Nikolay Markov on why Russia's economy is in far better health than many realise.

Written by

Nikolay Markov

Senior Economist

Julian Zbar

EM Product Specialist

Share this article

Grand-Master Putin...

Political developments made my visit to Moscow last week even more timely than originally anticipated. But despite the government’s shock resignation, I remain optimistic about Russia's economic prospects in 2020 and beyond.

The key takeaway is that Vladimir Putin has made clear he will remain head of the Russian state beyond 2024 when, according to the constitution, he is required to step down as President. Stability at the top is positive, as is the installation of the business friendly Mikhail Mishustin as interim prime minister. He offers the prospect of even stronger economic growth in the medium term.

The National Projects initiative is designed to cement Putin's legacy as Russia's greatest ruler since the era of the Tsars.

Details are not final, but it seems the power of the Presidential office will be reduced in favour of Parliament and the State Council, which Putin is likely to head after he leaves the presidency. Putin also announced a number of measures likely to appeal to the public. He said he’d tackle increasing levels of poverty and corruption, and announced a number of family-friendly cash incentives: increases in child benefit; free hot lunches for school kids; and 50 per cent increases in grants for large families.

From my discussions with business leaders, the resignation of Prime Minister Dmitri Medvedev, came as a surprise even to insiders. It seems to have resulted from his disagreements with Putin over the planned constitutional reforms. Furthermore, Mishustin, a technocrat, is arguably a safer pair of hands to deliver Putin's cherished and ambitious National Projects by 2024 (of which more below).

What about the economy?

The Russian equity market should respond positively.

Russian stocks had a sensational 2019, up over 50 per cent in US dollar terms. For more on why this might yet continue please read the analysis of my equity colleague Julian Zbar below. My view is the equity market should remain upbeat, supported by strong foreign demand, lower interest rates, record high dividend yields, as well as the successful implementation of Putin's pension reforms.

Russia has economic fundamentals that would be the envy of many of its developed rivals.

As we said in last month's EM Monitor, we expect Russia's growth to accelerate at a faster rate than almost any other emerging market in 2020.

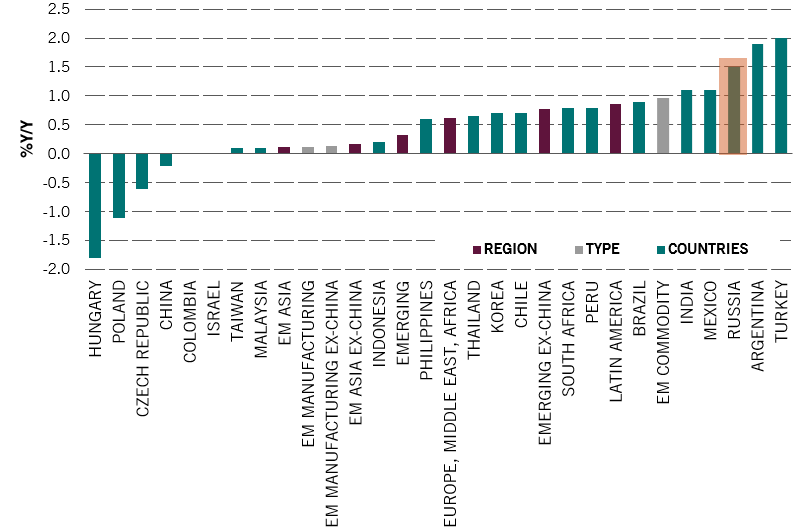

The bear bounces back

Fig.1 - Real GDP growth change: 2020 forecast less 2019 forecast (%Y/Y)

Source: Pictet Asset Management, CEIC, Refinitv, Bloomberg; November 2019.

Guided by our leading indicators, we expect real GDP growth of 2.5 per cent, above consensus forecast of 1.7 per cent (source Bloomberg 20.01.2020). This will be driven by better implementation of the ambitious National Projects and a pick-up in private consumption, supported by looser financial conditions and planned increases in social spending. Other positives are increasing trade activity with China – a repercussion of US trade policy – and sustained oil price strength, which remains Russia’s dominant export.

Strong fundamentals

Russia has some economic fundamentals that would be the envy of many of its developed rivals.

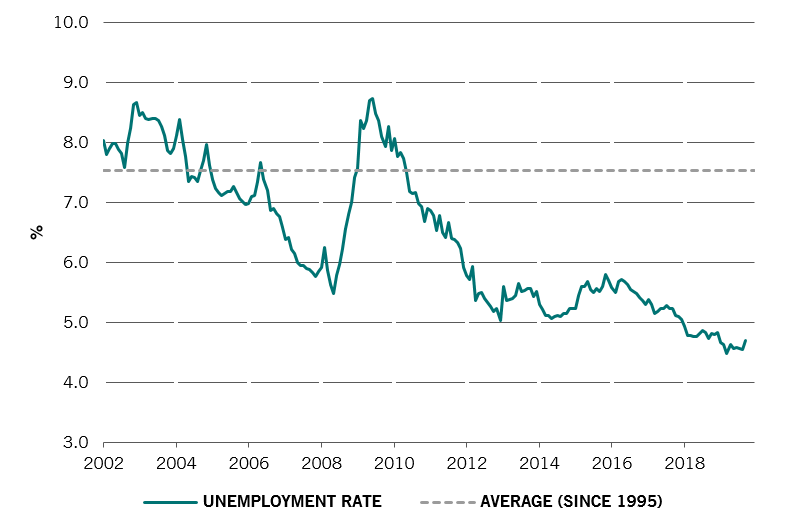

Labour market in good health

Fig.2 - Russia unemployment rate

Source: Pictet Asset Management, CEIC, Refinitiv; January 2020

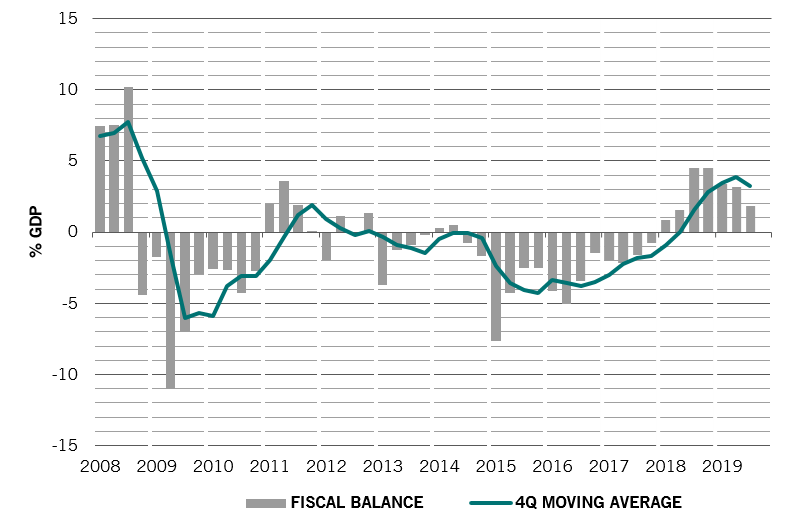

Love fiscally...

Unemployment, for example, remains on a strong downward trend. It is a rarity in running a strong fiscal surplus. It has an enviably low general government debt to GDP ratio of 12 per cent. Inflation appears well under control and trending lower.

Room to spend....

Fig.3 - Russia general government fiscal balance to GDP ratio

Source: Pictet Asset Management, CEIC, Refinitiv; January 2020

And our view is the ruble is still undervalued by 5.3 per cent in trade-weighted terms as of 20.01.2020.

We think all these factors paint a very positive picture for sovereign debt investors.

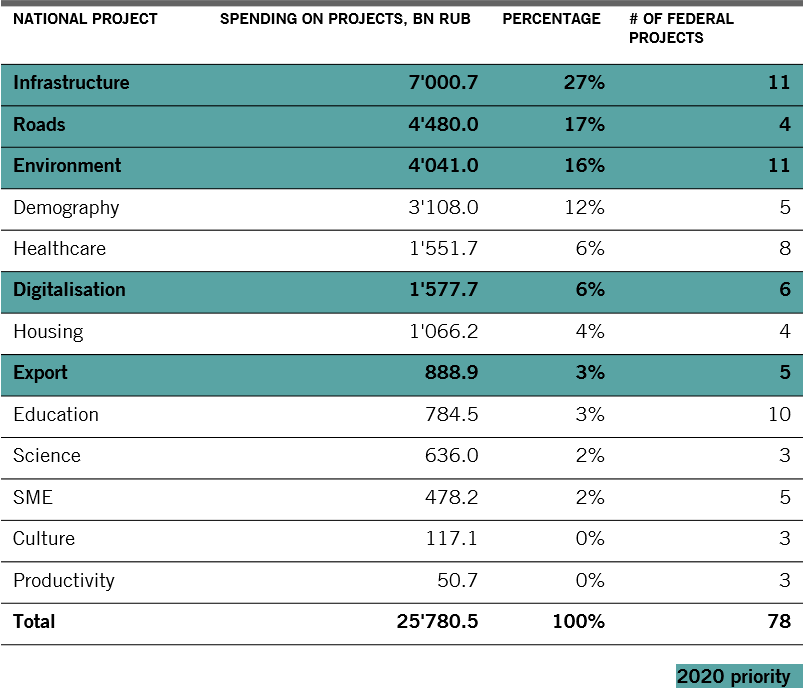

National Projects

It is against this benign economic backdrop that President Putin is launching his RUB 25.8 trillion National Projects initiative, which is designed to cement his legacy as Russia’s greatest ruler since the era of the Tsars.

Worth 23 per cent of GDP, the initiative’s aim is to double the economy’s long-term growth potential to 3 per cent and to reduce its reliance on petrochemicals. Some 60 per cent of the funds are allocated to infrastructure, roads and environment, with the rest going into demography, healthcare, digitalisation, housing, exports, education, science, SMEs, culture and productivity.

National Projects

Fig. 4 - Scope of expenses on National Projects

Source: Accounts Chamber, MinFin, VTB Capital Research. Courtesy VTB, November 2019

In 2020, significant subsidies are being allocated to exporters, while the government is also targeting 100 per cent Internet access for the population.

We expect spending on the National Projects should be stronger in 2020 than last year thanks to robust oil revenues, which should add an additional 0.5 percentage points of growth this year and around 0.3 per year in the following years.

Meanwhile, the increase in retirement age to 65 years for men and 60 for women, should be enough to reverse the negative demographic trend and to increase the working age population in the long run.

All this taken together with a much stronger than reported residential construction activity (focused on the replacement of prefabricated Soviet era housing stock) would make a 2.5 per cent GDP growth for 2020 quite realistic.

The sectors most likely to benefit are metals, real estate and banks. The next 12 months should also be a game changer for the retail sector given the expected pick-up in household spending thanks to real income increases, new maternity support, new social benefits and elevated dividend yields.

The risks?

Thanks to the country’s improved public finances , benign inflation, high stock dividend yields and the potential for acceleration in GDP growth, Russia’s equities have evolved into a low beta market. But there remain clear risks, not least the rule of law.

There might be good macroeconomic policy, but there is weaker microeconomic policy (anti-trust, legal system, lagging in terms of technology networks). In our view, this places a limit on private sector-led dynamism.

Putin's ongoing rule carries political risk. But for investors in Russia recent announcements push out the biggest risk into the mid to long term: namely what happens post-2024. For the foreseeable future, Putin's influence on the Russian economy and politics are to remain unchanged.

THE VIEW FROM OUR EQUITY TEAM

By Julian Zbar, Product Specialist

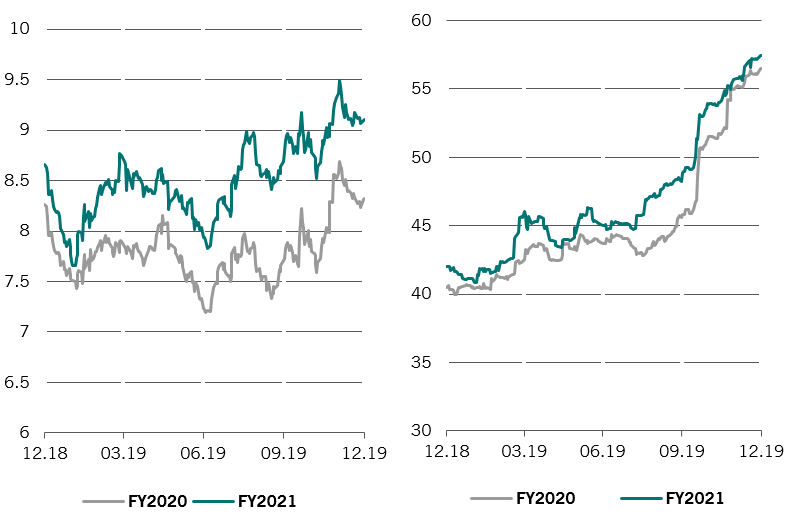

The Russian market, as measured by the MSCI Russia Index, returned 53 per cent in 2019 in dollar terms. But despite the rally, we believe the market continues to offer tremendous value. A 12 month forward price-to-earnings ratio of under 7 times represents a 47 per cent and 60 per cent discount to global emerging and developed markets, respectively*.

Quite remarkably, as the charts below show, the market has actually become cheaper on a dividend yield basis. Russian forward dividend yields for FY2020 and FY2021 have been revised up in the period between December 2018 and December 2019. As at the 31 December 2019, the FY2020 and FY2021 yields are 8.3 per cent and 9.1 per cent respectively.

*As per MSCI Russia, MSCI Emerging Markets, MSCI World. Factset consensus as at 31.12.2019

Reaping the dividends...

Fig. 5a - MSCI Russia forward dividend yield / Fig. 5b - MSCI Russia forward payout ratio

Source: Factset, as at 31.12.2019

Mechanically, over a defined period of time, the dividend yield can only increase if the expected dividend per share increases by a larger quantum than market prices. This has been the case in 2019 as both expected earnings per share and expected pay-out ratios have increased. Forward expectations on dividend pay-out ratios in particular have surged last year. Given the highly cash generative nature of Russian companies today, their very low levels of leverage, the improving distribution policies and, as mentioned above, the stable nature of the economy – we believe these yields are sustainable into the future.

About

Nikolay Markov

Nikolay Markov joined Pictet Asset Management in 2013. He is a Senior Economist, Lead on CEE and Other advanced economies.

Before joining Pictet, he was working in the Monetary Policy Analysis Unit of the Swiss National Bank where he performed research on monetary policy rules for Switzerland. Prior to working at the Swiss National Bank he was a teaching and research assistant at the University of Geneva and participated in international academic conferences.

Nikolay holds a PhD in Economics from the University of Geneva and obtained a PhD program certificate from the Swiss National Bank doctoral institute in Gerzensee.

About

Julian Zbar

Julian Zbar joined Pictet Asset Management in August 2017 and is a Product Specialist in the Emerging Equities team. Prior to his current role, Julian was an Analyst for the Pictet Trading Strategy team within Pictet Trading and Sales, a role he started in April 2016. Julian began his career at Bloomberg LP within Sales, as a Global Account Manager for buyside firms. Julian graduated from HEC Lausanne in 2012 with a BSc in Economics. He is also a Chartered Financial Analyst (CFA) charterholder.

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user navigation and to collect statistical data. To refuse the use of cookies, change your settings or for more information, please click on the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.