Asset allocation: too far too fast

With a slowing global economy at risk of being undermined further by the various trade spats initiated by US President Donald Trump, the US Federal Reserve once again made its presence felt in global markets. One after another, Fed policymakers indicated that the central bank was prepared to insure against a serious downturn with pre-emptive rate cuts, helping lift global equities and bonds by some 6 per cent and 1 per cent respectively on the month.

The market is now discounting a full percentage point of rate cuts over the coming 12 months, starting with a reduction in July. Not only is the S&P 500 index back near record highs, but more than USD12 trillion of global debt is trading at negative yields.

In our view, however, the euphoria over US interest rate cuts is overdone – the first rate cut could well be delayed until September.

As a result we’re downgrading bonds and are now underweight both fixed income and equity; we have also raised our weighting to cash.

July 2019

The Fed’s new dovishness has to be set against a US economic backdrop that remains relatively positive.

True, our own leading indicator has been weakening since the end of last year. But lately, construction activity has picked up, employment remains robust and car sales are showing sign of a tentative rebound.

While our business cycle indicators continue to show the global economy is slowing, they don’t suggest a hard landing. China-US trade tensions are hurting both economies, but some degree of policy response in both countries – even if less than the market expects – looks set to mitigate any weakness.

For technical reasons related to quantitative easing, the inversion of the US yield curve could well be overstating risks the economy falls into recession during the next year or two.

Meanwhile, other economies are benefiting from the China-US spat. Vietnam, Taiwan and South Korea have picked up a significant amount of China’s lost business and Chinese firms have increasingly switched to Latin America from the US for their agricultural imports.

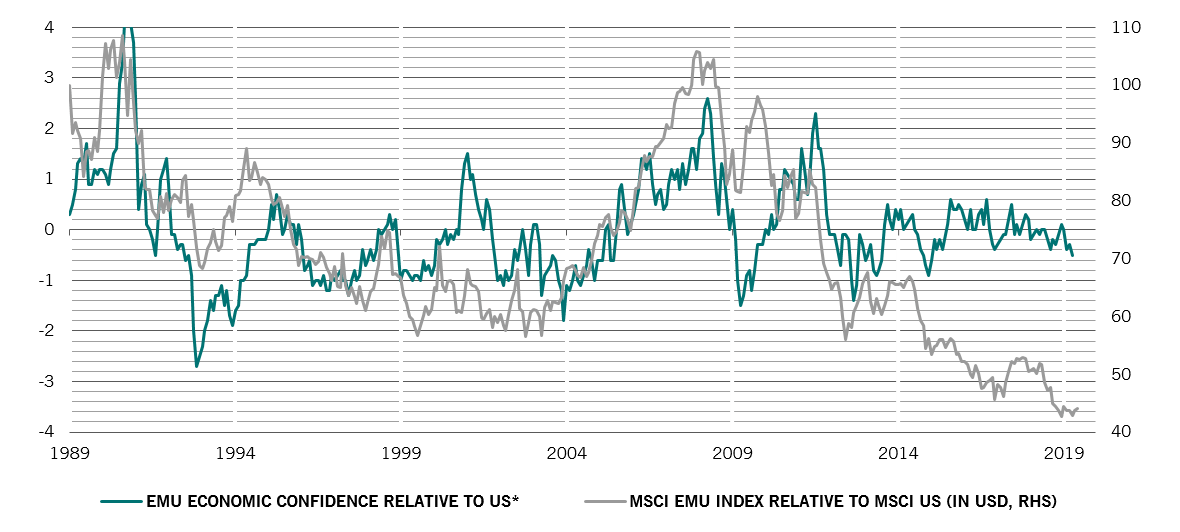

Notably, the euro zone’s outlook has been improving – and that’s even before European Central Bank President Mario Draghi’s delivers on a renewed commitment to provide stimulus as and when needed.

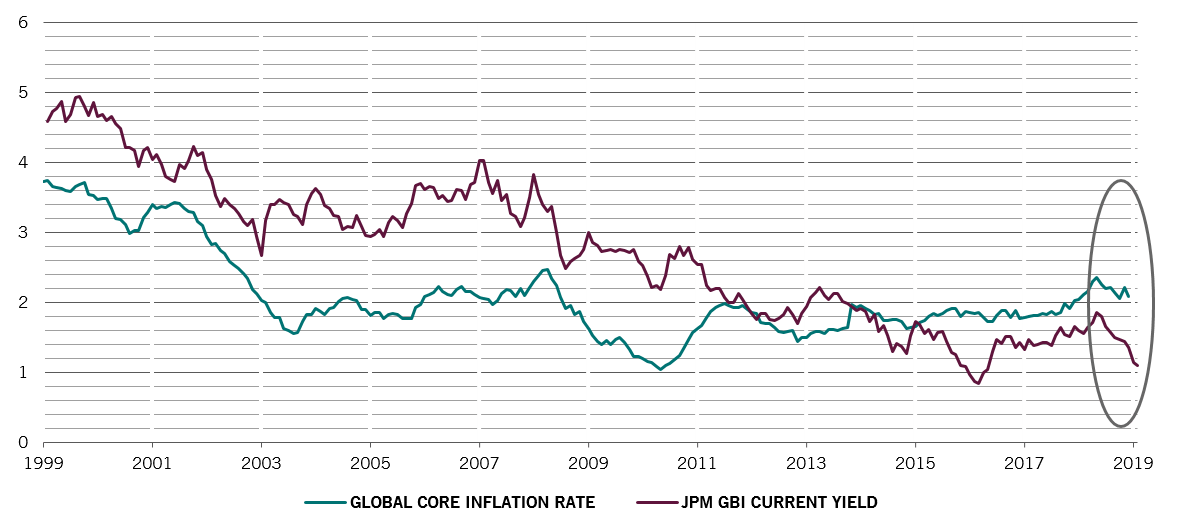

Global inflation versus bond yields, %

Our liquidity analysis offers a reason for optimism. Should the Fed meet the market’s expectations on policy easing, other central banks may follow as they seek to keep their currencies from appreciating and thus hurting their trade competitiveness. That public sector boost would reinforce growing private sector liquidity provision, with credit edging higher across all major regions.

Valuations are flashing red for bonds. Euro zone and Swiss bonds are the most expensive they’ve ever been. Indeed, apart from US investment grade credit and emerging market local currency debt, which are only just in neutral valuation territory, every other asset in the fixed income universe is overvalued.

Elsewhere, despite their strong run during the month, global equities broadly look fairly priced. Still, with the earnings outlook looking considerably weaker than analysts have forecast – we see no growth in earnings over the coming 12 months against consensus expectations of about 7 per cent - stocks remain vulnerable.

Technicals offer support for bonds, which benefit from strong seasonal trends. And despite their big rally, they still don’t look overbought, according to the investor positioning indicators we monitor. As for equities, the trend is neutral and seasonality is negative, but they remains a curiously unloved investments. This relatively light positioning in equities among investors suggests any selloff in shares is likely to be limited. Meanwhile, gold, the strongest performing asset during the month, should continue to be supported by strong seasonality, while it too isn’t yet overbought.