Asset allocation: turning less pessimistic

Trade wars are dominating the summer headlines, yet the global economy and markets remain surprisingly resilient. Corporate earnings are strong, particularly in the US, leading indicators have bottomed out, inflation seems to have peaked and China’s fiscal and monetary authorities have once again started stimulating the economy.

This improvement in economic and financial conditions has, in turn, prompted us to rethink our overall stance on equities – we’ve lifted them to neutral from underweight and trimmed bonds to neutral from overweight.

August 2018

We decided against taking a more aggressive stance on equities for a number of reasons.

The first is trade. We remain concerned about longer-term prospects, however. Trade wars tend to be bad for growth and we think that if US President Donald Trump presses on with punishing tariffs, particularly against Chinese and European exporters, there are bound to be negative economic repercussions. US levies are expected to affect between USD500 billion and USD700 billion worth of trade, though some estimates figure the total could rise as high as USD900 billion.

Second, the US Federal Reserve shows no sign of being derailed from its aim of reversing monetary stimulus. The two policies could yet produce, if not a perfect storm, then certainly an unpleasant one for the world economy.

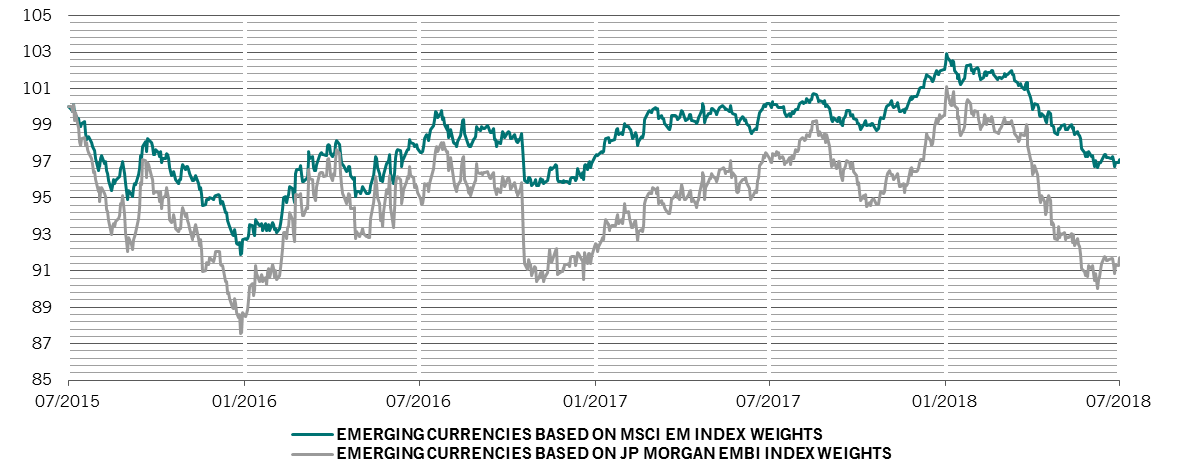

Still, our business cycle indicators suggest that for now the global economy’s recent deceleration might have run its course. Emerging markets leading indicators have, on the whole, improved. These were led by a significant rebound in China, where the easing of both fiscal and monetary conditions, as well as a recent dramatic devaluation of the yuan are supporting growth. There is, however, a risk that the pick-up in Chinese manufacturing activity could be short-lived, having been driven by production brought forward before US tariffs start to bite.

Developed economies are still running at below trend growth. But they have shown some improvement (except for the euro zone which has deteriorated during the past month).

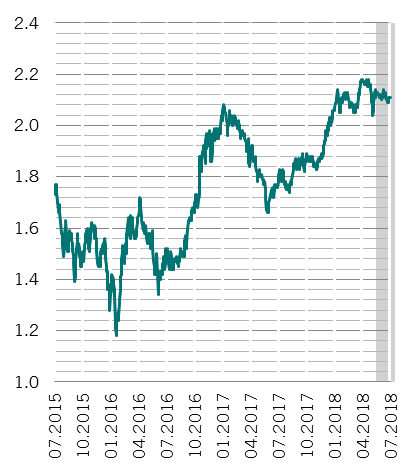

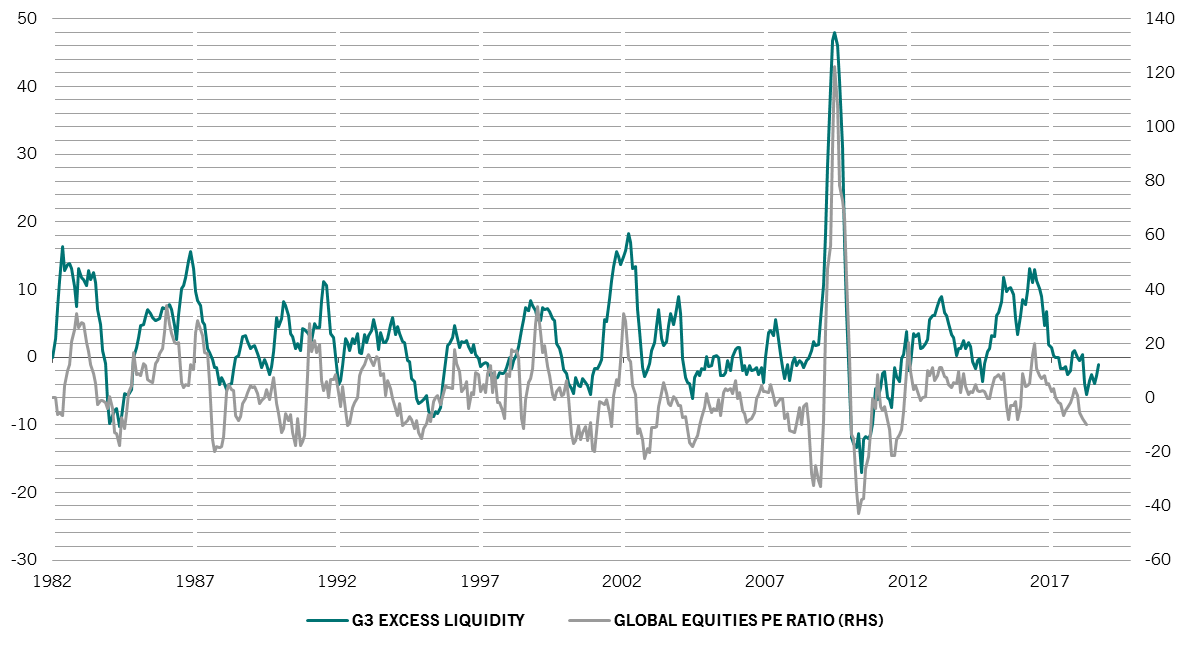

Excess G3 liquidity and global equity PE ratios, 6m % change

One of the key factors behind our more optimistic tilt on equities this month was an improvement in two key components of our liquidity model. In the US, private liquidity growth, possibly driven by corporate repatriation of money held abroad, is offsetting Fed tightening. We observe that the growth of private liquidity, particularly bank credit, is in fact broad based across regions. Meanwhile, in China, the one region where private liquidity isn’t growing, the central bank has been easing policy.

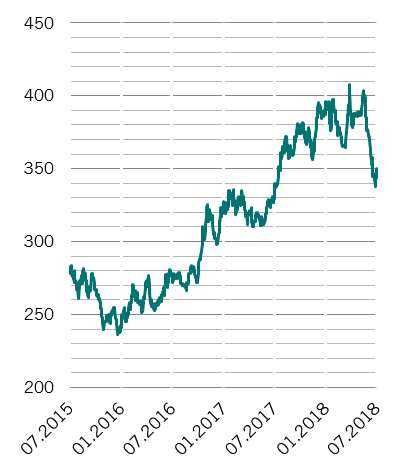

A less negative stance on equities is also supported by our valuation metrics. Not only has the second quarter produced the best results season ever for US corporates, but other markets are also starting to catch up – the positive earnings story is filtering through to the rest of the world.

Technicals offer no clear trends, with few offsets from sentiment indicators. There, recent flows suggest the rout in emerging debt and equity is coming to an end. On balance, though, technicals are neutral for equities with negative seasonal effects in play through the summer months.