[1] Carbon Pricing Dashboard, World Bank

[2] Article 6 of the Paris Agreement provides options for voluntary cooperation amongst countries in achieving their NDC (nationally-defined contributions) targets to allow for higher climate ambition, promote sustainable development, and safeguard environmental integrity

[3] Ricke, K., Drouet, L., Caldeira, K. et al. Country-level social cost of carbon. Nature Clim Change 8, 895–900 (2018). https://doi.org/10.1038/s41558-018-0282-y

[4] China Carbon Pricing Survey 2020

The world needs a much higher carbon price

Carbon pricing has so far failed to take off. But it could soon become a pillar of the green economy.

Written by

The Thematic Advisory Board

The transition from a fossil-fuelled economy to one powered by renewables carries the promise of being as transformational as the agricultural and industrial revolutions.

But as things stand, hopes for containing climate change look ambitious.

New net zero pledges from the US, China and Europe are inadequate. They still leave the world far short of the Paris Agreement goal of limiting global temperature rises to below 2 degrees Celsius from pre-industrial levels.

This is why carbon pricing is essential.

According to members of the Pictet Clean Energy Advisory Board, a fully functioning carbon pricing mechanism could be the difference between halting climate change and allowing it to spiral out of control.

Market forces, they argue, can be a powerful ally, helping change the behaviour of businesses and consumers.

The problem is finding a way to harness them effectively.

Currently averaging globally at just USD2 per tonne of CO2, the carbon market is clearly not doing the job it was set up to do. The International Energy Agency says carbon prices need to rise to as much as USD140 by 2040 to meet Paris goals.

Breaking the tragedy

Getting there will not be straightforward.

As former Bank of England Governor Mark Carney warned, the battle against climate change is hampered by the “tragedy of horizon”. In other words, the current generation has no direct incentive to fix the problem when catastrophic impacts of climate change will not be felt for decades.

By making carbon emissions more costly today, however, there is the possibility of avoiding that tragedy.

The World Bank’s modelling has shown that carbon pricing has the potential to halve the cost of implementing Paris targets, saving some USD250 billion by 2030.

One problem is that carbon pricing schemes don’t cover nearly enough of the world’s emissions.

Globally, the carbon pricing market accounts for about 12 gigatonnes of CO2 equivalent – which translates into just under a quarter of all annual global greenhouse gas emissions.1

The US, the world’s biggest polluter, does not even participate in carbon trading at the federal level while the Paris climate agreement did not include a provision for pricing carbon.2 Industry lobby groups in coal, oil and gas sectors had been fierce opponents too.

And then there is a wide divergence in prices from country to country.

European countries set the example.

Sweden levies the highest carbon tax in the world at SEK1,190 (EUR117)/tonne CO2, covering about 40 per cent of its greenhouse gas emissions.

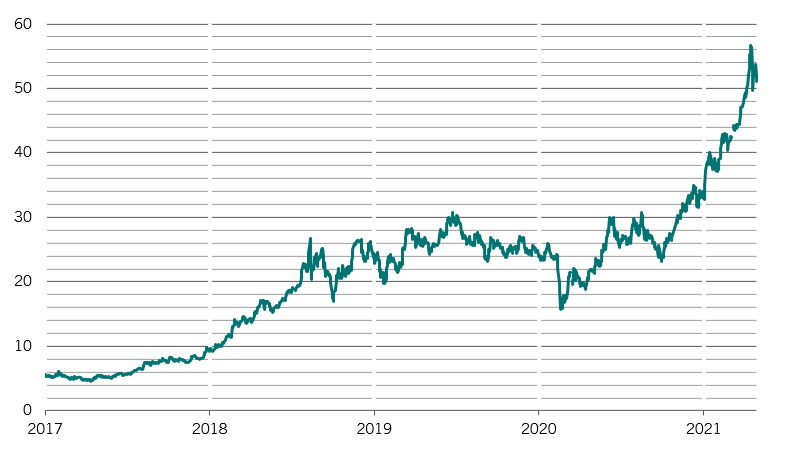

In Europe, the world’s biggest and oldest market, carbon prices rose more than five-fold since 2018 to a record high in May (see Fig. 1).

Fig. 1 - Pay-as-you-pollute

European Union Carbon Emissions Allowances (EUA) December 2021 futures

But elsewhere, carbon remains under-priced.

According to the IEA, the average carbon prices would need to rise almost 50-fold to USD75-100/tonne by 2030 and then USD125-140 by 2040 to meet Paris Agreement goals.

University of California San Diego researchers believe even that will fall short.

Their study puts the social cost of carbon – which takes into account empirical climate-driven economic damage estimations and socio-economic projections – at a staggering USD417/tonne.3

The lack of a harmonised market and a unified global carbon price are perhaps the most significant problems.

Businesses, especially in energy-intensive industries, may relocate out of countries with high carbon costs into those with laxer emission constraints – in a phenomenon known as “carbon leakage”.

Our advisory board members say renewed international efforts to fight global warming could encourage more countries and regions to start adopting carbon pricing schemes. That should push prices higher in the long term and prevent carbon leakage.

The signs are encouraging. In China, which launched its national carbon market in February, market participants expect the price to average RMB66/tonne (USD10) in 2025 before rising to RMB77 by the end of the decade.4 It has the potential to be the world’s biggest carbon market.

Elsewhere, the American Petroleum Institute, the powerful fossil fuel lobby, is now endorsing the introduction of carbon prices in a major policy reversal that underscored seriousness in tackling climate change.

What’s more, Brussels plans to present proposals to revise and possibly expand its emission trading system in line with the European Green Deal and its new target to reduce greenhouse gas emissions by at least 55 per cent by 2030.

One way to improve the emission pricing system is to expand the use of carbon credits. Governments can give out credits to businesses that lower their carbon footprint with carbon capture and storage (CCS) technology, reforestation activities or energy efficiency solutions.

This way, companies can gain flexibility in complying with carbon pricing regulations.

The discussion on carbon pricing and credits is likely to feature prominently during the landmark UN climate talks in Glasgow later this year as potential cornerstone to supporting climate goals.

Accelerating innovation

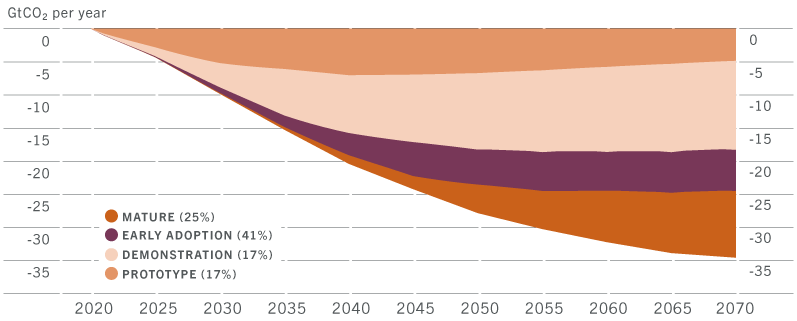

An overlooked benefit of effective carbon pricing is that it can also accelerate the pace of innovation in clean energy technologies and promote a faster and broader adoption of products and services that have yet to become commercially viable.

For example, our Advisory Board members say, certain types of hydrogen power generation that combines carbon storage could become cost competitive if carbon prices are set around EUR60-70 per tonne of CO2.

Other technologies that could become viable at higher carbon prices include advanced power transmission mechanisms and next-generation batteries.

This would have significant benefits. The IEA estimates such technologies alone have the potential to cut global energy sector CO2 emissions by nearly 35 gigatonnes of CO2 by 2070, or 100 per cent of what’s considered sustainable in the same period.

Fig. 2 - Innovate to reduce

Global energy sector CO2 emissions reductions by current technology readiness category

The transition to a decarbonised economy will be among the most wrenching socio-economic shifts humans have ever experienced. Yet even though the survival of the planet is at stake, resistance to change is proving difficult to overcome. A higher carbon price can smooth the path.

more on clean energy

Listed infrastructure's crucial role in the clean energy transition

Why clean energy stocks should be considered as part of an allocation to infrastructure.

April 2021

Aiming for zero: Europe raises its clean energy game

Why Europe's ambitious new climate plan will help the region become carbon neutral and spur investments into the clean energy industry.

April 2021

A climate-aware US ushers in a new era for clean energy

Biden's bold environmental plan will reinvigorate the global fight against climate change and turbo-charge the clean energy industry.

January 2021

Hydrogen: beyond hot air

As production scales up and costs fall, a hydrogen-fuelled future is within sight.

January 2021

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Investor Information Document (KIID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 15 avenue J.F. Kennedy, L-1855 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any. The KIID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. Pictet Asset Management (Europe) S.A. has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.