Navigating populism

Investors need to prepare for increasingly populist and market unfriendly politics.

Written by

Shaniel Ramjee

Co-Head Multi Asset London

Investors’ halcyon decade is drawing to a close. The coming years are likely to be more challenging.

To see why, it’s important to consider how we got to where we are now. Aggressive central bank intervention staved off a global depression following the Lehman Brothers collapse in 2008. But it also came with nasty side effects. The plentiful liquidity which ignited a boom in company earnings and asset markets also led to a severe widening of the divide between society’s very wealthy and the rest.

This, in turn, has fed populist fires. The public perception that quantitative easing has largely been for the benefit of the 1 per cent – notwithstanding that it helped to support fragile economies and boost employment – underpins current calls for governments to look for other solutions when the next downturn strikes.

Most investors seem to take it for granted that central bank independence is guaranteed forever. They shouldn't.

One of these alternatives is central bank-funded fiscal spending, an approach that’s at the heart of Modern Monetary Theory (MMT). MMT essentially says that a government that issues its own currency can always maintain full employment by having the central bank finance sufficient levels of public spending. It’s a modern reworking of 1930s New Deal policies with the additional twist of not being worried about where the money’s coming from.

MMT’s theoretical merits are still being hotly debated in policy making and academic circles. But it’s captured the popular imagination and the support of politicians of various stripes.

The upshot of these sorts of policies is an end to an extremely market-friendly era and a return to some of the challenges investors faced during the 1970s.

The end of independence

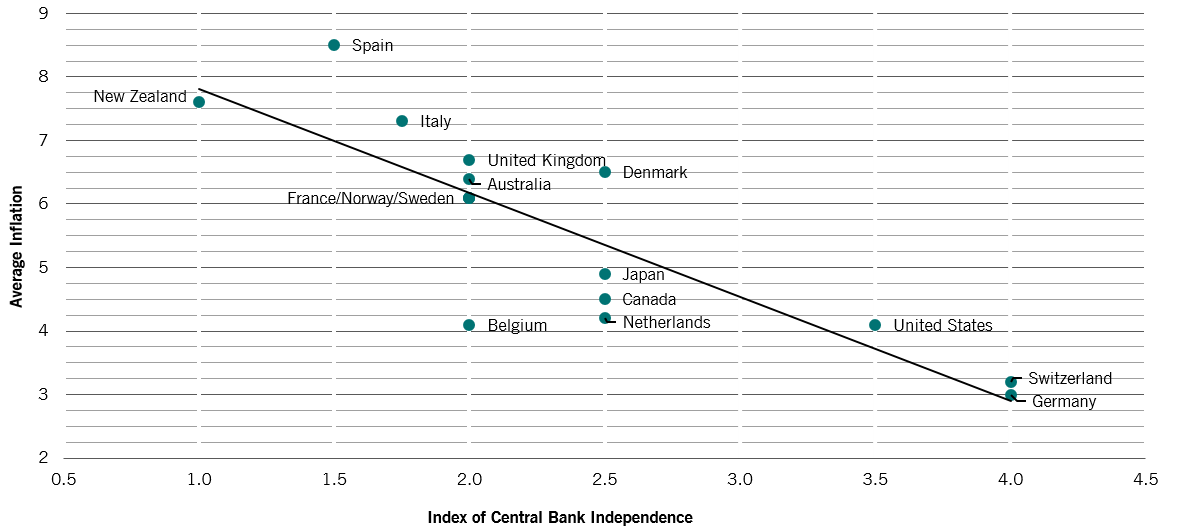

Undoubtedly, central bankers would put up a fight. Monetary financing of fiscal deficits is anathema to orthodox economics – notwithstanding the increasing politicisation of monetary policymaking during the past decade. That's because central bank independence is strongly associated with low inflation (see chart).

Indeed, central bank independence has become such an article of faith in finance it’s easy to forget how relatively new it is – the Bank of England, for instance, only gained operational control over monetary policy in 1997.

Yet most investors seem to take it for granted that independence is guaranteed forever. They shouldn’t. We think there’s a significant risk that central banking’s future could well look a lot like its distant past: back to being government departments under politicians’ direct control.

free to fight inflation

Average inflation 1955-88, %, vs. index of central bank independence (higher score = more independent)

You can see the global drift in that direction already. Turkish President Recep Tayyip Erdogan has frequently weighed in on the Bank of Turkey’s policy and last year gained the power to appoint its governor directly. Philippine President Rodgrigo Duterte recently selected a political ally as head of his country’s central bank, unsettling investors1. Such shifts aren’t confined to the developing world, either. They’re even emerging in advanced economies.

In the US, President Donald Trump has taken frequent pot shots at the US Federal Reserve over what he sees as an overly tight monetary policy. Italy’s populist government, meanwhile, has been pushing the European Central Bank for debt forgiveness – in effect asking for its debt to be monetised.

To be sure, open-handed government spending, be it helicopter money or more targeted measures, would probably see a broader distribution of benefits than the quantitative easing of the past decade. It’d be a “people’s QE” of the sort advocated by the UK’s left wing Labour Party. But it would also bring a whole new set of side-effects.

Investors be warned

Monetisation of government debt is likely to be inflationary in a way that ordinary QE hasn’t been. QE relies on the wealth effect, by forcing people out of safe government bonds into riskier assets. This, in turn, boosts business sentiment and spending and ultimately gets the economy going by encouraging companies to hire more people. Fiscal spending (or transfers), in comparsion, is much more direct. Money goes straight to those who are more likely to spend it. That might work when there’s slack in the economy. But once that disappears, too much money ends up chasing too few goods, allowing inflation to take root and potentially spiral out of control.

At the same time, deficit countries engaged in this sort of policy threaten to scare off foreign creditors, causing their currencies to depreciate, government bond yields to be squeezed higher and inflation to pick up.

Countries with big balance of payments and government deficits are likely to suffer most. And those with substantial wealth and income inequality might be expected to provoke bigger populist backlashes.

Rising inflation and wages, then, threaten to eat into corporate margins and profitability. Both could drop sharply given that they’re already historically high.

Normally, companies with monopolistic or oligopolistic pricing power would be better placed to defend their profitability. But populist governments are likely to be business-unfriendly in a number of ways. They’d be more inclined to regulate against rent-seeking companies. They’d probably look to offset deficits with more corporate taxation and potentially with higher capital gains taxes. Some industries are likely to be particularly hard hit, such as financials. By contrast infrastructure is likely to benefit. As are sectors that tend to be publicly funded – healthcare and education in particular.

Investors will need to, at the very least, keep up with inflation. Real assets, like real estate or gold are usually favoured although the former can be taxed, while the latter doesn’t generate any yield.

Commodities may benefit too, although Green Economy sectors are more likely long-term winners. At the same time, regulatory pressure to boost competition in technology and communications should lead to the emergence of a host of new high-growth companies.

With the political weather likely to be very changeable, investors need to be nimble and exceptionally well-informed. In other words, it’ll be an environment that requires more nuanced investments and the willingness to adopt a tactical approach.

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer. This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.