Asset allocation: guarded optimism

The global economy appears to be on the road to a V-shape recovery from the Covid-induced recession.

Economic activity has been picking up in US and Europe but most rapidly in China, where our real-time indicators show output levels are back at pre-pandemic levels.1

At the same time, although monetary stimulus from central banks may be easing, it remains sufficient to support demand for now.

This is not to say all is rosy.

Investors have no shortage of risks to contend with in the coming months – a resurgence of Covid cases, fears of a new round of lockdowns in Europe and the potential for a disputed US presidential election next month.

Taking all this into account, we have retained a neutral weighting in equities and bonds. Within stocks, we like emerging market and euro zone equities yet, due to the uncertainty regarding Covid-19 and the US election, we have sought some insurance by retaining an overweight on the safe-haven Swiss franc and gold.

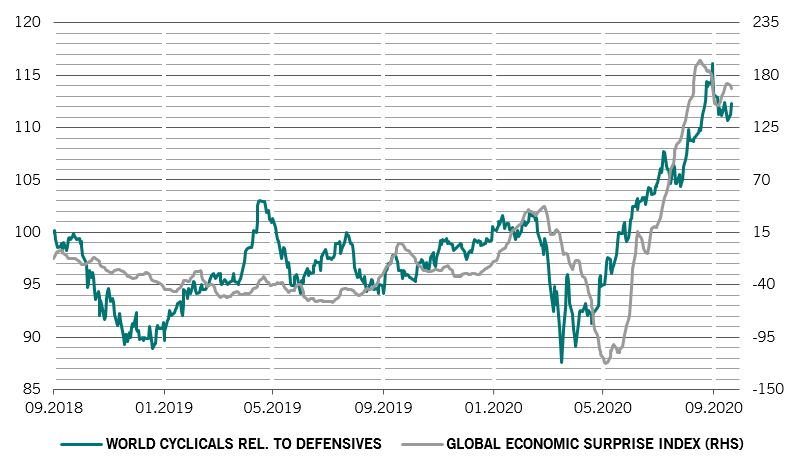

Our business cycle indicators show global industrial activity is nearly back to pre-Covid levels, while spending on services is lagging.

In the US, the recovery is being fuelled by a strong housing market, where record low interest rates have helped push existing home sales to their highest levels in nearly 14 years.

We now expect a smaller contraction in output this year than our previous forecast, which was for a for -4.6 per cent drop. We see GDP growth recovering to 5.5 per cent next year – which is just under the 2019 trend projections.

There are concerns that the forthcoming lapse in US pandemic relief benefits and grants – or what has become known as the “fiscal cliff” – could stall the recovery. But we think the high level of savings among US households, which, as a proportion of net disposable income, hit a record 33 per cent earlier this year, should cushion any shock to the economy.

Recoveries in the euro zone and Japan are modest by comparison. In the euro zone, new restrictions to halt the resurgence in virus infections threaten to derail a recovery in the services industry while retail sales in Japan also remain weak.

Emerging market (EM) economies, led by China, are recovering strongly, thanks to improving global trade – which stands at just 10 per cent below pre-Covid levels. Our leading indicator for EM economic activity has turned positive on a three month basis for the first time this year, outperforming its developed world counterpart which is still in negative territory.

Our liquidity signals are positive for risky assets, with the volume of public and private money supply remaining at a record high of 28 per cent of GDP.2

However, this is likely to represent the peak. Central banks are unlikely to boost monetary stimulus significantly from this point, which should squeeze stocks’ price-to-earnings multiples in the coming months.

What is more, bank lending standards have tightened to levels not seen since the global financial crisis. In the US, for example, a net 71 per cent of banks surveyed by the US Federal Reserve have tightened their lending standards, the highest percentage since 2008. This could spell trouble for financial markets at a time when the coordination between central banks and governments is weakening.

Our valuation gauges continue to show equity prices are stretched, even after the recent fall in stock markets.

The expansion of equity multiples – responsible for almost all of the total return of equities this year – appears to be over.

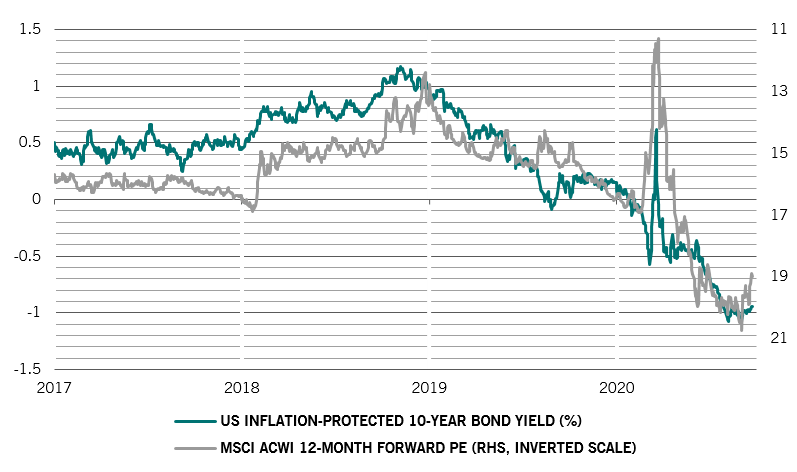

Historically, price-earnings (PE) ratios have had a close relationship with real yields (see chart), where the PE tends to rise when real yields fall. However, real yields, using inflation-linked bond yields as a proxy, seem to have bottomed out at a record low of -1 per cent in the US. What is more, the US Federal Reserve is unlikely to turn much more dovish than it is now.

Investors therefore are unlikely to enjoy the same level of equity gains from the multiple expansion in the coming months. Our models point to an underperformance of stocks to bonds of 5-7 per cent over the next 12 months.

Our technical and sentiment indicators have turned positive for risky assets, partly thanks to seasonality – the tendency for equities to rally towards the end of the year. Although mutual fund data show investors bought USD26 billion of equities last week, the highest weekly amount this year, investor positioning in stocks is not excessively high.

That said, we are mindful of growing political risks surrounding the November US presidential election. Judging from Wall Street’s volatility options pricing, investors are beginning to factor in the possibility of a contested election in November and political turmoil early next year.