Asset Allocation: wary about the optimism

As lockdowns are lifted and economies start to revive almost everywhere, it would be easy to assume risk assets were vindicated in rallying sharply since their late-March lows. But we think it is premature to argue that the crisis is over and that the world is heading into a V-shaped recovery. Which is why we maintain our neutral stance on the major asset classes.

Risks are balanced. For all the optimism generated by falling infection and death rates in much of the world and enthusiasm for fiscal and monetary stimulus, the possibility of a significant second wave of the Covid pandemic later in the year can’t be discounted. At the same time, businesses face carrying heavy new burdens – such as having to restructure the way they operate to meet social distancing guidelines – for some time.

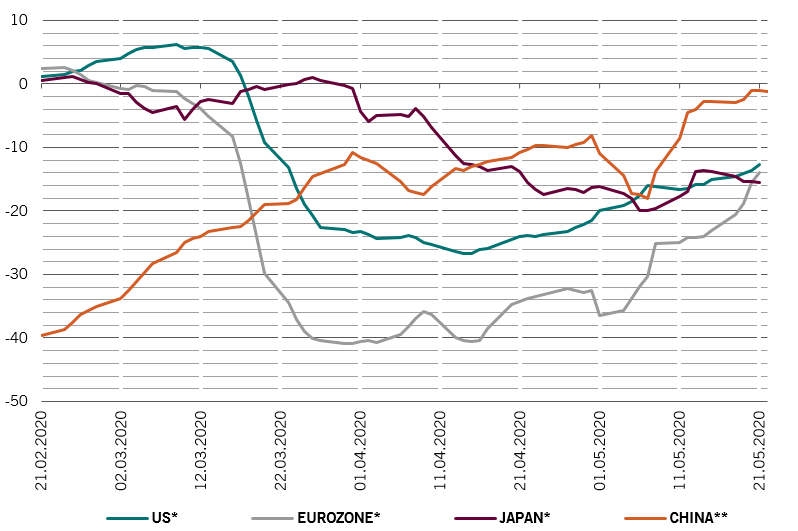

To be sure, our business cycle indicators show that economies across the world have picked themselves off the floor. Daily activity trackers from the likes of Google and Apple show most developed countries are edging towards normality, halving the declines suffered during their March and April lows, with the euro zone now down some 24 per cent below pre-Covid levels and the US and Japan down around 15 per cent. China is back to January levels, though the country’s unique policy circumstances – both to lockdown and stimulus – mean it might not be a template for elsewhere.

Huge job losses – the unemployment rate is likely to peak well above 20 per cent – have hit US consumption. We expect a 12 per cent peak-to-trough decline in consumer spending. This, however, will be mitigated by massive fiscal stimulus. The US fiscal deficit is off the charts, and is likely to reach USD4 trillion this year, some 20 per cent of GDP, without even taking into account the various spending programmes winding their way through Congress. Some 90 per cent of that increase is being financed by the US Federal Reserve.

The euro zone has, hitherto, been more conservative in its approach. But a new EUR750 billion rescue programme (a mix of grants and loans), to be funded through a commonly issued bond, is a big first step towards fiscal integration of the single currency region. This, ultimately, could be even more important than short-term rescue measures and represents a great step forward for the single currency region, especially in light of the lack of solidarity among member countries at the start of the crisis. Even if the plan is watered down - as seems likely - the Franco-German programme could change the bloc's medium and long-term economic prospects.

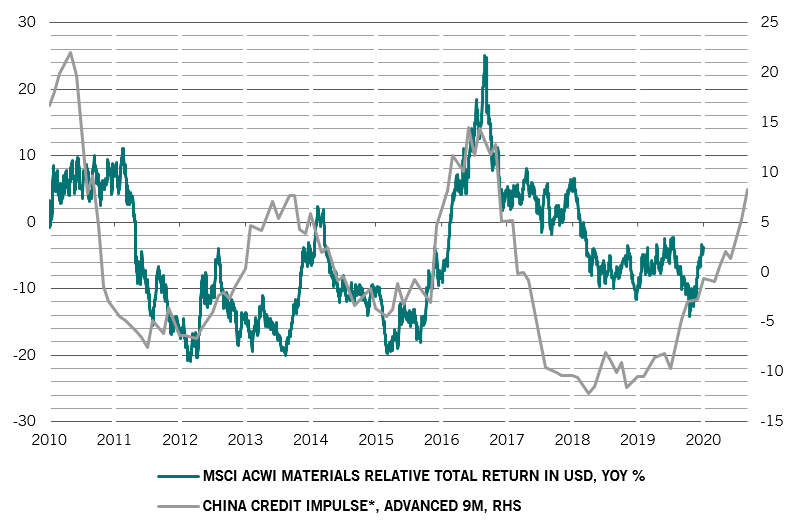

Emerging markets, underpinned by China and India, are likely to suffer less of a drop in growth than their developed counterparts, but we see world growth down 3.6 per cent this year, with a peak-to-trough drop of 8 per cent, double the global financial crisis slump.

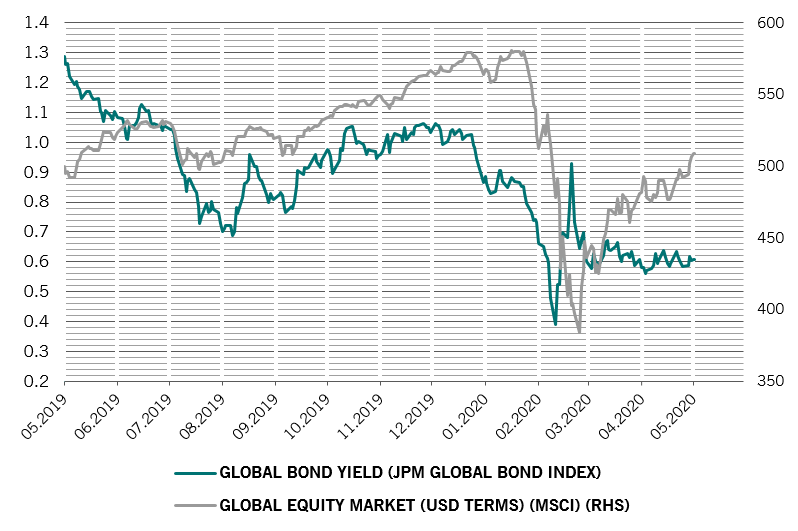

Markets are pricing in a permanent decline in the cost of capital rather than focusing on income and earnings, which is boosting valuations. After a 30 per cent rally from their March lows, equities are now back to fair value while bonds are their most expensive ever. Relative to bonds, equities have some marginal upside. However, absolute valuations matter and in some markets like the US, multiples are very high, even on trend earnings, never mind the hit the Covid crisis and its aftereffects is likely to cause profits – we expect a 40 per cent decline this year, almost twice the consensus. Dispersion of valuations is extreme within asset classes, but the relative rankings of both equity regions and sectors is similar to pre-Covid levels.

Our technical indicators suggest a possible correction for equities, while negative seasonal effects represent a headwind for risk assets. Sentiment has returned to normal levels, but it’s worth noting that retail investors had never fully capitulated, which is typical of severe bear markets. Surveys suggest widespread scepticism of this rally among professional investors, who continue to hold high cash levels.