Asset allocation: taking precautions

The coronavirus has spread well beyond China and its neighbours, threatening to morph into a global pandemic. Stocks have fallen sharply in response, with the S&P 500 Index this month suffering its steepest weekly fall since the 2008 financial crisis.

In this uncertain climate, we have been shifting to a more defensive footing in recent weeks, taking our equity allocation to underweight while increasing our holdings of cash. Still, that's not to say we expect to remain cautious for an extended period; experience tells us that attractive investment opportunities emerge whenever markets succumb to prolonged indiscriminate selling.

For now, our base case scenario is that the virus outbreak will shave around 0.3 percentage points (ppts) from China’s GDP growth for the whole of this year, taking it down to 5.6 per cent. The impact on the world as a whole will be around half as much, with the global economy now likely to grow by around 2.5 to 2.6 per cent in 2020.

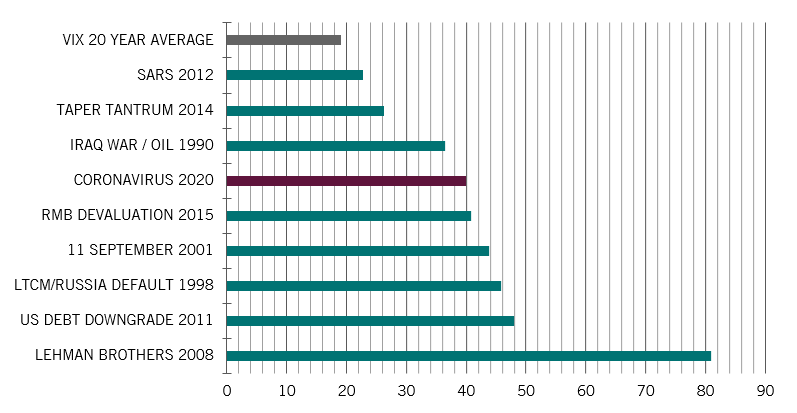

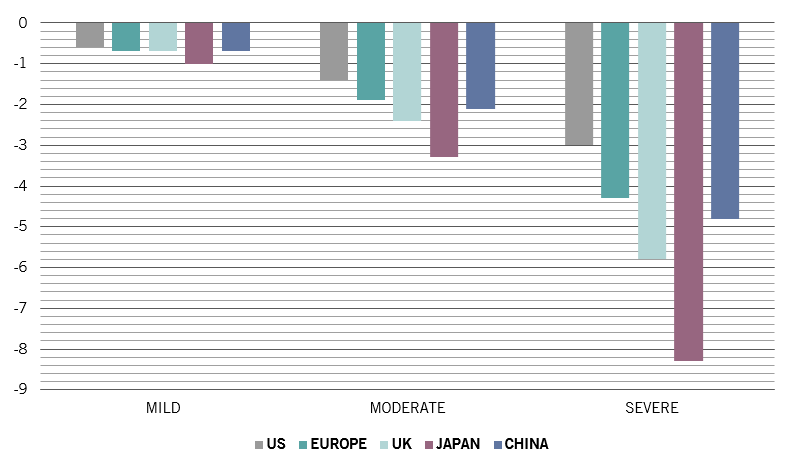

However, the situation could become much more serious if the coronavirus turns into a full-blown pandemic. Academic research suggests that a mild pandemic, like the Hong Kong flu of 1968-9, would trim global economic growth by 0.7 ppts, while a severe one, modelled on the Spanish flu half a century earlier, would slash it by 4.8 ppts – tipping the world into recession (see chart).

Crucially, the impact will be widespread. Japan, potentially, will be more affected than China; Europe and UK could also suffer a heavy blow.

So far, the impact has yet to emerge in our business cycle models. And, arguably, from an economic point of view there is a saving grace in the fact that the world has been looking relatively healthy before the virus hit.

What's encouraging is that central banks and governments around the world are already stepping in to try and limit the economic damage. China is in a particularly strong position thanks to the big role of the state in the economy, which gives it the power, for example, to cut energy prices and to order large banks to support small and medium-sized enterprises in affected regions through extended or subsidised loans.

Our models show that the total liquidity flow1 in China is currently running at around 18.9 per cent of GDP, well below the long-term average of 31.1 per cent of GDP, which leaves plenty of room for more stimulus. The US can also provide more liquidity injections – based on past easing cycles, if the situation demands it we see potential for as much as 150 basis points worth of rate cuts from the US Federal Reserve.

Japan and Europe both have more limited room for manoeuvre in terms of monetary policy, yet are both already feeling the impact of the coronavirus.

Looking through the prism of valuations, the outbreak came at a bad time – equities in particular were expensive, with both US and global indices setting fresh all-time highs at the start of 2020. The subsequent sell-off has reduced some of the exuberance: the MSCI All-Country World Index now looks fairly valued according to our models, with a price-to-book ratio, at 2.2 times, in line with the 20-year average.

Technical indicators suggest the sell-off could continue. Investor surveys still show a degree of complacency. Surveys show investors remain overweight stocks, and there are few signs that equities are 'oversold' However, positive seasonal factors – stocks tend to do well from March to May – could help limit losses.