Family businesses: Insights on an attractive investment prospect

September 2020

Marketing Material

Pictet-Family – Fund manager interview

Pictet Asset Management has developed a new investment strategy that invests in listed family businesses, companies that count founding families as major shareholders.

Written by

Cyril Benier

Senior Investment Manager

Share this article

The portfolio is a repositioning of the Pictet-Small Cap Europe fund and is managed by Cyril Benier and Alain Caffort.

In this Q&A, they discuss the strategy’s guiding philosophy.

What exactly is a family business?

How you define a family business is a matter of interpretation. Sometimes it’s obvious, say when founders hold very large stakes in their own names. But the boundaries can sometimes be blurred. We take a systematic and rigorous approach to our definition. Family businesses that make up our investment universe are public companies in which an individual or family holds a minimum of 30 per cent of voting rights. The family can be by blood or marriage, the stake can be held through a foundation or some other vehicle. Such information is rarely freely available; unearthing it often requires painstaking research.

Why 30 per cent?

Research shows that active participation in the general assemblies of publicly listed companies averages around 60 per cent of share ownership. At 30 per cent, a shareholder (or group of closely tied shareholders) effectively has the casting vote and, thus, control.

Why focus on family businesses?

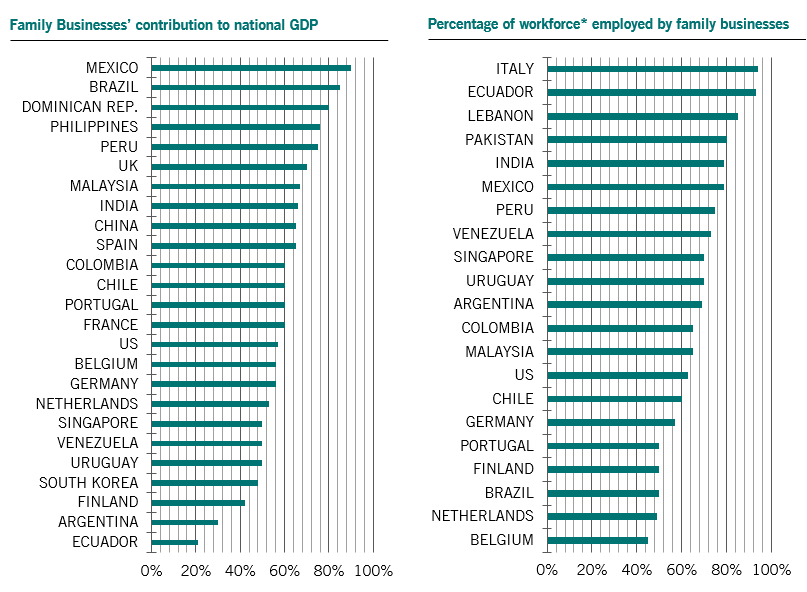

Family businesses are the lifeblood of our society and the backbone of the global economy. They contribute between 50 per cent and 70 per cent of countries’ gross domestic product and employ the majority of their workforces.

Society's true backbone, both economically and socially

Source: Tharawat Magazine, Economic Impact of Family Businesses – A Compilation of Facts, 06/01/2016 – over 40 sources used including IMD and KPMG

*Data representative of private employers only

There’s a large body of research showing family businesses tend to outperform their peers – financially and in terms of shareholder returns.

Of course, as anyone with experience of families and family disputes knows, this type of ownership can also lead to a number of problems – which is why it is also crucial to take an active approach to investing in these companies. And that’s where we can make a difference – ensuring we avoid the pitfalls in this otherwise attractive investment landscape. Please read our related article on the universe for more about why it makes sense to invest in family businesses with an active approach.

This suggests corporate governance is a big focus for you, is that right?

Environmental, social and governance (ESG) factors are all important sources of investment performance. But when it comes to investing in family businesses, governance is key. That’s because governance is intrinsic to a company’s overall values and culture.

We use several bespoke indicators in order to draw out what’s acceptable and what isn’t. For example, we tolerate a lower degree of board independence from family companies – after all, the close alignment between the family’s and business’ fortunes is one of the reasons these companies do so well – but we’re much more stringent on the composition and approach of the company’s audit, remuneration and nomination committees.

What sorts of family businesses do you invest in?

We look for high quality businesses with strong revenue growth and balance sheets that are well managed and leaders in their sectors.

We have no geographic or size preference – with the caveat that the shares have to have a fairly substantial minimum daily liquidity of USD5 million. We accept that this liquidity requirement keeps us from investing in some potentially interesting companies, but it also protects our clients from the worst effects of market dislocations such as we’ve recently seen.

Importantly, even after applying this stringent criteria, there are enough investable companies left – our universe is made up of 500 companies globally that operate across all sectors. It’s also worth noting that our liquidity limitation means that our strategy’s performance isn’t down to size effects. It’s not a case of trading performance for liquidity and thus volatility, as is the case with many small-cap funds. So we know that the outperformance of family businesses really is down to family effects.

Are family firms weighted to certain countries and sectors?

Not in a way that narrows our investment options. Family companies operate across all sectors and industries. And we have a more balanced regional distribution than capitalisation-weighted global equity indices – for instance, 59 per cent of the MSCI All Country Index is based in North America, while our weighting is around 44 per cent.

But it is true we prefer some sectors to others. For example, Consumer Discretionary companies make up around 11 per cent of the MSCI ACWI but have nearly twice the weighting in our portfolio. And the majority of these companies are based in Europe, including some of the great luxury goods companies.

We’re also relatively heavily weighted towards Communication Services and Consumer Staples. By contrast Energy makes up more than 5 per cent of the MSCI ACWI but less than 2 per cent of our holdings.

Why Pictet Asset Management?

Pictet-Family brings together the core capabilities of the Pictet group: Family businesses, Global funds, identification of winning market themes and a strong focus on ESG factors.

We know what the drivers of a successful family business are and what characteristics of a family business we are looking for. After all, we have a strong case study right at home: Pictet is a family business and a very successful one.

Webcast

>

Click the icon below to access our latest Pictet-Family webcast

Acknowledgements

Alain Caffort and Cyril Benier contributed to this article.

Cyril Benier joined Pictet Asset Management in 2016 as a Senior Investment Manager.

Before joining Pictet, Cyril had been working at AXA IM since June 2008 as a Portfolio Manager within the Small Cap Equities Team. He was in charge of the coverage of Industrial, Chemical, Mining and Energy sectors for European and Global small cap portfolios. He co-managed the European Small caps fund and managed the AXA Deutschland fund. Prior to that Cyril spent four years at Natixis Asset Management, as a mid- and small-cap equities Portfolio Manager. He was also responsible for the Natexis Eurovalue fund from 2005-2008 and for the European Smallcaps fund from 2007. Cyril began his career at Crédit Lyonnais Asset Management as a small-cap Analyst in 2002.

Cyril is a graduate of the SFAF, has a specialised Master’s degree from HEC, a leading French business school, and an engineering degree from the UTT-Groupe UTC.

Share this article

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user experience and to collect statistical data. You may refuse to accept cookies or change your settings by clicking the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.