Emerging Asia's stocks and bonds have experienced a lost decade. Over the past 10 years, their returns have lagged those of global indices by a considerable margin. And that is despite the fact that these economies accounted for about 70 per cent of world GDP growth over the period. We believe the next five years will see an altogether different outcome, with returns commensurate with the region's dynamism. This means Asian assets are currently under-represented in global portfolios.

That is the conclusion of our analysis of emerging Asia1, a region characterised by improving growth prospects, low inflation, a credible commitment to reform and an increasingly diversified economy.

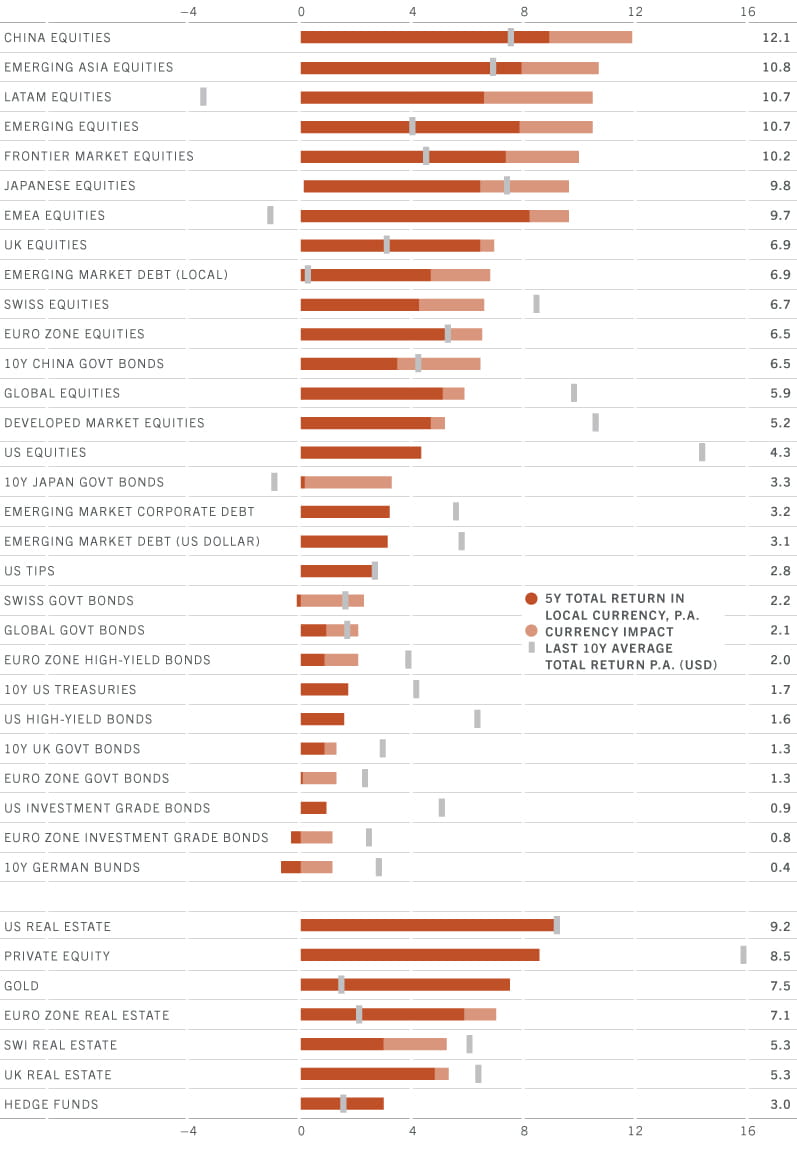

We expect emerging Asian equities to be the best performing asset class over the next five years, with returns averaging around 11 per cent per annum in US dollar terms. Vietnam and India should do particularly well.

Within fixed income, meanwhile, China’s government bonds offer the best return/risk profile while investment grade corporate bonds also look attractive.

To make the most of this opportunity, allocations will need to be both directly in Asian companies (as opposed to indirect exposure via developed market companies with exposure to Asia) and active. An active approach is essential because the divergence in returns for Asian asset markets increases the scope for excess returns. In addition the the economy is changing rapidly in areas such as e-commerce, green technology and financial services, sectors where Asia could become a global leader.

Currencies offer an additional source of return. Our models show the region’s currencies are among the most undervalued versus the US dollar, and we see good reason for that to change. The region runs a current account surplus, its monetary policy is far less expansionary and, in the renminbi, it has a currency that will soon begin to challenge the greenback’s dominance of the financial landscape.

Of course, there are risks. Asia’s developing economies face significant challenges ranging from China’s debt pile to those that won’t be resolved for decades, not least deteriorating demographics, climate change and weak governance. But many of these challenges can be overcome with a combination of technological development, innovation and political and social reforms.

The 1997 currency crash, which spread from Thailand to its neighbours, was a watershed for Asia.

It proved to be a catalyst for numerous ground-breaking structural reforms, each designed to reduce the region’s vulnerabilities and improve its economic resilience.

Two decades on, Asia finds itself at another turning point. Formerly the epicentre of the virus outbreak, it has emerged from the Covid crisis as the engine of the global economic recovery.

Thanks to its relatively effective handling of the pandemic and prudent fiscal and monetary policies, we expect Asia to be the world’s fastest-expanding region this year with GDP growth of more than 9 per cent .

Its regeneration won’t end there. Applying lessons from the 1997 playbook, Asian governments are using the crisis as an opportunity to extend reforms, boosting the international competitiveness of their economies.

Diversity is part of Asia’s investment appeal.

Luca PaoliniChief Strategist

There’s a crucial difference, however, between what is happening now and what unfolded two decades ago. In the late 1990s, the rise of the Asian tiger economies resulted from a singular focus. Export-led growth was the priority. The region’s current and future success, by contrast, rests on the diversity of its constituent parts. Some economies privilege domestic demand while others are pursuing global leadership in some of the world’s most dynamic industries. Korea and Taiwan, for example, are technologically advanced, open economies that are deeply embedded in global supply chains. Other Asian economies, meanwhile, benefit from a deepening pool of wealthy consumers and a growing service economy. India, with its burgeoning middle class, falls into this category. The region also supports emerging manufacturing hubs such as Vietnam and countries with a tilt towards commodities such as Indonesia and Malaysia. Then there’s China. The region’s dominant force is building on its traditional strengths in manufacturing while also gaining a foothold in areas where it has hitherto lacked influence. It has displaced the US as Europe’s biggest trading partner and is pressing ahead with reforms that could help it become a financial and technological powerhouse in as little as a decade.

Yet if diversity is part of Asia’s investment appeal, so too is the region’s drive to build on its advantage. This, its leaders increasingly recognise, will require deeper economic integration, more investment in technology and better welfare and educational provision. We expect the next five years to deliver rapid progress on all three fronts, tilting the world’s centre of economic gravity decisively Eastward.

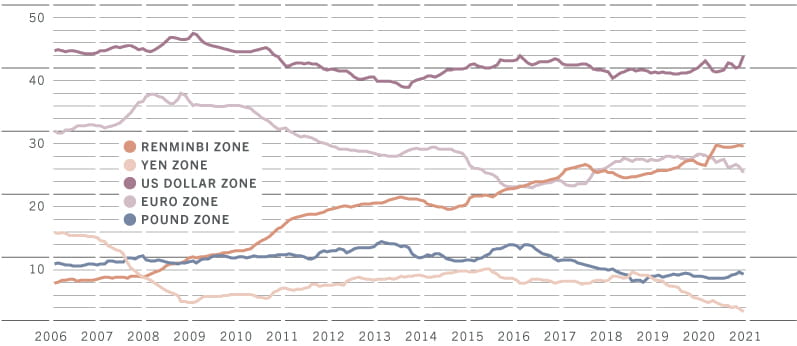

Since it joined the World Trade Organization in 2001, China has made a habit of disrupting the established order. It took the country less than 15 years to dethrone the US as the world’s largest economy on a purchasing power parity basis. Its research expenditure, meanwhile, has more than tripled in the last two decades, with the Chinese now spending almost as much on R&D as the Americans. Asia’s powerhouse has also quickly established itself as the global leader in artificial intelligence (AI). Last year, it accounted for a staggering 473 of the 607 AI patents filed with the World Intellectual Property Organisation2.

Yet within this impressively rapid metamorphosis sits an anomaly. For all its economic and technological heft, China’s currency, and by extension its stocks and bonds, remain minor players on the world stage. By one yardstick, the renminbi is a minnow by international standards, barely registering on the balance sheets of the world’s central banks.

Source: Pictet Asset Management, data covering period 31.12.2005-3-1.12.2020

Monetary zone is estimated as the elasticity-weighted share of 48 economies GDP where elasticity is the reserve currency weight in a given currency using a 2-step Frankel-Wei rolling regression

Emerging Asia’s investment hotspots

Asia is not only the world’s fastest growing continental economy: it is also, arguably its most dynamic. Its metamorphosis encompasses changes in its demographic make-up, economic models, consumption patterns and corporate structures. For investors, that gives rise to both opportunities and risks.

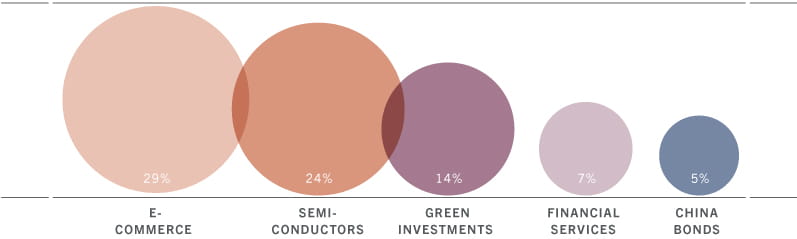

The region is fast becoming more digital, more urban, more innovative, and more focused on sustainability – structural shifts which investors can best harness through a thematic lens. We see particularly strong potential in five areas: e-commerce, financial products and services, the green transition, semiconductors and Chinese renminbi bonds. China and India should do well, while Vietnam flickers as a potential hidden gem.

The region’s distinguishing feature – and part of its investment appeal - is the diversity of its constituents, from the economic and cultural heft of India and China to the technological prowess of Taiwan and Korea.

Fig.3 - EM Asia’s share of global market*, selected sectors

*approximation of

EM Asia’s share of current investible opportunity, based on relevant sub-industries in MSCI World benchmark as of 31.05.05

China: Catching up with the US: benefits from a large and growing sphere of influence and an economy increasingly focused on innovation and R&D. Despite its size, China still offers strong economic growth, leadership in sectors such as e-commerce, a currency that is both attractively valued and stable and a defensive asset class in bonds.

India: Best long-term growth prospects in the region and a well-diversified economy. An investor favourite that, despite advantages such as a growing middle class and thriving tech sector, has underwhelmed in terms of performance in recent years: we believe reforms that address bottlenecks to growth, and a changing corporate landscape, including a strong pipeline of tech unicorns, can enable its this economy to achieve its potential.

Korea/Taiwan: World leaders in technology hardware and semiconductors, areas with formidable barriers to entry. Equities offer a cyclical boost to portfolios and protection in periods of a strong ride in the US dollar – typically when traditional emerging markets suffer.

ASEAN: Defensive growth profile. Smaller countries set to benefit from increased intra-regional trade. Within ASEAN, we see particularly interesting opportunities in Vietnam.

South and East Asia’s breakneck development over the past few decades has been a blessing for the billions who call it home. It has also brought with it challenges that governments have to tackle head on if this trend of superior growth is to be sustainable. The birth rate in the region is falling and its population ageing fast. Then there’s debt. A considerable amount of China’s growth has been driven by borrowing, recently among households. Longer term, meanwhile, countries across the region need to improve governance standards to make the leap to fully developed economies. Along the way, they’ll also have to tackle their share of climate change.

Asia’s ESG gap

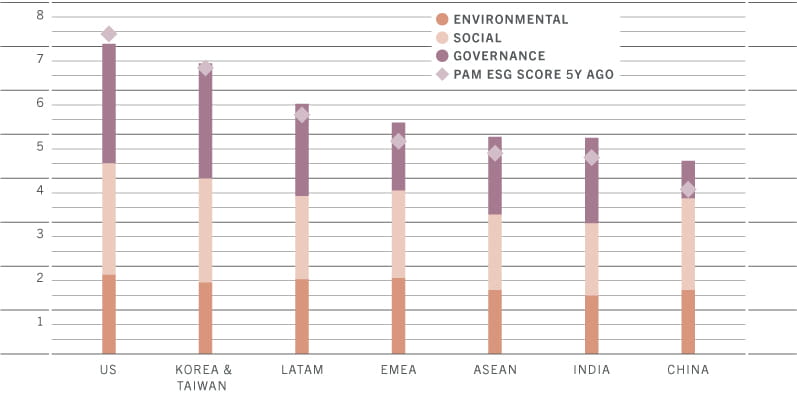

It is not a surprise that Asia, along with the majority of emerging countries, scores poorly on ESG metrics. Countries at an earlier stage of development typically put economic development at the top of their priorities and in doing so can easily overlook the impact of growth on the environment and social wellbeing. Their political and market institutions do not always ensure good governance – of which transparency is a key factor. We strongly believe that superior ESG scores will ultimately lead to superior performance and appeal to a new class of investors for which ESG is a pre-requisite for any investment decision.

Asia’s difficulties on the ESG front are clear and significant. But what really matters in our view, like most things in the world of investing, is the direction of travel. And on this, long-term investors might take some solace from the fact that although Asia lags on ESG scores, it is also improving the fastest among regions.

*PAM ESG score is based on a set of Environmental (7 including Air Quality, Climate Change, Water Quality and others), Social (7 including Education, Healthcare, Gender Equality and others) and Governance (9 including Civil Unrest, Corruption, Judicial system, Government Stability and others) indicators. ASEAN includes Indonesia, Malaysia, Thailand, Philippines and Vietnam. Regional score aggregated by GDP in PPP terms.

Source: Pictet Asset Management. Data as of Q2 2021

Superior growth, low inflation and cheap currencies. These are some of the defining characteristics of emerging Asian economies. They are also the reasons why investors should consider increasing their exposure to the region. Others include a reform agenda that is more ambitious than any in the world and a commitment to invest heavily in R&D.

We expect emerging Asian equities to deliver among the best returns in global stock markets over the next half decade, especially in dollar terms (10.8 per cent per year on average, or double the global market). We calculate that their outperformance – which stems mainly from superior earnings growth and currency appreciation – could amount to 35 per cent on a cumulative basis over the US in that timeframe.

Our analysis shows dollar-based investors are under-exposed to the region and should consider almost trebling the weight of Asian equities and bonds in their portfolios.

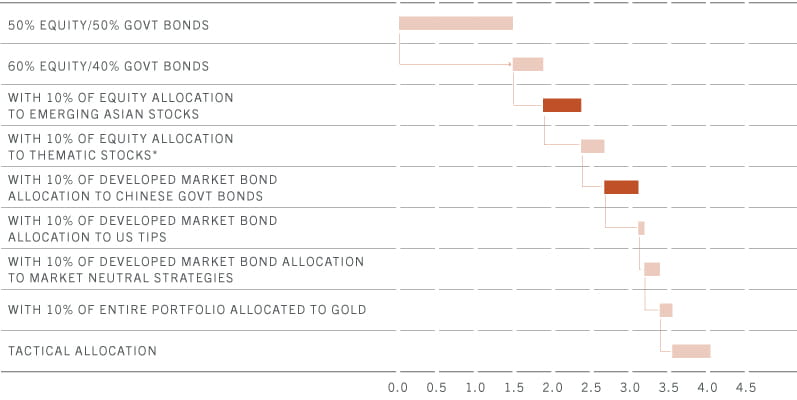

Fig. 5 - How to achieve a 4% annualised return over 5 years

Source: Pictet Asset Management; forecast period 31.05.2021-31.05.2026; Indices used in calculations: MSCI equity indices, JPMorgan government and emerging-market bond indices; *Thematic stocks are companies within our thematic universe that we believe offer a potential excess return of 3% per year over the MSCI World A/C Index. These companies operate in industries we expect to expand at a faster rate than the world economy (such as clean energy, robotics and digital technology). Please refer to the Appendix in the full document for the methodology.

Luca Paolini joined Pictet Asset Management in 2012 as Chief Strategist.

Before joining Pictet, Luca worked as an Equity Strategist at Credit Suisse Securities, responsible for asset, regional and sector allocation. From 2005 to 2007, he was Investment Strategist at Union Investment. Luca started his career in 2001 at Allianz Dresdner Asset Management as a assistant vice president, covering asset allocation and investment strategy.

Luca holds a Master degree in International Economics and Management from SDA Bocconi School of Management in Milan, and a Laurea Magistrale in Political Sciences from the University of Bologna.

Arun Sai

Senior Multiasset Strategist

Arun Sai joined Pictet Asset Management in 2020 as Senior Multi-Asset Strategist.

Before joining Pictet, Arun worked at Credit Suisse where he provided country and sector recommendations as a Global Emerging Markets strategist for the past 9 years. He began his career in 2005 as a Business Analyst at Cognizant Technology Solutions.

Arun holds a Bachelor of Engineering in Computer Science from University of Madras, India as well as an MBA (Finance) from Bharathidasan Institute of Management, India.

Pictet Asset Management’s Strategy Unit (PSU)

The PSU is composed of Pictet Asset Management’s most experienced multi asset and fixed income portfolio managers, economists, strategists and research analysts. This investment group is responsible for providing asset allocation guidance over the short-term and long-term horizons across stocks, bonds, commodities and alternatives.

Every year, the PSU produces the Secular Outlook: a publication providing asset class return forecasts for the next five years. The research embeds, and is a reflection of the PSU’s investment philosophy.

For more information about our multi asset expertise please contact your Pictet Asset Management representative or a member of the team via the contact details listed below:

Nordic countries

Moor House, Level 11, 120 London Wall London, EC2Y 5ET *Authorised and regulated by the Financial Conduct Authority (FCA).

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user navigation and to collect statistical data. To refuse the use of cookies, change your settings or for more information, please click on the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.