If fixed income falls from grace, traditional stylised asset allocation is likely to underperform. A new approach to designing portfolios – and investment products – will therefore be needed.

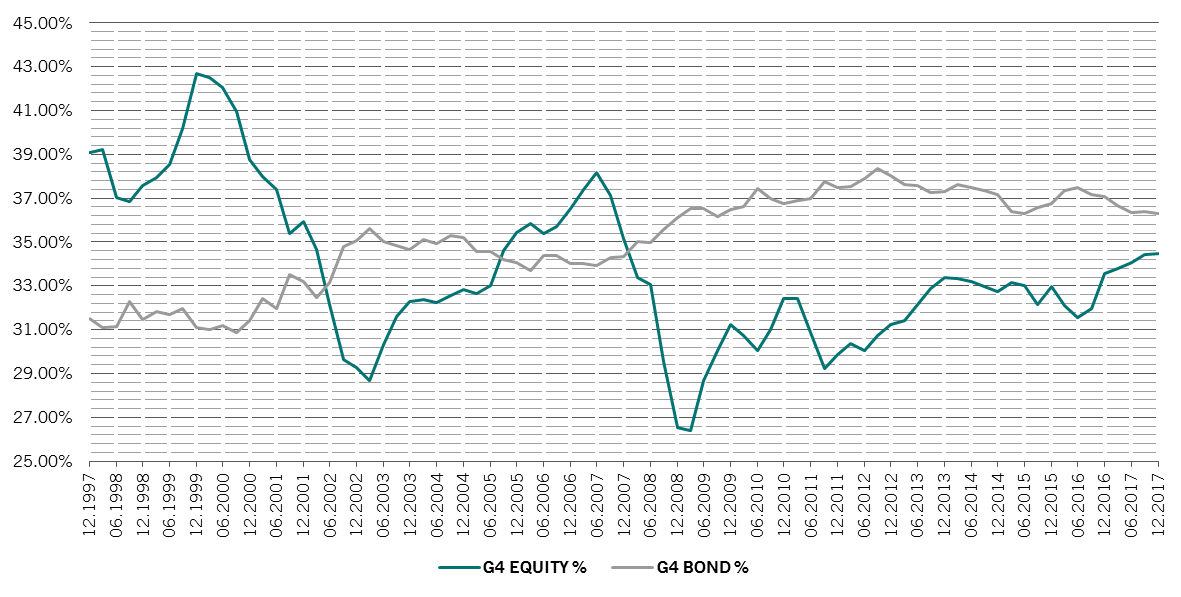

According to our calculations, the current average UK pension fund mix (of 47 per cent equities, 36 per cent bonds, 17 per cent alternatives/other)8 will return 0.5 per cent per annum less than would be required to reach a 50 per cent coverage of final salary at retirement.

A more growth-focused portfolio should serve investor interests better by replacing some of the traditional bond holdings with a greater allocation to equities and alternatives. A 50/30/20 split would, for example, achieve the target, as long as a higher-risk, higher-return alternative, such as private equity, is selected.9

Infrastructure should do well, not least as buildings and cities adapt to cater to the ageing population. Private asset classes should also rise in popularity, with more vehicles designed to give mainstream investors access (see our Secular Outlook).

Even further up the risk curve, new types of investment – such as bitcoin, peer-to-peer lending or crowdfunded bonds – may attract a following from more adventurous investors.

Increased demand for riskier assets, in turn, is likely to result in the development of new investment products.

Increased demand for riskier assets, in turn, is likely to result in the development of new investment products. These could take the form of higher-risk, growth-focused pension wrappers for defined contribution (DC) savers, new outcome-oriented fixed income strategies, as well as products which lock capital away for relatively long periods of time.

In the face of growing demand, we think the rules on pensions will be relaxed to allow investment in a wider range of assets, including illiquid ones. At the same time, we expect that retail and wholesale investors will also gain access to a wider range of products, including ones which are currently reserved for institutions. In a decade or two, pension savings could well feature private equity and maybe even cryptocurrencies alongside government bonds.

There is also likely to be increased appetite for advice to better navigate the new investment landscape, particularly among the growing number of DC savers. More of that advice will come from robots of various forms. Betterment in the US and Scalable Capital in the UK are among those already offering robo-advice for individual pension scheme investors.

The longevity-driven shift in portfolio allocation is likely to crystalise as the first wave of DC pensioners approach retirement over the next two decades. US workers, for example, have an estimated retirement deficit of some USD4.13 trillion – more than a fifth of the country’s GDP.10