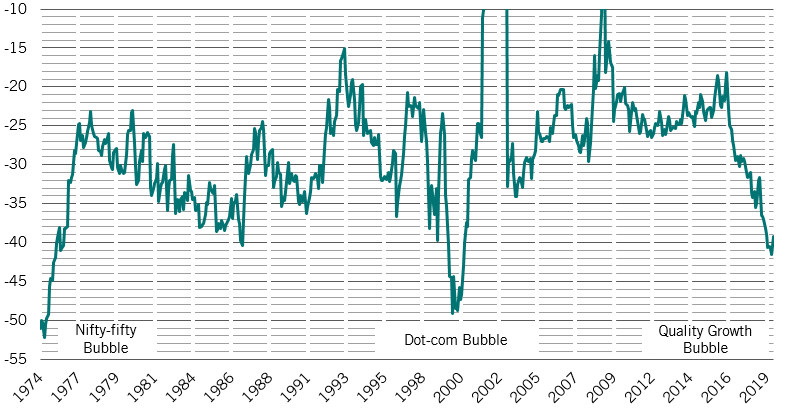

Asset allocation: glimmers of light

The US Federal Reserve and the European Central Bank are again pushing on the liquidity pedal. The US and China have relented on launching salvos at each other over trade. And our leading economic indicator is showing positive glimmers.

Yes, there are still question marks over China. And Germany continues to struggle. But on balance there’s a sense that sunnier skies are opening behind the recent global gloom. Hence our decision to raise our equity allocation to neutral from underweight – accompanied by a reduction in our cash allocation.

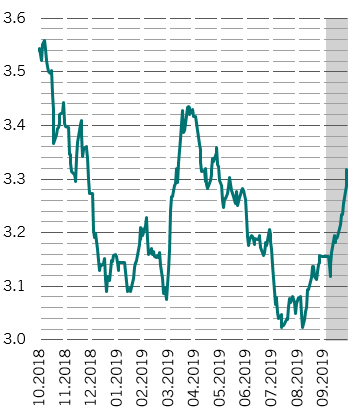

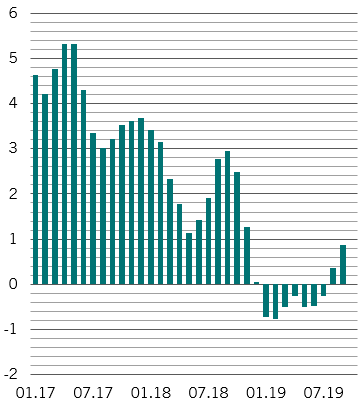

Our business cycle readings show that although global growth prospects remain below potential, our leading indicator points to some improvement in economic conditions in the months ahead. Much of that is thanks to some increasingly positive data from the US manufacturing and industrial sector and to the American consumer’s surprising resilience. If this month’s China-US trade talks result in a compromise – however narrow in scope – that’s likely to lift business sentiment.

A relaxation of trade conditions would be welcome for China in particular. Although its forward indicators have shown some improvement, the economy is still burdened by a decline in private investment, sluggish consumer spending and the devastation African swine fever has wrought on the country’s pork industry. Germany – which is likely to be in recession – will also be looking for good news on trade given its dependence on manufacturing and exports.

World leading economic indicator, 3m/3m annualised

Global liquidity conditions are neutral for riskier asset classes. The Fed seems bent on completely reversing its quantitative tightening with its interventions in the repo market. True, it’s not officially quantitative easing. But the effect is the same. At the same time, the central bank has delivered three rate cuts.

Meanwhile, on this side of the Atlantic, the ECB has engaged in its own easing programme – a parting gift from outgoing president Mario Draghi. That’s on top of strength we see in euro zone private lending. And several emerging economies have also started cutting rates.

So far, China hasn’t followed suit. Official policy continues to squeeze the shadow banking sector, while rising inflation – a result of the porcine catastrophe – limits the central bank’s room for manoeuvre. A trade deal, however, might give it a bit more flexibility.

Our valuation indicators haven’t changed materially over the past month despite the rally in risk assets and bond market sell-off. Equities are broadly fairly priced, though within the asset class, the US remains very expensive and the UK very cheap. And government bonds are expensive, while corporate bonds are extremely expensive.

Technical indicators are also broadly the same on last month – modestly positive for both bonds and equities and seasonality broadly neutral for both markets. Trends signals are turning negative, however, for Swiss and Japanese government bonds.