The joy of absolute return

The emerging market investment case is clear. With developed economies held back by poor demographics and low rates of productivity growth, investors are increasingly turning their sights to the faster-expanding countries of the emerging world (see Fig.1). That EM assets tend to be relatively uncorrelated with developed markets is a further plus.1

The problem is, many investors end up deciding against making an allocation. That's because, for all their attractions, EM assets are all too often undermined by volatility – emerging stocks, bonds and currencies can experience severe bouts of turbulence.

But a solution has emerged. Thanks to the evolution and expansion of EM derivatives markets, investors are now able to access EM investments using an absolute return approach.

This strategy targets a positive return in all market environments by use of long and short positions and the ability to select from a broad canvas of assets – not least in EM fixed income and currencies.

EM alpha

EM sovereign bond and foreign exchange markets are an especially rich potential source of excess investment return. Not only is there significant dispersion within the asset class but EM bonds also tend to be under-researched, particularly outside of the largest government bond markets. That's in contrast to developed market bonds, which now move largely in lockstep.

At the same time, EM bond markets are dominated by long-only investors who closely track broader indices.

Many large institutional investors treat the EM universe as homogeneous, and invest in it using index trackers.

But that can be counter-productive. Those who follow capitalisation-weighted benchmarks risk ending up with worse quality assets as troubled governments borrow more.

For instance, Turkey’s index weighting grew as it issued ever more debt. This left index-tracking investors with ever larger positions in the country even as its eroding economic fundamentals suggested they hold fewer (or none) of its bonds.

Active long-only management doesn't necessarily solve this problem. That’s because most active strategies use established indices as their benchmarks and thus also end up tracking them, even if less closely.

Another reason why investors miss out on EM debt's full benefits is that some are wary of the market's reputation for big and sudden price swings. Many consequently under-allocate to the asset class.

Together, these factors create an environment in which nimble investors with strong analytical skills can generate alpha.

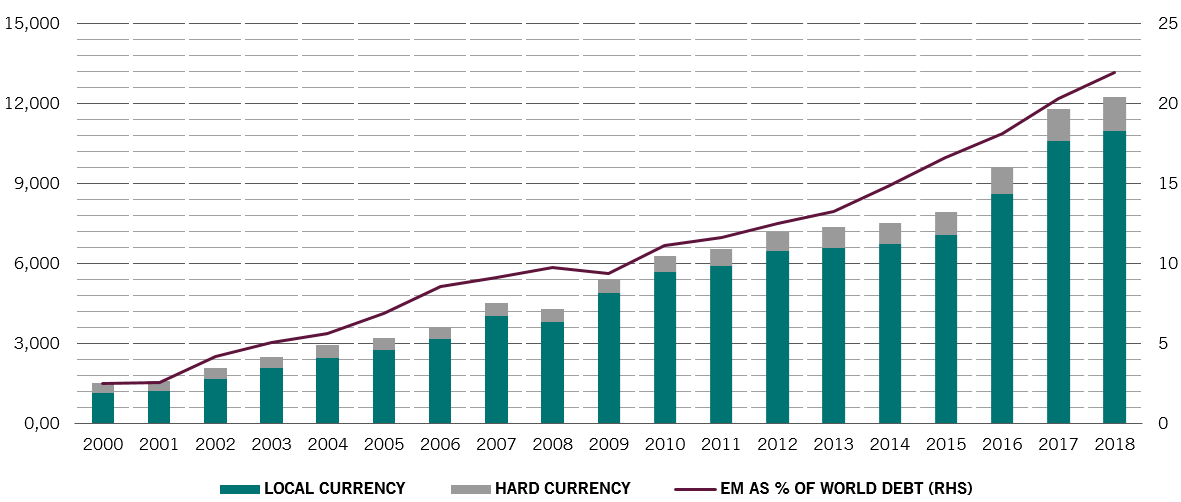

EM government debt in local and hard currency (USD bn) and total EM debt as % of total world debt

One way to mitigate the risk of capital loss and still allow investors to benefit from EM’s potential is to target absolute returns. Absolute return strategies aren’t tethered to benchmarks. Instead they aim to generate positive returns no matter what the broader market is doing. They target excess returns from dispersion and not from trying to solely time market swings.

A true absolute return portfolio isn't a hostage to beta, or market direction. This means constant and close monitoring of positions to ensure adequate diversification – seemingly disparate assets frequently show high levels of correlation in stressed market environments. Absolute return shouldn't mean just chasing yield. For instance, investors blindly drawn to Argentina’s substantial yield spread would have missed the warning signs that recently saw the value of its sovereign bonds halve on political risks.

To achieve returns that are independent of market direction, investment managers running Pictet Asset Management's Sirius strategy apply disciplined risk management and well designed portfolio construction. It's a skill that demands a deep understanding of markets. The strategy also depends on an ability to take short positions; a willingness to commit to conviction trades, albeit sticking to rational position sizes, and, not least, a determination only to trade in liquid assets. In doing so, they are able to generate appealing risk-adjusted returns at all points in the market cycle.

All of which means adding a total return portfolio to an existing EM debt allocation can improve the risk-adjusted return of the entire investment.

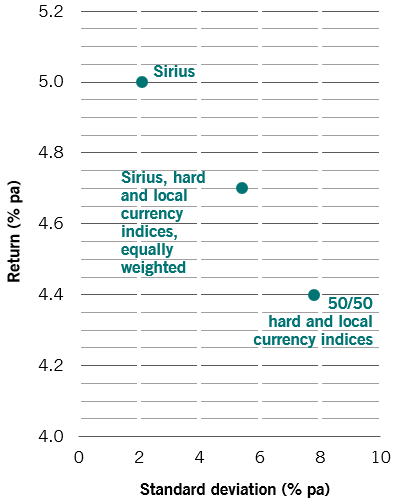

For instance, including Pictet AM's Sirius long-short EM debt strategy from the nearest quarter after its inception to a portfolio made up equally of passive EM hard and local currency debt investments, creating an equally weighted portfolio of the three, would have cut its annualised volatility by a third by the end of the second quarter 2019. It would also have improved returns and significantly reduced maximum market drawdowns [See Fig. 2]2.

Variety

Because broad market moves often overwhelm dispersion within the EM sovereign fixed income universe, it’s easy to underestimate the ever expanding variety of assets on offer. It’s worth noting that this expansion hasn’t come at the expense of quality – an increasing proportion of EM debt is priced in local currencies rather than dollars, helping to make their long-term debt positions more sustainable. And ever more of this debt is being bought by domestic investors, who tend to be stickier bondholders than foreigners.

As the market has matured, so too has the number of derivative instruments. Pictet AM's Sirius strategy selects from among more than 70 sovereign bond markets and related liquid derivatives, interest rates swaps, credit default swaps, interest rate futures, forex and options. This opens up a wealth of possibilities for both macro directional and relative value trading, involving everything from trading big themes that evolve over a year or two, to taking advantage of short-term market dispersion.

Combining Sirius with long-only hard and local currency EM debt allocation.

Indeed, an investor is likely to need a rigorous set of filters to make the right choices. The nature of the asset class means that bottom-up country analysis has to be done through the prism of global macroeconomic factors, from G3 monetary policy to the state of the global economic cycle, capital flows and geopolitical developments. Then by considering how economic data is unfolding, the shape of countries’ interest rate curves and their performance history, investment choices can be narrowed down to a manageable pool of assets.

At that point, individual countries can be viewed in terms of long-, medium- and short-term perspectives. For instance, over the longer term, economic trends and policy and political frameworks matter, while over a middling time horizon, expectations about growth, inflation, monetary and fiscal policy are key. Short term it’s a question of event risks, market positioning, technicals and the outlook for volatility.

Done well, the result can be a portfolio whose returns are uncorrelated not only with major asset classes, but also with benchmark emerging market indices.

Such portfolio should also offer some protection against capital loss while delivering a steady positive return with more alpha than is commonly generated by more heavily-traded assets. All of which means the inclusion of absolute return strategy into a traditional bond portfolio has the potential to improve volatility-adjusted returns.