Our chief economist Patrick Zweifel assesses the impact the virus could have on growth in China and emerging markets

Written by

Patrick Zweifel

Chief Economist

Share this article

Over the worst?

Despite recent developments, our baseline assumption is that the number of global cases of Covid-19 (the coronavirus) will peak in the first half of March. As a result, the biggest economic impact should be felt during Q1 2020, followed by a full recovery in Q2. The main risks are that the contagion may last longer and/or that the virus may become more virulent.

Analysing the economic impacts of an outbreak

A pandemic impacts economies via three channels:

Mortality: impacts production as it removes certain people permanently from workforce;

Illness, hospitalisation & absenteeism: output is temporarily affected;

Efforts to avoid infection: individuals change their behaviour in the face of a pandemic by (i) being quarantined (ii) avoiding travel from/to infected regions (iii) reducing consumption of services: restaurant, tourism, entertainment, mass transportation and offline retail shopping.

A pandemic impacts economies via three channels...

Although a tragedy, mortality is likely to have very limited economic impact in the case of the coronavirus. We look at the impact of the other two channels on China and on the rest of emerging markets.

The economic impact on China: supply and demand shocks

The two channels impact China in two ways. First, via supply shock: output is severely reduced as fewer people are going to work due to illness & quarantine. This is combined with a prolonged factory shutdown after the extension of the Lunar New Year holidays.

China will be impacted by supply and demand shocks

The second is via demand shock. Quarantine and the 'fear- factor', restrict people’s mobility and lead to a temporary large decline in activity in services. We estimate the sectors most impacted represent 52% of China's GDP. Yet services that will be most impacted represent 18% of GDP (transport 4.5%; wholesale & retail 10%; accommodation 2%; entertainment, culture & sport 1%).

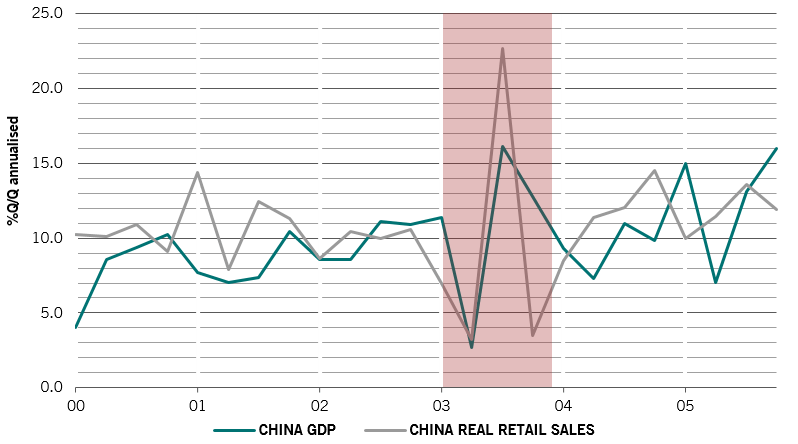

Comparing to SARS

Coronavirus is clearly very similar to SARS. Back in 2003, this outbreak caused a 1.5 percentage point fall in China's real GDP y/y between Q1 and Q2 while nominal retail sales fell 2.3 percentage points. These were followed by a very substantial rebound (+1.2 percentage points for GDP and +2.8 percentage points for retail sales).

Fig. 1 A short, sharp shock

SARs impact on China's GDP and retail sales

Source: Pictet Asset Management, CEIC, Refinitiv

The coronavirus shock is likely to be more pronounced this time as efforts to avoid contagion have been quicker and larger. In addition, the outbreak put the brakes on the usual Lunar New Year rush of spending on tourism and services.

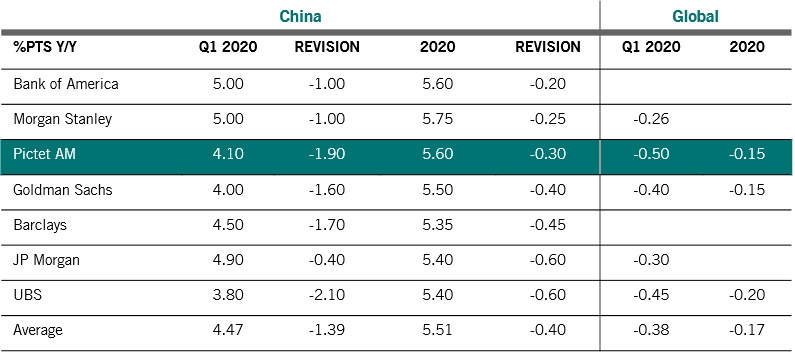

Revising our China forecast

As a result we have revised down our Q1 GDP growth forecast for China by 1.9 percentage points but expect a strong rebound in Q2 resulting in a full year negative impact of 0.3 percentage points (down to 5.6% from a previous forecast of 5.9%).

Fig. 2 - Forecasting coronavirus

Impact of Covid-19 on China and global GDP growth forecasts

Source: Pictet Asset Management, respective broker’s research

Our forecast takes into account the additional policy-easing we believe China will implement. This is best described as rescue measures rather than stimulus. Although monetary policy has already become more accommodative (7-day and 14-day repo rates were lowered by 10bps to 2.40% and to 2.55% respectively), we think fiscal policy will take the leading role in helping corporates to survive the large shock.

Similar to the SARS episode, Beijing will give more targeted support such as tax exemptions to certain businesses for a limited period of time. Anecdotal evidence reveals that local governments in Suzhou, Ningbo, Shenzhen, Shanghai have already announced supportive measures: waiver of office rental by 1-2 months; postponed tax filing; and a subsidy on interest payment of new corporate loans.

What about the wider impact on EM?

The impact of the virus on EM will mainly happen through three channels:

Quarantine & fear factor will hit tourism: the speed of government response suggests a larger impact than in 2003, with governments across Asia issuing travel advice as well as outright travel restrictions on travel to/from China.

Fall in Chinese demand will impact trade: China's demand accounts for 16% of the world's economy.

Shutdown of firms will disrupt global supply chain: the disruption to supply chains could be significant given China sits at the centre of Asian manufacturing. Wuhan is where disruption could originate from; local sectors most at risk are the auto and IT (see Figure 3).

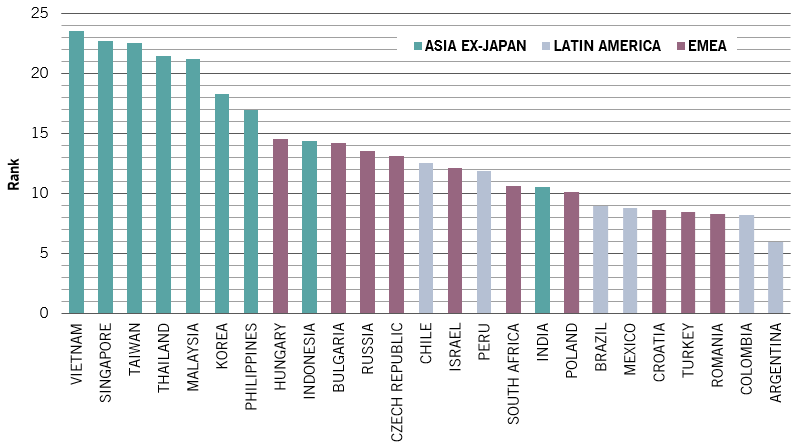

Fig. 4 shows that outside of China, the biggest concern is for Asia, in particular Vietnam, Singapore, Taiwan and Thailand. Indonesia and especially India look less vulnerable since they are more closed economies. The impact on the rest of EM should remain limited to big participants in the global value chain (e.g. Hungary) or big trading partners of China (e.g. Russia).

Fig. 4 - Which EMs are likely to be most impacted...

Coronavirus' impact on emerging markets: ranking based on countries’ exposures to China’s tourism & trade and to global value chain

Source: Pictet Asset Management, WTO, CEIC, Refinitiv as at February 2019

The economic shock from the outbreak will likely increase the pressure for more accommodative monetary policy in the region. That said, most central banks are unlikely to react immediately as they may need more time to evaluate whether the impact is transitory. The notable exceptions are Thailand and the Philippines where the central banks have already eased and will likely cut their policy rates again this year.

Elsewhere, Brazil and Russia have also cut rates. Meanwhile, the Monetary Authority of Singapore declared it has “sufficient room” to weaken the policy band of the Singapore dollar’s effective exchange rate. Overall, we expect the first line of support to come from fiscal policy for most economies.

Conclusion

A severe short-term impact that should be followed by strong recovery. Impact on global growth should be of some 0.15 percentage points.

It is worth stressing that global economic momentum was strengthening at the time of the outbreak and should naturally resume if the assumption of a transitory shock proves right.

Global economic momentum was strengthening...and should naturally resume if corona remains a 'transitory shock'.

In particular we would cite the following three tailwinds:

A fall in world inventories to 7-year lows which has supported a fourth consecutive month of strong rebound in new orders to inventories, a good short-term leading indicator of world industrial activity.

Strong signs of a rebound in global trade. Export orders and the export tech cycle is bottoming, having been a major factor behind weaker global exports.

Very accommodative monetary policies in EM, with the net number of central banks cutting rates reaching 63%, highest share since the global financial crisis. Monetary easing tends to lead activity by at least eight months.

Overall, the coronavirus outbreak does not change our constructive view on emerging markets. We still expect the emerging markets growth gap to widen relative to developed markets, it has just been delayed.

Patrick Zweifel joined Pictet in 1997. He is Chief Economist at Pictet Asset Management. Before assuming his current position in 2009, he was head of the “Macro Research Team” at Pictet Private Wealth Management. In particular, he had economic research responsibility for emerging markets and Japan, and for the development of quantitative models on major asset classes, primarily foreign exchange models. Before joining Pictet he was a research assistant in econometrics and monetary theory and worked on international research projects for the World Bank and the European Union. He holds a PhD in econometrics from the University of Lausanne.

Share this article

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Investor Information Document (KIID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 15 avenue J.F. Kennedy, L-1855 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any. The KIID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages.Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. Pictet Asset Management (Europe) S.A. has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user navigation and to collect statistical data. To refuse the use of cookies, change your settings or for more information, please click on the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.