Select your investor profile:

This content is only for the selected type of investor.

Individual investors?

Dividend yields cast UK stocks in favourable light

Relative to government bonds UK equity dividend yields are more generous than they've been for 60 years. That's something investors can't ignore Brexit or no Brexit.

Written by

Supriya Menon

Senior Multi Asset Strategist

The UK equity market can’t seem to catch a break. Any good news is almost immediately swamped by the latest glum Brexit headlines.

Some market commentators have gone so far as to argue that toxic politics makes British equities “uninvestable”. No wonder savers have pulled USD1.01 trillion from UK equity funds since June 2016 when the British voted to leave the European Union1.

The latest gloom centres on whether Prime Minister Theresa May will manage to convince enough of her party to buy into the deal she’s struck with Britain’s EU partners to win a House of Commons vote. Or whether the country will face the prospect of a disorderly divorce on Brexit day at the end of next March.

In our view, investors with robust risk appetites might consider the market a buy whatever the outcome.

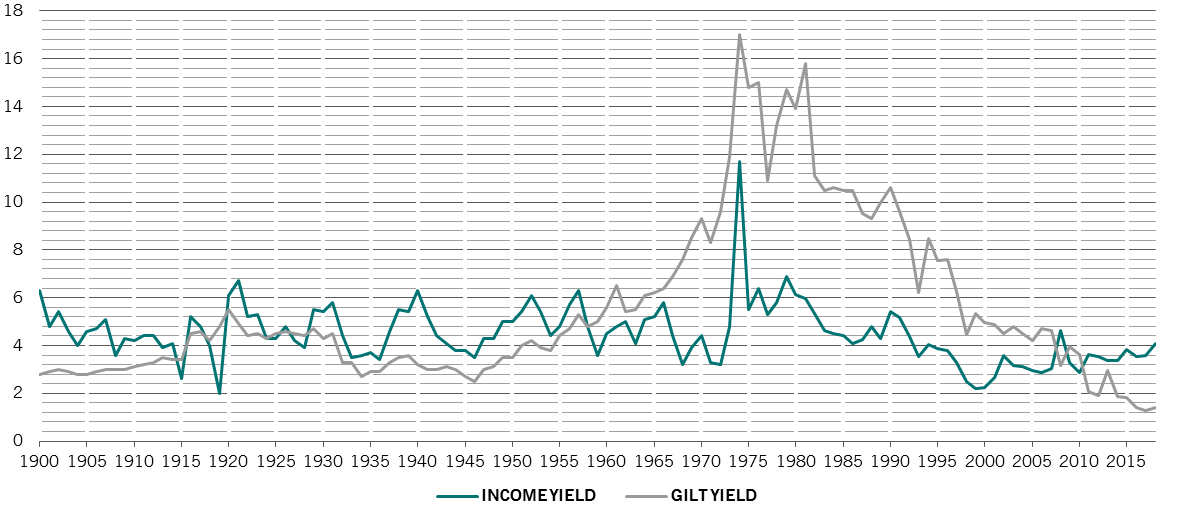

All Change

UK long-dated government bond yield and UK dividend yield, %

That contrarian take is supported by the handsome dividend yield British equities now offer, not just relative to government bonds and other developed stock markets, but relative to the market's own history.

Apart from a short period during the great financial crisis, the 4.1 per cent dividend yield currently offered by UK stocks is the highest it’s been since the mid-1990s2.

That also happens to be bang on its average since 1900, which includes the 1970s when dividend yields rocketed into the double digits with inflation.

Historic returns

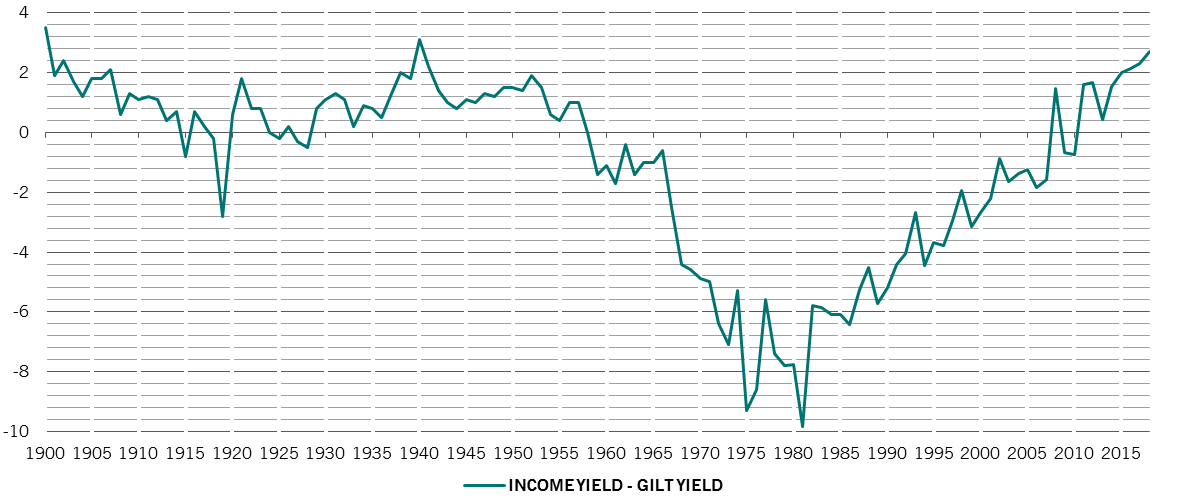

Meanwhile, relative to yields on 10-year British government bonds, the dividend yield is close to as high as it has ever been. Indeed, that positive differential of 2.7 per cent is nearly 4 percentage points above its 118-year average.

So what’s going on? To begin with, the big premium on equity over bond yields is bound to have more than a little to do with financial repression. Quantitative easing and regulatory demands that pension funds more closely match their liabilities with secure income flows have forced up the price of “safe” government bonds – which is to say, driven down their yields. And with the 10-year gilt yielding 1.3 per cent when markets are also anticipating a 3 per cent inflation rate, this merely means investors in UK government bonds will grow steadily poorer.

on the up

UK dividend yield minus long-dated government bond yield, percentage

But in the UK, this isn’t just a fixed income story. British companies have always tended to have high dividend payout ratios. The latest data show that British firms are paying 60 per cent of earnings to investors as dividends, against 38 per cent and 42 per cent for German and American companies respectively.

That could be because, historically, the UK has had more favourable tax treatment of dividends, or because of large institutional demand for income versus capital appreciation, or because the composition of the UK market is tilted towards mature, defensive companies.

At the same time, Brexit has forced up the implied equity risk premium on the UK equity market to close to 10-year highs, in essence projecting a corporate earnings growth rate of just 0.8 per cent on average over the long term. That's well below the 6.1 per cent average annual growth firms actually managed over the past quarter century. In other words, the UK equity market looks exceptionally cheap to anyone expecting the equity risk premium to drop back towards more normal levels.

In a world where investors are routinely starved of income, a 4.1 per cent yield starts to look fetching – especially considering that companies tend to be loath to cut dividends and payouts rarely fall across whole markets. Investors – like us – agnostic as to the source of return, whether it comes from income or capital appreciation, should find the UK’s dividend yield in an environment of weak economic growth attractive even if Brexit turns out to be of a harder variety than the one the government is aiming for.

related articles

Barometer: The investment landscape in 2019

Investors should expect conditions to get tougher in 2019 as central banks are likely to continue tightening the monetary reins leaving markets exposed to the risk of further political upheaval.

November 2018

Barometer: Battening down the hatches

With the outlook for the global economy darkening a shade and liquidity conditions less than buoyant riskier asset classes face an uphill struggle.

December 2018

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Investor Information Document (KIID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 15 avenue J.F. Kennedy, L-1855 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any. The KIID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. Pictet Asset Management (Europe) S.A. has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.