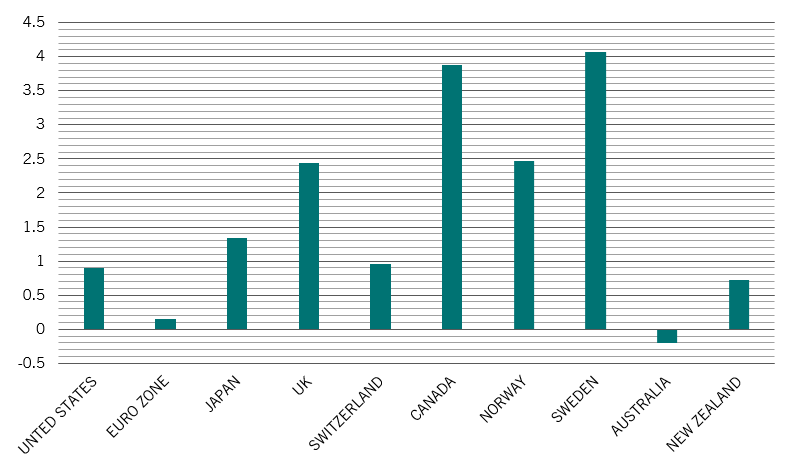

FIG. 1 - Advanced economy central banks behind the curve

Taylor rule estimate for change in key policy rate needed by 2023 subject to financial stability constraint, percentage point increase/decrease in rates

Many developed economy central banks are in a difficult position. Take the Bank of England. Its inflation-fighting credibility has come under pressure from a decade of ultra-easy monetary policy during which time inflation has frequently breached its 2 per cent target. Lately the UK inflation running exceptionally hot – CPI inflation was 5.5 per cent in January and is forecast to breach 7 per cent in the coming months.

At the same time, the UK private sector has a heavy burden of debt, with total credit to the private non-financial sector running at some 160 per cent of GDP – in the early 1990s that ratio was under 120 per cent.1 This makes the economy particularly vulnerable to interest rate rises.

As a result, any rate rises would have to take into account financial stability. According to our Taylor Rule model,2 we estimate the UK would have to limit rate hikes to 2.4 percentage points above the current 0.5 per cent – still a dramatic move, but one that would balance strains on the economy with recovering Band of England policy credibility (see Fig. 1).

The story is similar for some other developed economies, particularly Sweden and Canada, which, in both cases, need to see rises of around 4 percentage points in 2023 to maintain financial stability.

Emerging market central banks, on the other hand, have largely taken the inflationary bull by the horns, which means they’ll be in a strong position to start easing policy in the coming year.

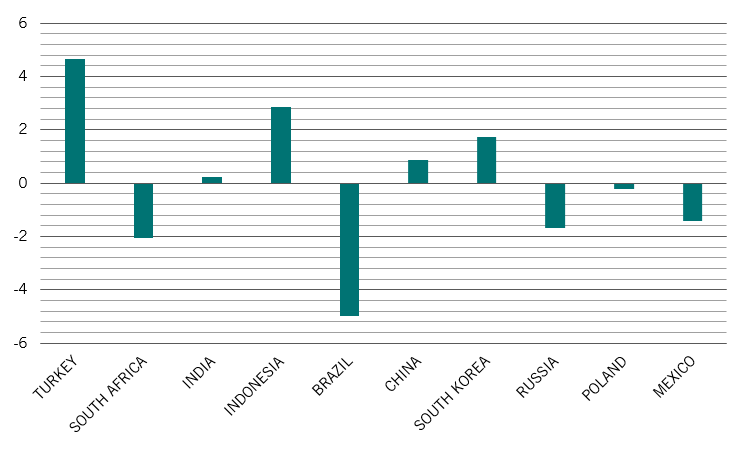

FIG. 2 - Emerging markets central banks ahead of the curve

Taylor rule estimate for change in key policy rate needed in 2023 subject to financial stability constraint, percentage point increase/decrease in rates

Our model suggests that Brazil, Russia, Poland, South Africa and Mexico will be in a position to cut rates in 2023, with Brazil having scope to slash its policy by nearly 3 percentage points from the current 10.75 per cent [see Fig. 2].

In a nutshell, a number of developed economy central banks will have to work hard to restore their credibility. By contrast, emerging market central banks have largely been quick to anticipate and respond to the inflation problem. The trick will be to negotiate a tightening cycle while minimising financial disruption – years of accumulated corporate and household debt thanks to the low rate era could yet cause trouble.

[1] Bank for International Settlements data, to Q2 2021. Data as at 16.02.2022.

[2] We use state-of-the-art semiparametric Taylor Rule to account for a possibly changing Central Bank’s responsiveness to macroeconomic fundamentals depending on the state of the economy. In that specification, the policy rate is set as a nonlinear function of our inflation forecasts, real GDP growth forecasts and real effective exchange rate growth rate.

related articles

The inflation conundrum

The prospect of a sharp pick-up in inflationary pressures is beginning to concern investors. Our historical analysis sheds light on how stocks, bonds and other asset classes behave during periods when inflation takes hold.

April 2021

Which emerging markets are most at risk from US rate hikes?

Our model shows which emerging nations are most vulnerable to a tightening of US monetary policy.

January 2022

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Investor Information Document (KIID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 15 avenue J.F. Kennedy, L-1855 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any. The KIID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. Pictet Asset Management (Europe) S.A. has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.