[1] Accenture COVID-19 Consumer Research, conducted March 19–25 and April 2–6, 2020

[2] Includes organic, Fairtrade, Rainforest Alliance and Marine Stewardship Council (MSC) certified product. https://www.mintel.com/press-centre/food-and-drink/eating-with-a-conscience-ethical-food-and-drink-sales-hit-8-2-billion-in-2018

[3] COVID-19 Disruptions in the US Meat Supply Chain, Federal Reserve Bank of Kansas City

[4] Popkin, BM, Du, S, Green, WD, et al. Individuals with obesity and COVID‐19: A global perspective on the epidemiology and biological relationships. Obesity Reviews. 2020; 21:e13128. https://doi.org/10.1111/obr.13128

[5] UN Food and Agriculture Organization

[6] European Commission

Better for you, better for the planet - food after Covid

Covid-19 has disrupted the food sector's supply chains and is set to change consumer eating habits for good.

Written by

Mayssa Al Midani

Senior Investment Manager

The Thematic Advisory Board

Spending an entire day in the fresh air and sunshine, having the freedom to roam in outdoor space of some 108 square feet, and being able to feast on delicious wildflowers in open pastures untouched by pesticides or herbicides.

This is the leisurely daily routine that the “girls” – or hens – at Texas-based food company Vital Farms enjoy in return for producing their highly prized eggs.

It's a scene you'd expect to come across in a small organic farm, the sort run by a family committed to ethical production. Vital Farms certainly started out that way. But it is now going big.

So big in fact that, earlier this year, the ethical food company secured a valuation of USD1.3 billion in one of the sector's most-anticipated initial public offerings.

The food industry will soon be full of companies like Vital.

That's because the firm's success owes much to some powerful trends unleashed by Covid-19. Two stand out. First, food producers are having to re-configure their supply chains after the pandemic disrupted global trade. It's an environment where complex international sourcing and distribution networks are under pressure and under scrutiny.

Second, the industry now has to cater to the needs of a more demanding customer base - one that cares less about convenience and more about the nutritional and ethical aspects of what it buys and eats.

In a few years, the food industry could look very different, according to members of the Nutrition Strategy Advisory Board. It might consist almost entirely of companies that possess only the strongest social and environmental credentials.

Covid: shaken and stirred

The pandemic has unleashed turmoil across a wide range of industries. Food suffered more than most. Lockdowns and border closures disrupted the distribution of agricultural products and also led to severe labour shortages at food processing facilities.

At the same time, Covid-19 triggered a change in consumer behaviour.

A survey by consultancy Accenture conducted during the pandemic found that consumers increasingly prioritised health and sustainability when deciding what to buy.1

In the UK alone, sales of ethical food and drink are forecast to rise by 17 per cent to GBP9.6 billion by 2023, having already grown more than 40 per cent in the five years to 2018.2

In response, the food industry is investing heavily in a wide range of high-tech solutions. Many of which are geared to strengthening supply chains, raising production standards and reducing food waste..

It is perhaps in the meat industry where the pandemic-induced transformation is particularly acute.

Slaughterhouses and meat-processing plants found themselves in the frontline of the Covid battle after cluster of virus cases emerged in facilities worldwide. In the US for example, more than 80 beef and pork packing plants in the US reported virus outbreaks between April and June 2020. By mid-May, meat production fell 40 per cent below 2019 levels.3

But keeping facilities safe and virus free isn't the industry's only problem. The pandemic also brought into relief the health and environmental costs associated with meat consumption and production.

Studies have shown a strong link between obesity and Covid.4 At the same time, consumers have been reminded of meat's outsized environmental footprint. Livestock farming is responsible for 15 per cent of greenhouse gas emissions and accounts for some 29 per cent of the world’s freshwater use.5

It is for these reasons that our Advisory Board members expect meat consumption to fall and healthier alternative meats and plant-based diets to become more popular.

Alternative culture

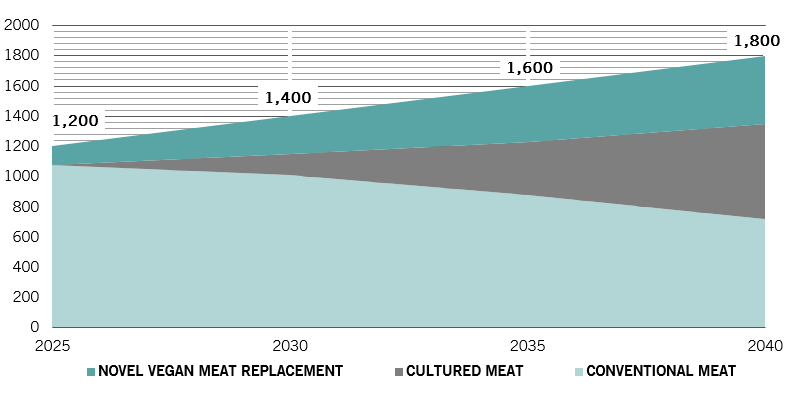

Global meat market sales forecast 2025-2040 (USD bn)

Alternative meat producers such as Beyond Meat and Impossible Food have already raised hundreds of millions of dollars in funding in recent years. Their expansion has also seen them seal agreements with major supermarkets and fast food chains to sell their high-margin products. To our Advisory Board members, this represents only one aspect of the meat revolution.

Internet of Food Things

Another is increased automation. Compared to other parts of the food industry, meat production is very labour intensive. This became a vulnerability during the virus outbreak as plants struggled to remain operational with severely depleted workforces. Many producers now see technology as means to improve their resilience.

The same is true for industries beyond meat. Greater use of automated systems would not only ensure food security and quality, however. It brings the added benefit of more efficient resource use.

According to our Advisory Board, the production lines of the future will be built on sensor networks, the Internet of Things and blockchain technology. Other points in the supply chain are also set to make greater use of technology, particularly logistics and distribution.

Greater use of automated systems would not only ensure food security and quality...it brings the added benefit of more efficient resource use.

The public health crisis has also trained a spotlight on food hygiene standards. Unsettled by the rapid spread of the virus, consumers have understandably become concerned at the possibility of food being a transmitter of disease. Technology can help assuage such fears, our Advisory Board members say.

The food industry is home to a growing number of specialist companies developing advanced food testing and diagnostics services.Our advisors expect food producers to invest more heavily in sustainable grocery packaging that has antibacterial properties, and make greater use plastic alternatives or other innovative technologies such as QR codes.

Interestingly, these products not only improve food safety and reduce the risk of contamination, they are also good for the environment as they can help reduce waste. Waste is one of the food industry's biggest problems. Europe alone wastes an eye-watering 20 per cent of all produced food, worth some EUR143 billion a year.6

Taste of the future

Faced with a growing world population and climate change, the food industry was already under severe strain even before Covid-19 struck.

Looking ahead however, the pandemic could help revitalise it. If food producers and distributors move quickly to deploy advanced technology and innovation to meet growing consumer appetite for food that is healthier and more sustainable, the industry will be fit to meet the demands of the 21st century.

The Nutrition strategy: investing in the future of food

- Our Nutrition strategy directs capital to companies which improve sustainability, access, and quality of food necessary for health and growth. The strategy invests across the entire food chain, from farm to fork.

- Long-term growth potential: both governments and consumers are demanding higher quality food and improved diets. Therefore, companies enabling better nutrition should benefit from growth.

- Responsible and sustainable approach: companies that provide solutions to increase output with minimal resource use and waste (i.e. lower environmental impact) will be crucial in the shift toward a more sustainable food system.

- A diverse and resilient opportunity set: across several sectors and geographies with different characteristics; supported by strong long-term secular growth tailwinds, the strategy aims to outperform the broader market over economic cycles.

- The strategy is suitable for investors who are prepared to invest for the long term and are willing to take a potentially higher risk with their investment.

- Each stock must have a high thematic “purity” for it to qualify as a potential investment. Thematic purity is a proprietary indicator of how specialised a company’s activities are. In Nutrition strategy, we exclude activities such as the manufacture of beef, palm oil, alcoholic and carbonated soft drinks as well as unhealthy snacks from this purity calculation.

Read more on thematic investing

Thematic equities: their use in a diversified portfolio

Investors can make an allocation to thematic equities whichever portfolio construction approach they use.

December 2019

Five ways that investing could help create a better planet

By investing in companies finding solutions to the environmental crisis, investors can help build a better world for future generations.

Why take-out food could become a healthy obsession

As our eating habits change companies are developing new ways to produce convenience food that is healthier and better for the environment. That's also good news for investors.

July 2019

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Investor Information Document (KIID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 15 avenue J.F. Kennedy, L-1855 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any. The KIID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. Pictet Asset Management (Europe) S.A. has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.