Select your investor profile:

This content is only for the selected type of investor.

Individual investors?

EM local bonds shine in a low-yield world

With developed market yields stuck at zero, EM local bonds look increasingly attractive, especially given these economies' strong fundamentals.

Written by

Alper Gocer

Head of Emerging Markets Fixed Income

The stars are aligning for emerging market local debt. The asset class may have been in the doldrums since the global financial crisis, but it is now poised to outperform thanks to a raft of positive factors – from emerging markets’ solid economic fundamentals and undervalued currencies to the prospect of zero interest rate policies in developed economies for years to come. As a result, the asset class makes a strong case for inclusion in yield-starved portfolios.

Compelling fundamentals

Those positive economic fundamentals underpin the case for a dependable flow of returns from emerging market assets, allowing them to replace yield that other investments no longer provide.

The Covid pandemic has been destructive for economies around the world. But emerging market countries are rebounding sharply. Apart from services industries, economic activity has recovered to December 2019 levels for these countries overall.

To be sure, the strength so far has in significant part been driven by a rampant Chinese economy, where the likes of car sales, construction, industrial production and exports are well above where they were a year ago, and retail sales only just below. But the wider recovery looks to become increasingly self-sustaining. That momentum will only build as Covid vaccines become widely available over the coming months.

Indeed, emerging market economies are outperforming their developed market counterparts. EM industrial production is running at above fourth quarter 2019 levels, while in developed economies it continues to lag by some 6 percentage points. The fact that EM economies are much more heavily geared to industry and less to services – developed economies are some 70 per cent services against 54 per cent in emerging economies – is a key factor for the differential in economic performance.

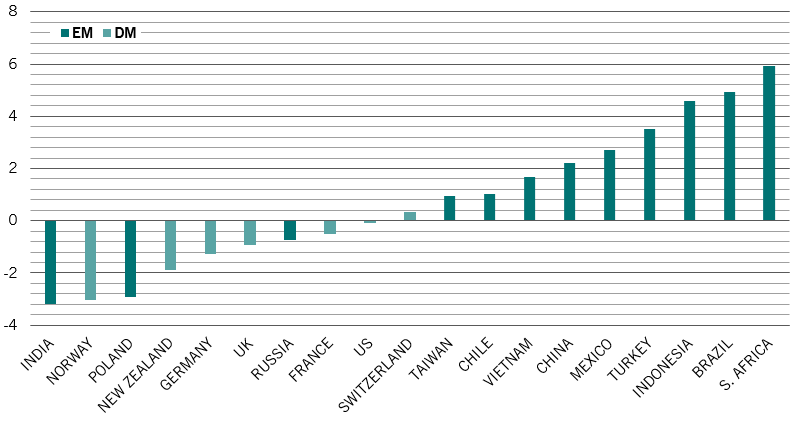

Fig. 1 - Real yields

10-year government bond yields deflated by core CPI

Meanwhile, the outlook for global trade is increasingly less gloomy. That’s critical for EM economies, given their relatively heavy reliance on exports compared to their developed counterparts. Global trade was already suffering under President Donald Trump’s anti-trade policies, particularly against China, when the Covid shock hit. Recovery, when it came, was just as sharp. That return to health is set to continue under a Joe Biden presidency. True, trade tensions between the US and China are unlikely to disappear completely – geopolitics is likely to ensure the two behemoths remain wary of each other’s intentions. But relations between the US and its other trade partners are bound to be considerably more diplomatic and less fraught.

Increasingly robust global demand – not least from China – will continue to support commodity prices. And given the relative weight of commodity exports in their economies, this should offer further support to emerging market countries.

Attractive valuation

As an asset class, emerging market local currency debt has been a source of frustration for many investors over much of the last decade. Investment returns failed to keep up with ever improving fundamentals. This was, however, largely down to challenging external factors, such as a strongly appreciating dollar. A raft of negative headlines specific to a handful of leading EM countries only made investors more wary.

Now, though, improvements to the global macroeconomic and policy outlook come against a backdrop of deeply attractive valuations and historically light investor positioning in EM local currency debt. As a result, yield-starved investors are increasingly being drawn to the asset class. The economic growth outlook is likely to translate into relative strength for EM currencies. That upward pressure is supported by interest rate differentials. Nearly all major developed countries' 10-year government bonds are posting negative or zero real yields. With 76 per cent of developed market (DM) sovereign debt now trading at negative real yields, DM investors are being forced to search for alternatives.

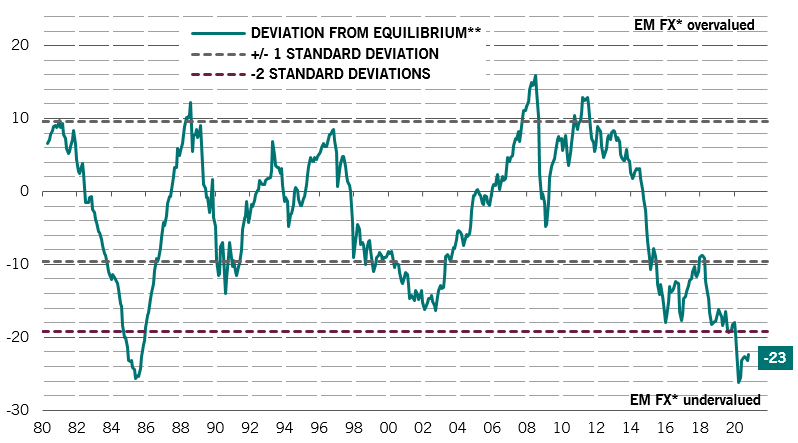

Fig. 2 - Going cheap

Emerging market currencies valuation relative to USD

** Based on relative prices, relative productivities and net foreign assets

Source: Pictet Asset Management, CEIC, Revfinitiv. Data from 01.01.1980 to 01.12.2020.

That’s likely to persist given both the US Federal Reserve and the European Central Bank have shown commitment to keeping interest rates at or near zero and to putting downward pressure on yields along the curve.

By contrast, equivalent sovereign debt in most EM markets offers solidly positive real yields, ranging from 2 per cent to just under 6 per cent (see Fig. 1). Pictet Asset Management economists estimate that EM currencies are some 25 per cent undervalued, which should give them further support (see Fig. 2).

Making EM sovereign bonds more attractive still, debt levels in emerging market economies are considerably smaller than in developed countries – our economists forecast a debt to GDP ratio of 66 per cent for EM economies versus 127 per cent for DM in 2021.

Go with the flow

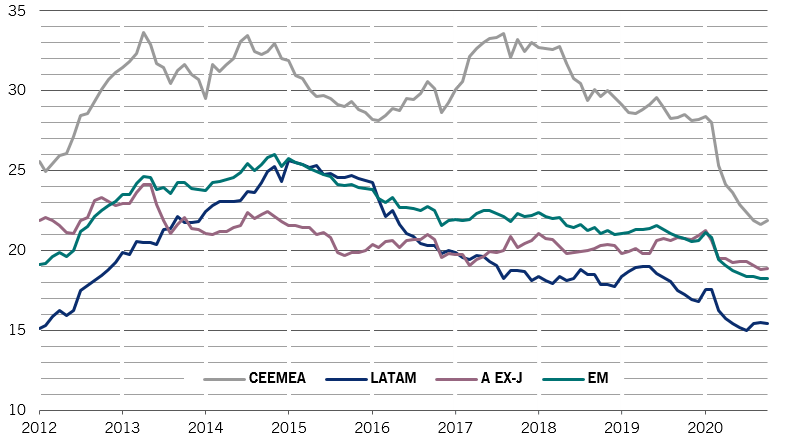

Emerging markets now represent some 50 per cent of global GDP. A proportion that will only increase as these countries catch up with the developed world in per capita output. Yet emerging market assets represent a disproportionately small fraction of investors’ portfolios – a proportion that’s declined over recent years. For instance, foreign ownership of many emerging market local currency bonds is at or near 10 year lows (see Fig 3).

But flows have been returning to emerging market assets. EM hard currency bonds have been boosted by demand from foreign investors hungry for yield. As emerging economies’ strong fundamentals become increasingly obvious, more investors will start to notice the benefits of EM local currency bonds as well, at which point a lack of positioning could spark a sudden and dramatic surge in prices. The speed of a move is only likely to be boosted by the fact EM local currency bonds are increasingly easily accessible. Demand, in turn, will be supported by a growing local institutional investor base. Indeed, EM inflows are running at their strongest rate for nearly a decade and, in the fourth quarter of 2020, are on track to see the strongest quarterly inflows since the first three months of 2012.

What’s more, this stage of the global economic cycle – when economies worldwide are recovering from a downturn, with growth momentum on the upswing – is the best phase for risk assets to outperform. This should particularly benefit emerging market currencies and bonds.

Fig. 3 - Underowned

Foreign ownership of emerging market debt, % of outstanding

related articles

The investment landscape in 2021

Next year should see the global economy recover strongly from the ravages of the pandemic. Expect emerging market assets to shine.

November 2020

Chinese onshore bonds: going mainstream

The inclusion of renminbi-denominated debt in the flagship global benchmark bond index will transform the asset class into a strategic investment.

February 2020

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Investor Information Document (KIID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 15 avenue J.F. Kennedy, L-1855 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any. The KIID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. Pictet Asset Management (Europe) S.A. has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.