01

Summary

|

Opportunities

|

Threats

|

|

Opportunities

|

Threats

|

Economic growth will slow. And so will inflation – but not enough. Equity returns will be lacklustre, but bonds will fare better. The US’s stellar status in global stock markets will dim, while European equities will surprise in a good way, for a change. At the same time, emerging market (EM) economies will outpace the developed world, though question marks over the Chinese economy mean that we prefer EM bonds to EM equities. Geopolitical risk isn’t likely to diminish in any meaningful way, not with countries accounting for half of global output holding elections during the year, which is likely to result in a slight increase in market volatility.

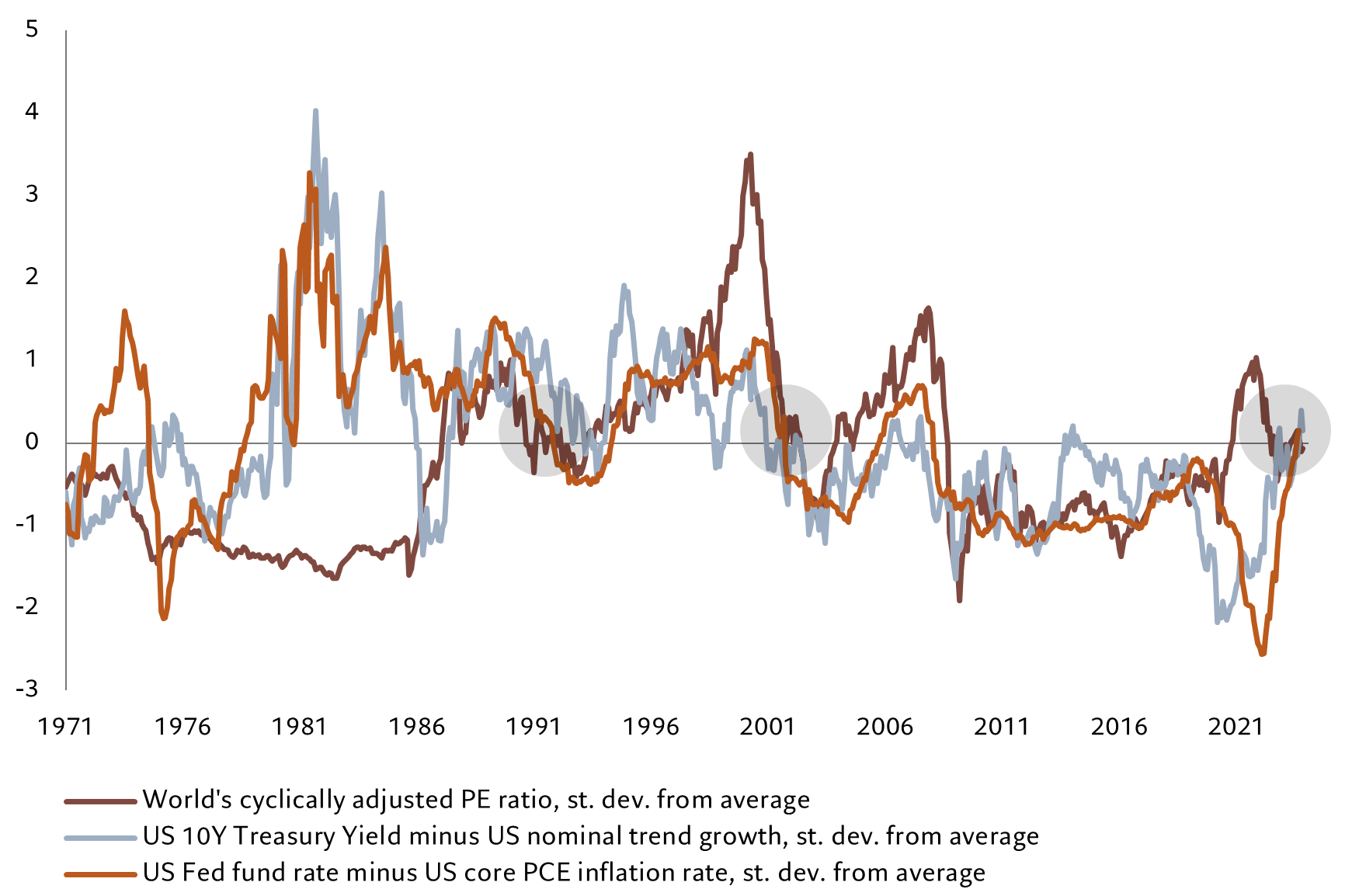

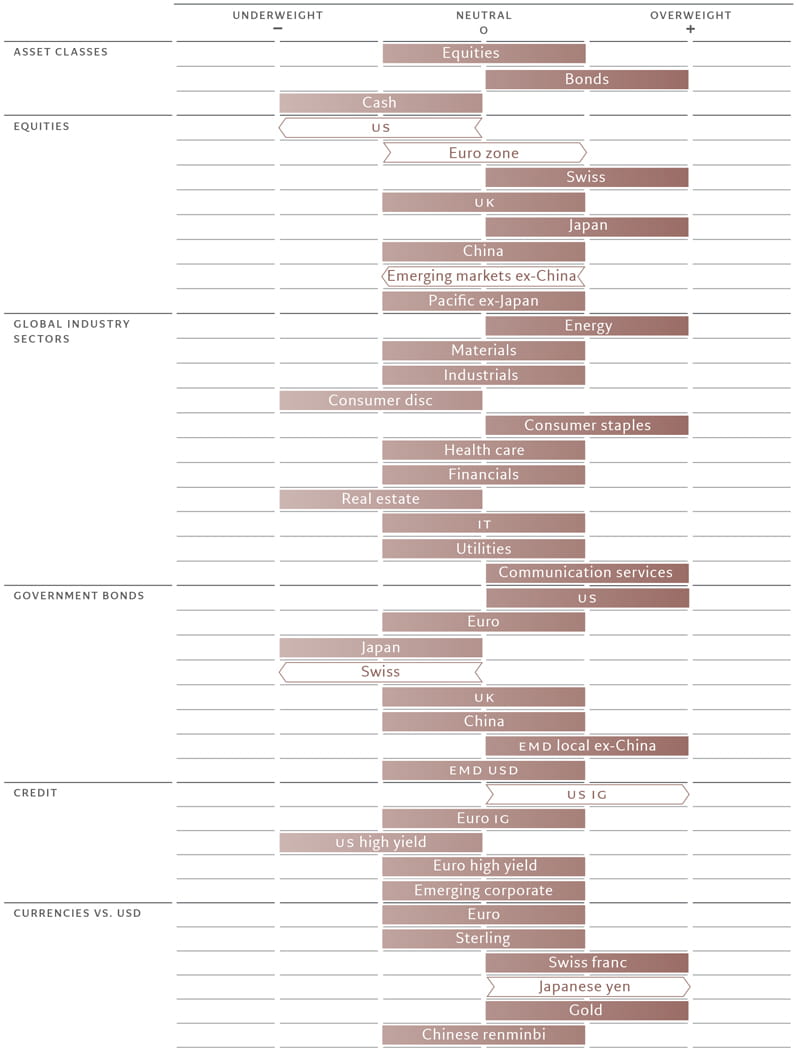

In all, 2024 will be less than a banner year for investors. But at the same time, we also expect some of the tight correlation between asset classes that has characterised the markets during the past few years – where equities and bonds have moved in lock-step – to ease. This should allow balanced portfolios to show better diversification (see Fig. 1).

Subdued growth but sticky inflation

The economic environment isn’t particularly promising: stagnating growth in developed economies, rising joblessness and inflation that stubbornly refuses to return to central bank targets will be prominent features of the investment landscape.

We expect developed economy inflation to fall back – we’re forecasting a rate of 3.0 per cent for 2024 from 4.7 per cent this year. But with central banks still smarting from having let inflation get out of control, as long as it remains above target, they’re unlikely to throw themselves into an aggressive easing cycle.

That said, the Bank of England looks likely to be the first major central bank to cut rates. The threat of recession could mean it starts to ease as early as May. We expect the US Federal Reserve to be more cautious in delivering cuts than the market currently expects, but still see it trimming twice in the latter half of the year and the European Central Bank doing the same.

If there’s a silver lining, it’s that, by and large, the world's largest economies will avoid recession. We expect developed economies to grow by 0.8 per cent after expanding 1.5 per cent in 2023, with the US's growth slowing to 0.9 per cent from 2.4 per cent. We think the market is vacillating between a US recession and a soft landing, underestimating the possibility of anaemic growth. At the same time, the fact that there aren’t any clear market bubbles – corporate balance sheets are solid, valuations aren’t excessive and there’s no sign of investor euphoria – any downturn isn’t likely to trigger an ugly negative feedback cycle.

Economic conditions will be considerably better in the emerging world. We see emerging market economies posting robust growth of 3.9 per cent next year, up from 3.7 per cent in 2023 and 2.8 per cent the previous year. That’s likely to be underpinned by China’s recovery from this year’s low point.

Backing bonds

As nominal economic growth slows in the developed world so too will corporate earnings growth, particularly during the first half of the year. But even with a rebound later in the year, we see global equity returns of around 5 per cent for the year, down from double digits in 2023.1

By contrast, bonds should benefit from a drop in inflation and a start to central banks’ easing cycle. We see global bond yields dropping by around 50 basis points, which should deliver investors a 7 per cent total return from basically zero so far this year.2

We see a pause, if not an end to US exceptionalism – a significant shift from what investors have grown used to. The US economy is set to slow dramatically, while Europe is likely to beat investors’ gloomy expectations. With equity valuations depressed within the single currency zone, European stocks have a solid prospect of outperforming during the coming year. Meanwhile, although robust economic growth in emerging markets bodes well for stocks there, the risks in China – the economy is only slowly recovering and remains vulnerable to its highly leveraged property market – tilt us in favour of EM bonds rather than equities.

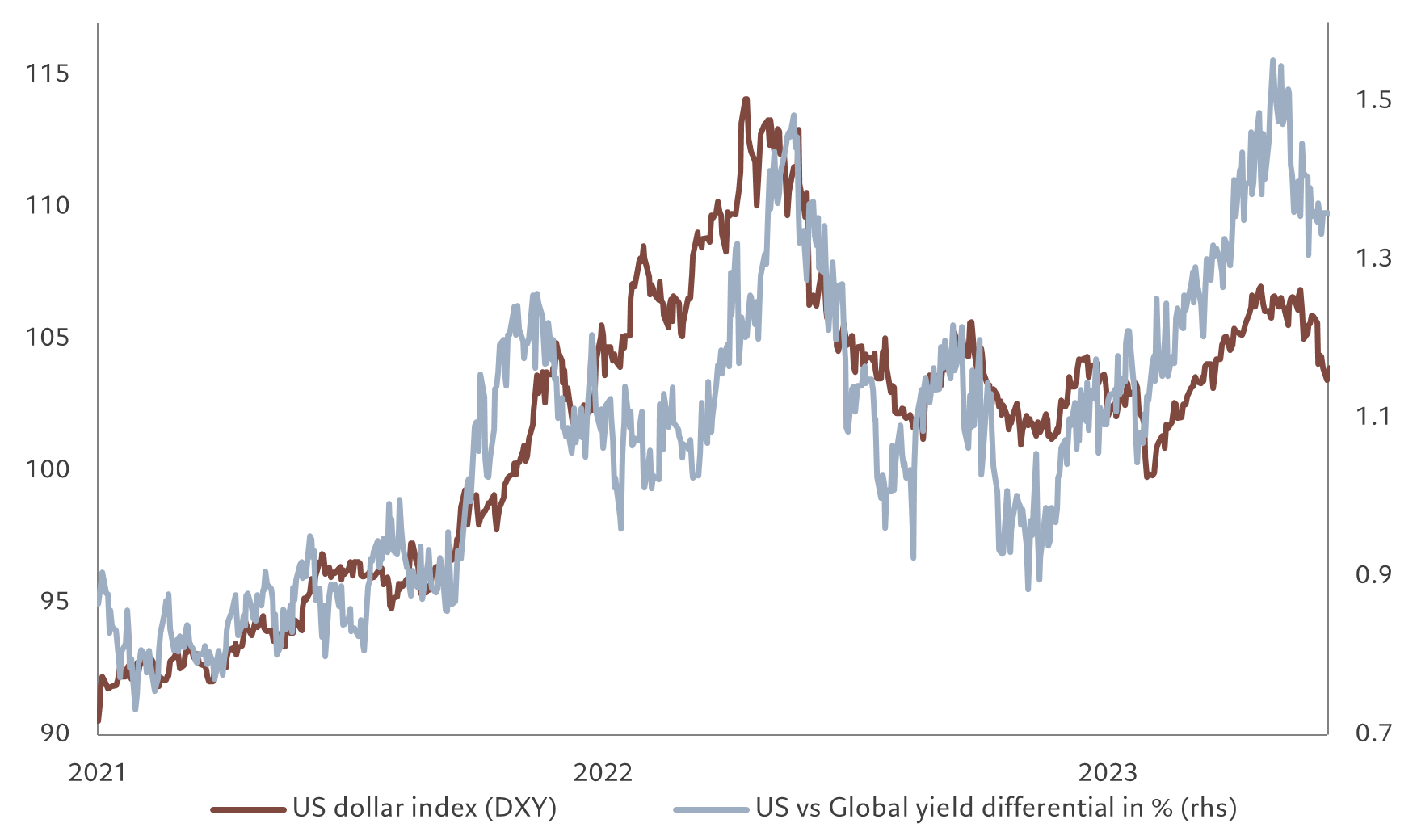

When it comes to currencies, we see the US dollar softening by at least 5 per cent during the year on disappointment with the US economy’s progress and valuation that – on almost any metric- remains well above neutral levels (see Fig. 2).

Among alternatives, we think gold should be well supported by a weak dollar, a peak in US interest rates and lingering geopolitical risks, but the upside appears limited by relatively high valuation on our models. Private equity is being challenged: too much capital is chasing too few attractive opportunities and high interest rates make life hard for leverage-driven businesses.

Tail risks

It would be imprudent, however, to ignore the tail risks to the scenario we set out. There’s a significant likelihood that, in being too eager to bring inflation back to target, central banks over-tighten monetary policy, triggering a recession – the risk of which we estimate at 25 per cent. Alternatively, we figure there’s a 15 per cent chance of stagflation, where inflation reaccelerates even as the economy slows, especially if there’s an energy shock triggered by global events.

Then there are the geopolitical risks. Regional flashpoints are multiplying. There is no sign of a resolution to the Russia-Ukraine conflict. Israel’s war with Hamas in Gaza threatens to become something bigger.

In a nutshell, 2024 will be a good year for investors to focus back on country and sector fundamentals, take a granular approach, with a focus on quality stocks and credits and a higher weighting to sovereign bonds.

Wither US exceptionalism?

Global equities are on track to deliver steady but unspectacular returns in 2024. Having lagged behind the US in recent months, Europe should get its turn to shine. And as global growth edges lower, defensive quality sectors should take the upper hand over more cyclical growth stocks.

Corporate earnings will continue to disappoint as sales growth slows and profit margins come under pressure from higher borrowing costs and rising real wages. Based on our economic models, we forecast global earnings growth at around 4 per cent for next year. That is some 6 percentage points lower than analysts' consensus estimates.

The gap between the market's earnings expectations and our own projections is the most pronounced in the US, where we expect economic growth to slow as interest rate hikes take their toll.

Consumers' excess savings are being depleted, while companies are cutting their capital expenditure. Indeed, our models suggest non-residential investment is heading into contraction territory. As the weaker economy hits corporate earnings, we expect the recent outperformance of US equities to reverse during 2024.

European renaissance

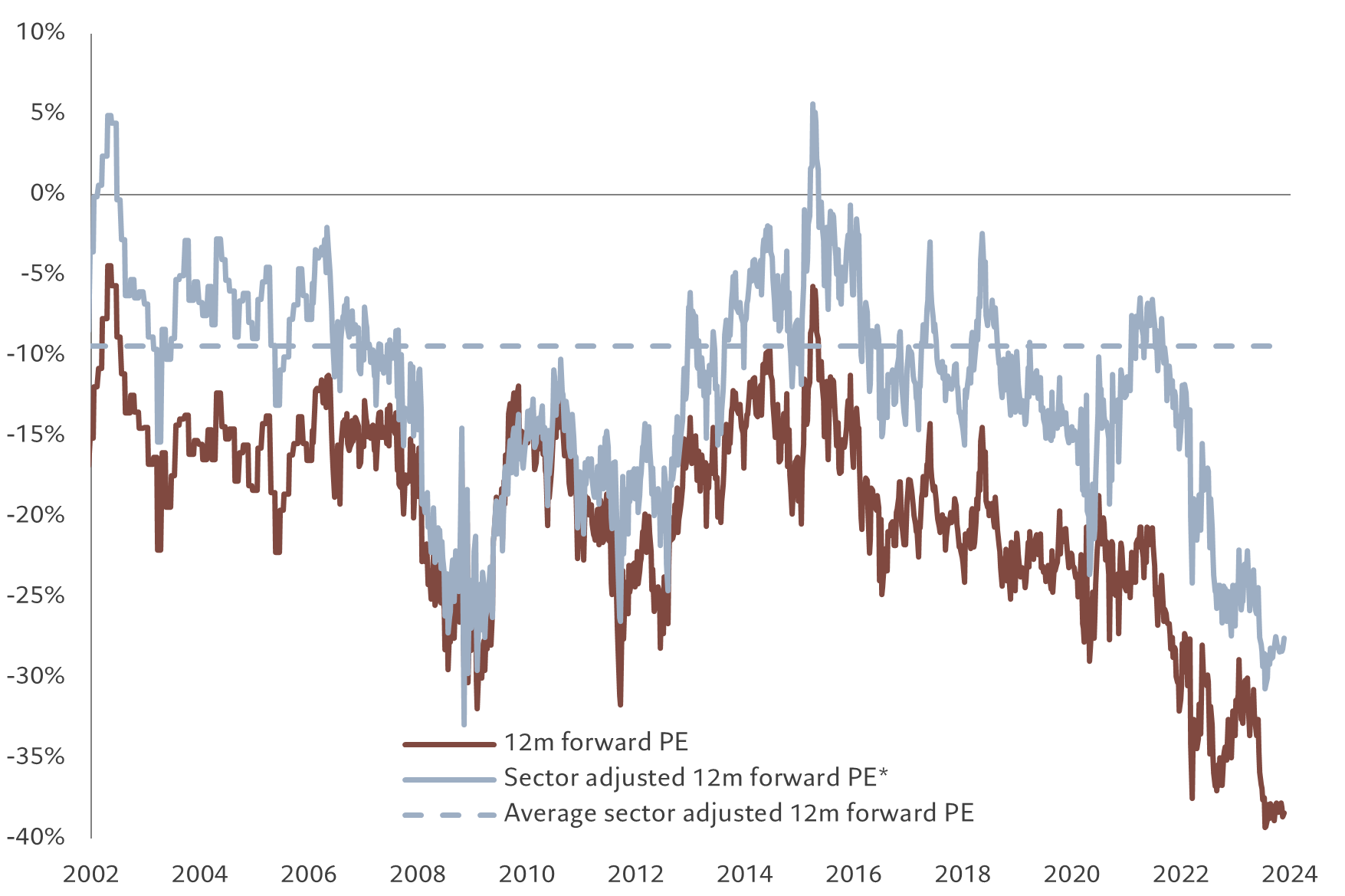

Europe, in contrast, should do better. Earnings expectations there are much more muted, leaving less room for disappointment. Bearish investor sentiment is likely to reverse as the economy recovers – as manufacturing starts to recover, we expect euro zone GDP growth will pick up to 0.7 per cent in 2024, largely in line with US growth compared to 2 percentage points below in 2023. The investment case becomes all the more compelling when you consider valuations and positioning. Europe trades on a 12-month forward price-to-earnings ratio of 12 times, compared to US at 19 times (see Fig. 3). Even adjusted for sector differences such a valuation discount is unprecedented.

MSCI EMU 12-m forward price-earnings ratio ( sector adjusted, equal weighted)

Source: Refinitiv Datastream, MSCI, IBES, Pictet Asset Management. *Sector valuations reweighted to MSCI ACWI weights. Data covering period 01.01.2002-21.11.2023.

We also see potential in Japan, where earnings revisions have held up better than elsewhere in the developed world, and tailwinds of positive corporate governance reform and the economy breaking out of deflation remain in place (for more detail, see: Japan Inc ripe for change)

When it comes to emerging economies, valuations for stocks are relatively attractive according to our framework. However, we have to balance this against growing geopolitical risks and uncertainty over China – in terms of both the outlook for the all important property market and potential for the trade friction with the US remaining on top of mind for investors. We therefore prefer to hold EM exposure via bonds rather than stocks.

Swiss stability

Given the risks stemming from China and beyond, we believe it’s prudent to include some high quality defensive positions within a portfolio.

Switzerland's equity market looks like the only true safe haven in the global economy, benefiting from non-inflationary growth, a strong currency and good fiscal discipline. On the face of it, this all comes at a price – Switzerland is the second most expensive equity market on forward price to earnings measures. However, when you consider its defensive qualities, including some 60 per cent index weighing in healthcare and consumer staples companies, and adjusted for growth prospects, the valuation actually starts to look attractive. Furthermore, the Swiss equities trade below trend relative to domestic bonds, while in the rest of Europe and in the US the opposite is true.

Our defensive stance extends to sector allocation. We retain a preference for quality as a style, keeping in mind the anaemic growth and high interest rates backdrop. We also have a tilt towards value, given the unjustified premium demanded by growth stocks. In our view, analyst expectations are too optimistic for growth and policy priorities over the medium term – such as re-shoring and near-shoring, the green transition and tech regulation – are supportive of the value style.

We are overweight energy as a hedge against an escalation of the conflict in the Middle East. Energy also stands out as the only sector able to match the yield from cash. In communication services we see supportive earnings dynamics and the opportunity to gain exposure to the artificial intelligence theme at a reasonable price.

Global bond markets have never sustained a sustained period of volatility like that of the past two years.

But we believe we’re coming to the end of what some called “the greatest bond bear market of all time” as the prospects for developed and emerging market bond markets are finally brightening.

Global fixed income markets are likely to yield above-average gains for investors next year, thanks to higher coupon income, weaker nominal growth in the global economy and a gradual shift in central bank monetary policies away from aggressive tightening.

As interest rates stand at or near peak for most economies and inflation is likely to decline, albeit gradually and with volatility, some central banks are likely to start cutting interest rates, a process which has already started already in parts of the developing world.

Developed economies are likely to follow suit. We expect the Fed to cut interest rates twice during the latter half of the year, while the BoE could surprise the market by being the first major central bank to cut interest rates as early as May. The ECB is likely to cut interest rates too but less than its US counterpart.

Yields heading south

Government bond yields across major economies are likely to decline by some 50 basis points on average. We expect US benchmark 10-year Treasury yields to end the year at 4 per cent next year, which should lead to total return in global bonds – measured by the JP Morgan Global Aggregate Bond index -- of around 7 per cent in 2024.

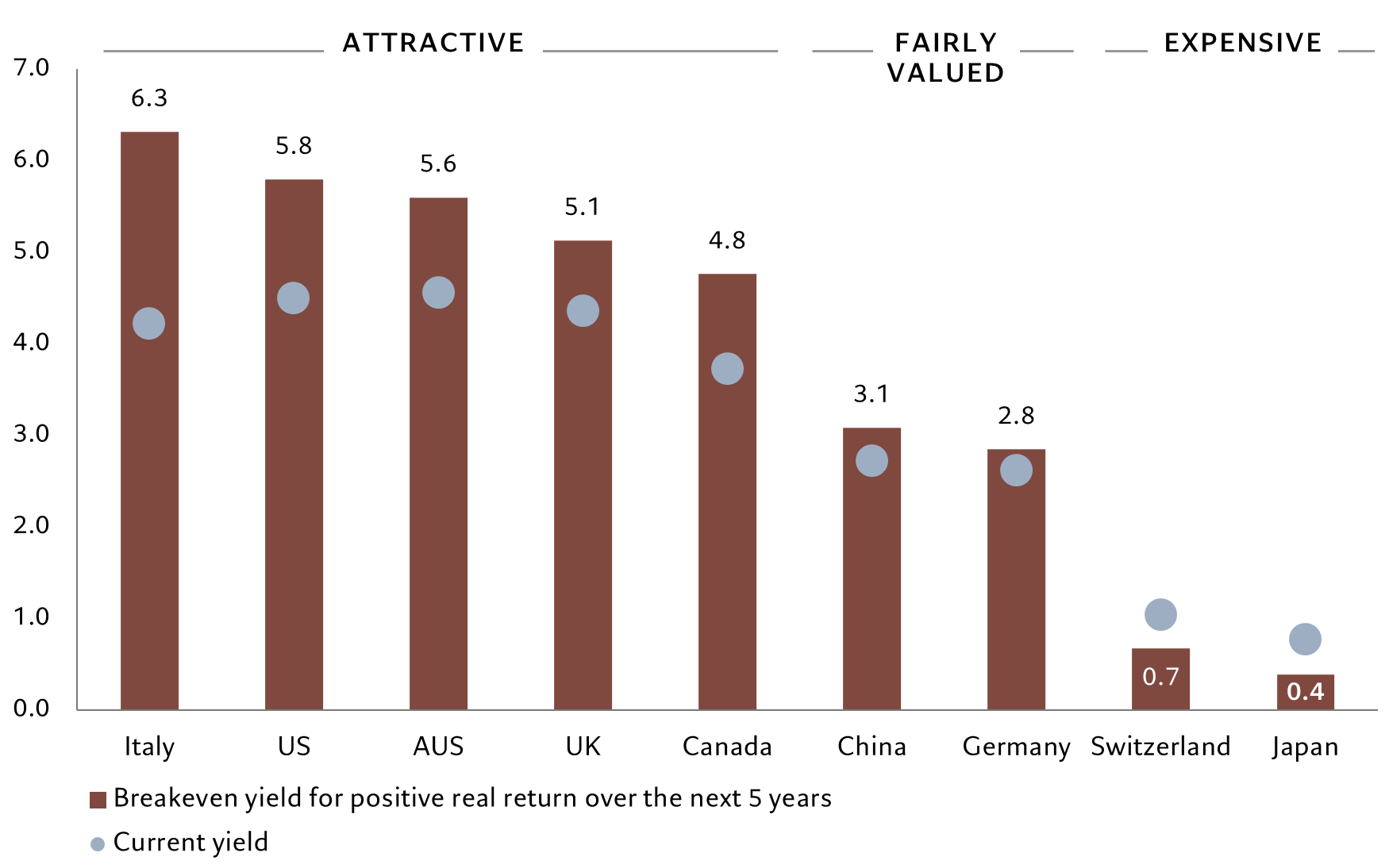

From Italy and the US to UK and Canada, investors in most developed government bonds can expect to secure capital gains after inflation next year. In the US, inflation-protected Treasury bonds (TIPS) look particularly attractive should inflation remain sticky as a result of conflicts in the Middle East.

Japanese and Swiss bond markets are likely to buck the positive trend. They are both low-yielding markets where the outlook for annualised return after inflation – or real yields -- is negative.

Investors should avoid Japanese government bonds in particular as the Bank of Japan appears set to normalise its monetary policy, ending negative interest rates in the new year before raising short-term borrowing costs over the course of 2024. We expect Japan to be the only country that will see its benchmark yields rise between now and end-2024.

Keeping an eye on deficits

The risk for developed market government bonds comes in the form of rising budget deficits and a resulting rise in bond supply.

Already in the US, the Treasury has been boosting the size of auction for bills, notes and bonds to plug a growing gap in the country’s budget deficit, which is worsening in part because of the Fed’s interest rate hikes.

At the same time, its valuation is no longer attractive after global bonds have attracted over USD240 billion of inflows since January, at least twice more than equities did. What is more, a record share of investors in surveys are overweight the asset class and expect bond yields to fall – this could reduce the upside risks to bond prices.

In corporate debt, we like high quality corporate bonds. As we enter a period of softer inflation and slowing growth, we prefer investment grade credit to high yield bonds. US high yield spreads stand at 400 basis points, which are too narrow to be justified given our expectation that default rates are likely to rise above the historical average of 3.6 per cent. According to our calculations, the current spread of 400 basis points is consistent with US GDP growth above 3 per cent, full normalisation of credit standards and well below-average default rates, a scenario that is unlikely to materialise.

Elsewhere, the case for allocating capital to EM bonds is strong, especially in Latin America. EM local currency debt has already benefited from interest rate cuts. Having moved earlier than their developed counterparts to control inflation, emerging central banks are better placed to support growth with easier monetary policy, a cycle which we believe will accelerate.

The prospect of an appreciation in EM currencies means such bonds could gain even more, especially when emerging economies are likely to outgrow their developed peers. We expect the growth gap between the EM and developed world to widen to 3 percentage points next year.

Our models show EM currencies are trading at as much as 20 per cent below fair value. While yield differentials –an important driver of currencies – may narrow in favour of the dollar, we think the emerging world’s superior growth should help their currencies appreciate in the coming year.

EM hard currency debt should also outperform given that its current yield stands at 9 per cent, the highest in the sovereign bond market and some 200 basis points above its 10-year average.

We expect marginal tightening of EM bond spreads, which, coupled with a decline in US yields, should result in a total return well above 10 per cent in 2024.

Dollar decline

In the foreign exchange markets, we expect the dollar to enter a period of a slow but sustained decline. The currency’s yield advantage over its developed market peers will disappear as US GDP growth falls below that of most other developed economies in 2024.

We expect the dollar to fall at least 5 per cent against its basket of currencies next year.

The yen should gain the most from the dollar’s weakness. Its real effective exchange rate is more than 20 per cent below its 10-year average, while on a purchasing power parity basis the Japanese currency is some 40 per cent below its fair value.

Falling US-Japan yield differentials in favour of the yen should help narrow this valuation gap in the coming year.

Gold’s investment appeal is also on the rise. Falling US real rates and a weaker dollar should benefit the precious metal, even though its valuation is no longer attractive after a near 10-per cent gain this year especially in the wake of the Israel-Hamas war.

Source: Pictet Asset Management.

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer. This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.