[1] Credit Suisse Research Institute, “The CS Family 1000 in 2018,” September 2018.

[2] Schwass, J. “Family businesses: successes and failures,” IMD Global Family Business Centre

[3] Bhagat, S. and Black, B. “Board independence and long-term firm performance”, February, 2000

When family values bring shareholder value

Family businesses can be an attractive investment prospect for investors, but capturing these opportunities requires an active approach.

Written by

Cyril Benier

Senior Investment Manager

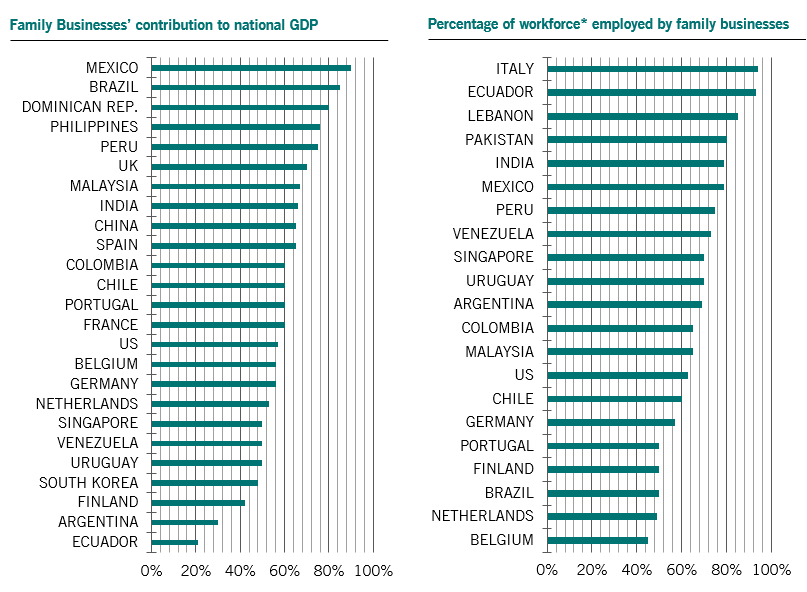

Family businesses are the backbone of the global economy. They contribute between 50 per cent and 70 per cent of countries' gross domestic product and employ the majority of their workforces. But there’s a widespread misapprehension that these companies are just small, local operations and so largely inaccessible to investors. Nothing could be further from the truth.

There are in fact hundreds of listed companies that count founding families as shareholders. They operate in every global industry and sector and come in various sizes – large, mid and small cap – and are held by a wide range of professional and non-professional investors. They are as diverse as Hermes, Dassault Systems, CGI and JD.com. Many have taken on outside finance in order to grow or meet inheritance tax liabilities or to allow family members who wish to pursue other interests to cash out.

Society's true backbone, both economically and socially

Although there is no consensus as to what constitutes a family business, we at Pictet Asset Management believe the label should apply when a family or founder has a controlling stake in the company. We define this as the family or founder holding 30% of voting rights. The 30 per cent figure might seem arbitrary at first glance, but it is based on the fact that, on average, only 60 per cent of eligible shareholder votes are cast at any one time.

The family factor

This definition opens up a universe of high-quality companies to investors. A number of studies have shown that family-owned publicly-traded companies have historically tended to outperform the wider market, including a recent piece by Credit Suisse1.

According to this reseach1, family-owned public companies have stronger revenue growth than their peers, which tends to result in outsized shareholder returns. Family companies also have better margins – 190 basis points vs 150bps. And they have more conservative balance sheets, with 22 per cent lower gearing.

Financial commitment

An unparalleled dedication to disciplined growth

This isn’t down to a small company, sectoral or regional effect. Family-owned businesses tend to outperform their non-family peers, even when results are adjusted for each of these factors.

So why do family businesses outperform?

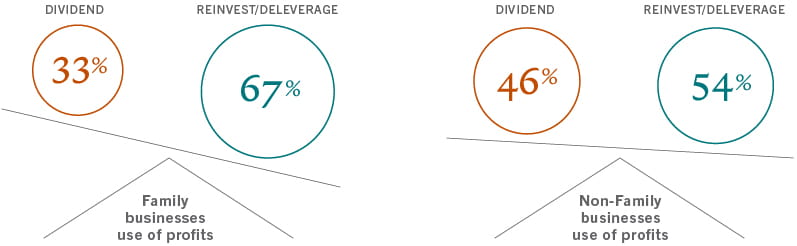

We believe there are three primary reasons. First, because the families tend to have most of their wealth and reputations invested in these companies, their interests are closely aligned. This, in turn, leads to the second reason, that family businesses often reinvest a larger proportion of their profits than their peers. Finally, stability of ownership also allows management to take a long-term view, rather than obsessing about the next quarter's profits. Their capital expenditure as a proportion of depreciation is higher than average.History has shown that family businesses operate with stricter financial discipline while at the same time making better investments.

Despite all this, many investors continue to shy away from listed family-controlled companies. Concerns often centre on the liquidity of the investment and the quality of the governance structure.

But such worries are often misplaced.

Even by Pictet AM’s stringent criteria – 30 per cent family ownership and a minimum of USD5 million daily stock exchange liquidity – there are some 500 companies globally that qualify as listed family businesses.

In terms of governance, it is clear that close monitoring is needed when there is a high degree of concentration of influence2. For example, some investors argue for increased independence of corporate boards – but we believe this could negate some of the advantages of family ownerships. Indeed, research shows that, within family businesses, greater board independence doesn’t improve company performance, all other things being equal3. Instead, independence and strong leadership of the firm’s audit, remuneration and nomination committees are as essential as checks against powerful family board presence.

Other common issues that can arise from concentrated ownership includes damaging family squabbles, or inadequate succession planning. Here too, it’s a matter of closely researching the company’s legal structure and any other governance agreements and ensuring that they’re being followed.

Investors also need to be aware that, although family-owned businesses run the gamut of small to mega-cap, are found across developed and emerging markets and across sectors, they don’t mirror the wider market. They are more heavily weighted towards consumer discretionary, communications and consumer staples sectors – there are fewer such firms operating in finance and energy.

So while family-owned businesses are attractive prospects for investors, getting the most out of them – which is to say, avoiding hazards and maintaining a well balanced portfolio – necessitates close analysis and a well calibrated, active approach.

Acknowledgements

Alain Caffort and Cyril Benier contributed to this article.Read more on family

Pictet-Family – Fund manager interview

Pictet Asset Management has developed a new investment strategy that invests in listed family businesses, companies that count founding families as major shareholders.

September 2020

In turbulent times, family businesses must stick to certain core principles

As the Professor of Family Business and Entrepreneurship at IMD Business School in Lausanne, Peter Vogel has dedicated his professional life to understanding the unique intricacies of family businesses around the world.

October 2020

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer. This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.