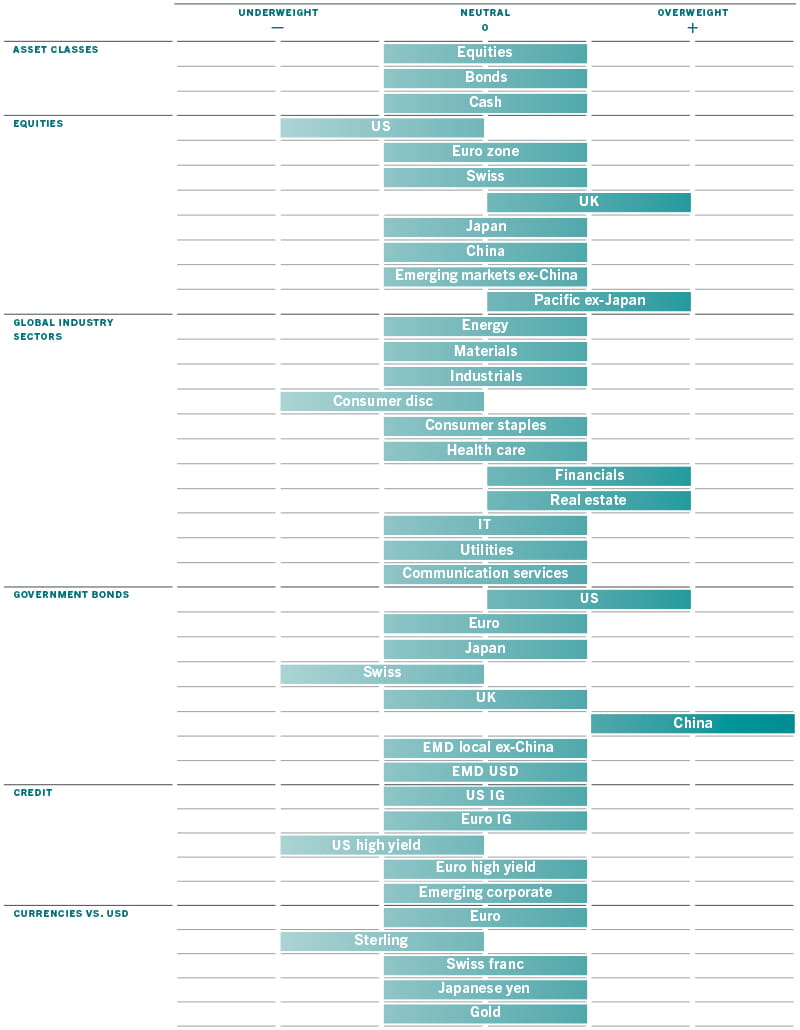

Asset allocation: strong growth, but strong inflation too

The global economy is expanding at a solid pace. Developed countries are responsible for much of that growth thanks to the rapid vaccine rollout and the lifting of lockdown measures.

But economic momentum is beginning to ease as central banks prepare themselves to scale back monetary stimulus in response to rising price pressures.

A less favourable mix of growth and inflation, tighter liquidity conditions and high valuations for riskier asset classes lead us to maintain our neutral stance on equities.

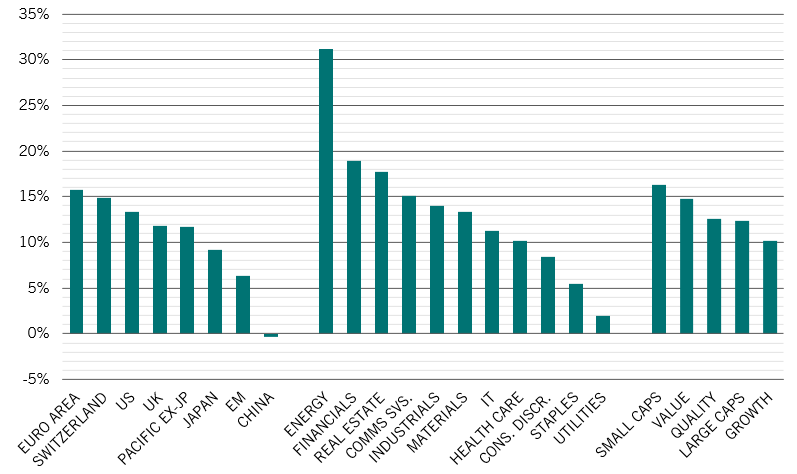

Within equities, we are underweight economically-sensitive sectors - including consumer discretionary stocks – while in fixed income we are underweight riskier bonds such as US high yield debt.

At the same time, we continue to hold overweight positions in defensive assets such as US Treasuries and Chinese local currency bonds.

July 2021

Source: Pictet Asset Management

Our business cycle analysis shows price pressures are becoming more visible in the US.

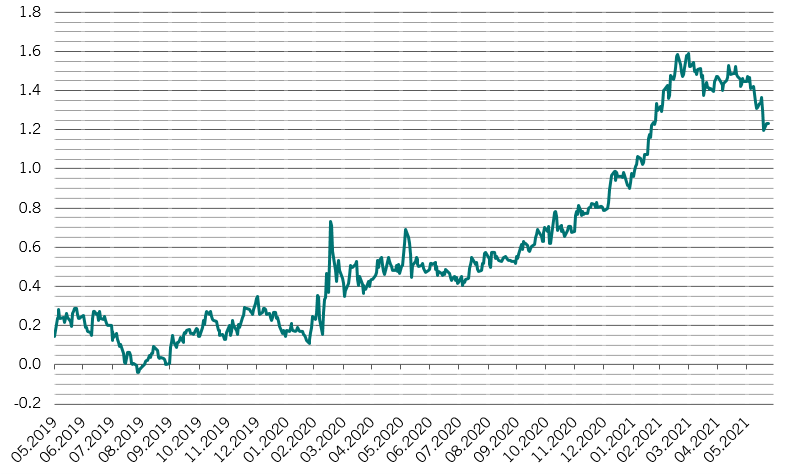

The country’s consumer price index excluding food and energy is increasing at a 3-month annualised pace of 8.2 per cent, the highest since 1982.

Core PCE, the US Federal Reserve’s preferred measure of inflation, also rose 3.4 per cent to hit its highest level in nearly 30 years.

However, we believe the bout of inflationary pressure is transitory, owing to supply distortions and a surge in demand for items that were most affected by the pandemic, such as used cars.

Stripping out the impact from these Covid-sensitive items and the base effect, our analysis shows inflation is still stable at around 1.6 per cent.1

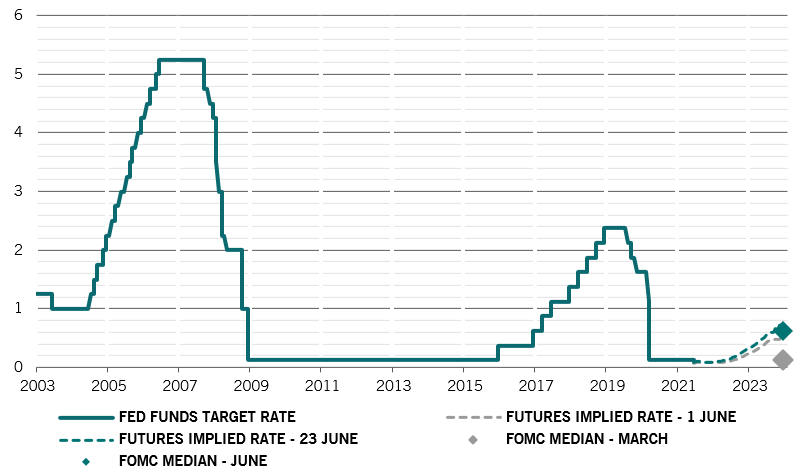

The Fed now appears set to hike interest rates as early as end-2022 after it unexpectedly upgraded this year’s growth and inflation projections in June.

Higher interest rates could come even sooner if wage inflation picks up from the current 3 per cent year-on-year pace – which will in turn pressure corporate profit margins.

In Europe, economic conditions are improving rapidly as the bloc’s vaccination programme and business re-openings gather pace.

Further improving the region’s prospects, euro zone countries will soon begin receiving funds from the EUR750 billion recovery fund, which is expected to boost growth by at least 0.2 percentage points both this year and next.

Economic momentum in emerging countries is levelling off as Chinese growth cools after a strong rebound. We think domestic demand will replace exports as the main contributor to economic growth, which will in turn boost retail sales and fixed asset investments.

Our liquidity indicators support our neutral stance on risky asset classes.

Liquidity conditions in the US and euro zone are the loosest in the world, thanks to continued monetary stimulus from central banks.

In contrast, China’s liquidity conditions are now tighter than before the pandemic as Beijing resumes its crack down on debt after a 2020 boom in lending among small and medium enterprises.

However, a further slowdown in the world’s second largest economy may prompt the People’s Bank of China to switch to easier monetary policy later this year. This will see the central bank intervene in the foreign exchange market to weaken the renminbi currency.

Our valuation models suggest equity valuations are at their most expensive levels since 2008. Tighter liquidity conditions and a further increase in real yields are likely to pressure global price-earnings multiples, which we expect to decline by up to 20 per cent in the next 12 months.

Our model suggests that corporate profits should grow globally around 35 per cent year-on-year this year. We think consensus earnings growth forecasts for the next two years -- at around 10 per cent -- are too optimistic as that would take EPS clearly above the pre-Covid trend, which is unlikely given that profit margins are already stretched.

Our technical indicators remain moderately positive for equities. Within fixed income, Chinese government debt – in which we are overweight – is the only asset class for which technical signals are positive.