Asset allocation: vaccine a boost but not a cure-all

There is light at the end of the Covid tunnel.

Rapid progress in the development of a vaccine and the formal start of US President-elect Joe Biden’s transition to the White House have helped boost prospects for the global economy and corporate profits.

That said, investors should not get ahead of themselves. Economic activity, especially in developed economies, is expected to recover only gradually in the coming weeks; Covid cases are still surging in the US and the chance of a third wave of the pandemic in Europe cannot be ruled out.

Because of such risks, we are maintaining our neutral stance on equities and non-investment grade bonds.

Our business cycle indicators show the global economy is on track for a strong recovery from the second quarter of 2021 onwards, thanks in large part to an improvement in conditions in the US and China.

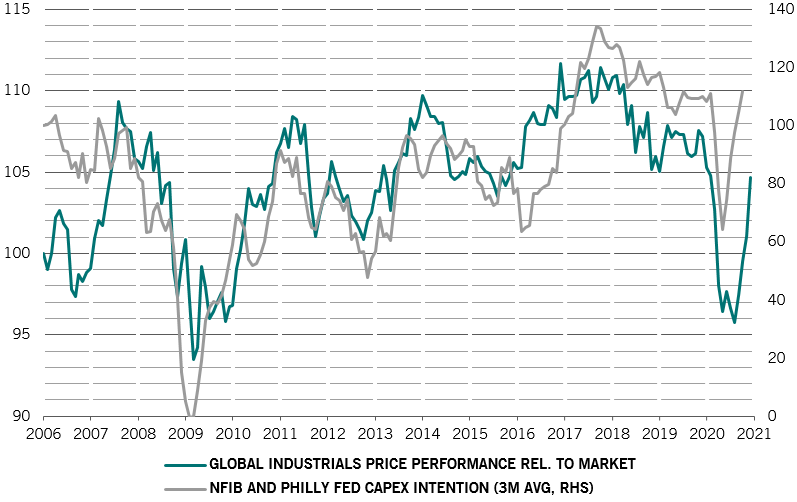

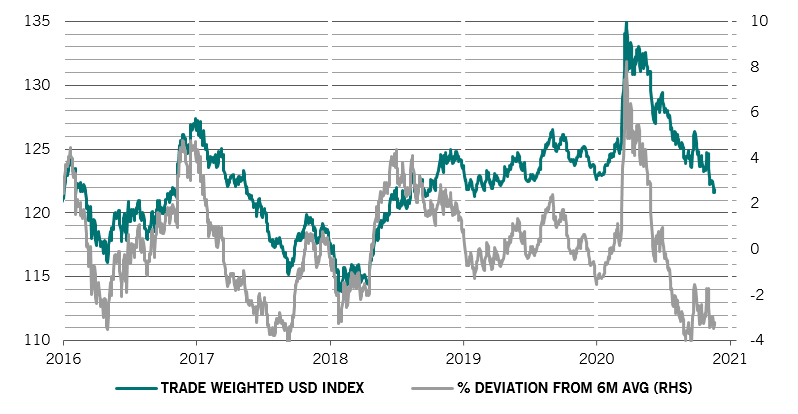

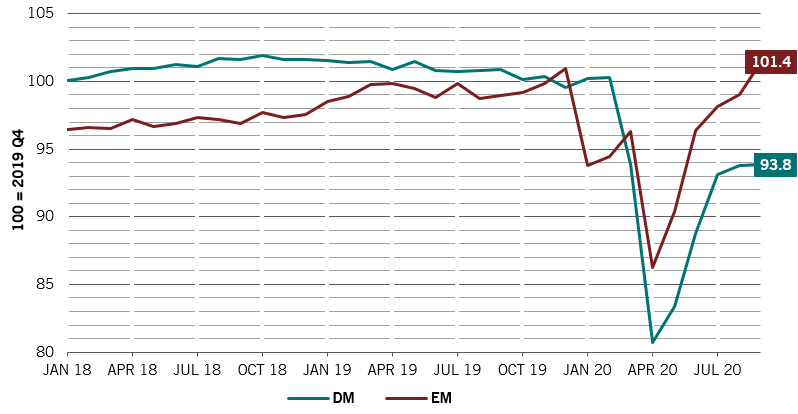

The gap in the economic growth rates of emerging and developed nations is widening with developing world industrial production recovering to above pre-Covid levels (see Fig. 2). This differential could grow further if global trade continues to improve and the US dollar resumes its descent.

In the US, a buoyant housing market is leading the recovery, while surprisingly upbeat capital goods orders data point to a rebound in business investment. Corporations – and households – have amassed historically high levels of cash, which they are sure to deploy if their confidence grows.

Developments in Washington, where lawmakers are negotiating the size and scope of the next coronavirus relief programme, will also be crucial.

President-elect Biden’s selection of former US Federal Reserve chair Janet Yellen as Treasury Secretary could pave the way for aggressive fiscal stimulus. Yellen has consistently maintained that interest rates should remain low for longer – a stance that we believe is compatible with ample fiscal stimulus.

We expect that even a scaled-down version of Biden’s stimulus plan would be enough to lift real personal consumption growth to 6.5 per cent in 2021 from current estimates of 5.3 per cent.

Our liquidity analysis shows conditions are still positive for riskier assets, albeit less so compared with a few months ago. The volume of global monetary stimulus injected into the financial system as a proportion of GDP has fallen to 18 per cent from an August peak of 29 per cent, as central bank emergency money printing and state-guaranteed credit creation slow.1

Private lending is also stalling. In the euro zone, the European Central Bank’s third-quarter survey showed significant tightening in banks’ credit standards and that demand for corporate loans remained weak.

Valuation signals are flashing red for equities after a recent rally has taken major indices to record highs and pushed earnings multiples for global stocks to above 19, compared with a long-term average of 15.

We expect stocks’ earnings multiples to contract 15 per cent next year, in tandem with a decline in excess liquidity-- or the difference between the rate of increase in money supply and nominal GDP growth. Our analysis indicates an enduring relationship between the two. Still, the contraction in multiples should be offset by what we see as a 25 per cent rise in corporate earnings in 2021.

Bonds are expensive in the main. We believe that will remain the case as central bank policies cap yields; the market is pricing no interest rate hikes at all in the next four years for any of the world’s major economies.

Sentiment and technical readings are marginally positive for both equities and bonds. Equities may have seen a significant USD71 billion in investment flows in the past two weeks, but this comes after a long period in which flows have been lacklustre.