Asset allocation: a note of caution

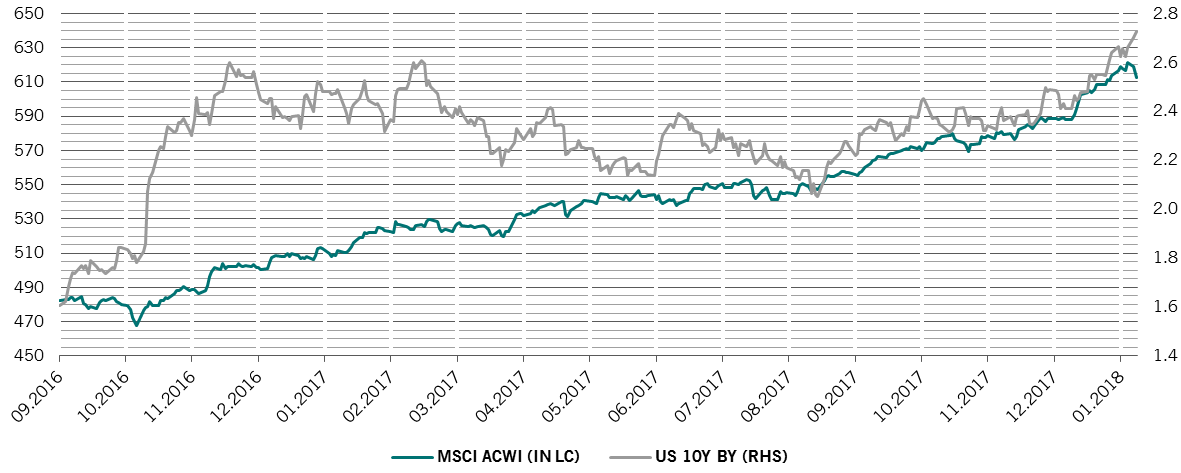

Global stocks kicked off the new year on a strong note, rising more than 5 per cent in January alone, with many bourses reaching record highs. The magnitude of the rally, and a simultaneous spike in yields on US Treasuries and German Bunds, means we now see limited upside for equity markets over the coming months. Hence we downgrade equities to neutral, raise cash to overweight, and keep our underweight stance in bonds, as we expect strong domestic demand and buoyant labour markets, especially in developed economies, to push inflation higher over 2018. What is more, a surprisingly strong rebound in inflation risks a more hawkish-than-expected response from central banks.

Our business cycle indicators show the global economy is on track to grow 3.4 per cent this year, having expanded above 3 per cent in 2017. We have become more optimistic about the prospects for the US. Domestic demand has grown at annualised rate of 4.4 per cent in the most recent quarter, the highest in three years; consumer and business confidence close to record levels; a weak dollar is supporting exports and Washington's tax reform should boost economic growth in the next two years. However, this, in turn, is translating into higher price pressures. US core PCE, the US Federal Reserve’s favourite inflation gauge, has risen to 1.5 per cent; we expect it to breach the Fed’s target of 2 per cent in late 2018.

Economic conditions in the euro zone remain buoyant, although growth may be plateauing.

We are more cautious about China’s economic prospects, however. Economic activity has deteriorated as fixed asset investment has fallen sharply in both the public and private sector. Should debt reduction gather pace, growth could decline sharply.

The rest of the emerging world is faring better; the growth differential between developing and developed economies should widen further after bottoming at 1.7 percentage points in 2016.

Our liquidity readings support a neutral stance on equities. The amount of liquidity provided by the world’s five major central banks is running at 12.5 per cent of GDP, towards the bottom of its two-year range.1 Another red flag is US monetary policy. With inflation on the rise, we expect the Fed to raise interest rates three times this year.

Tighter US monetary conditions are, however, being partially offset by central bank stimulus in China, as well as a weaker dollar, which supports emerging economies.

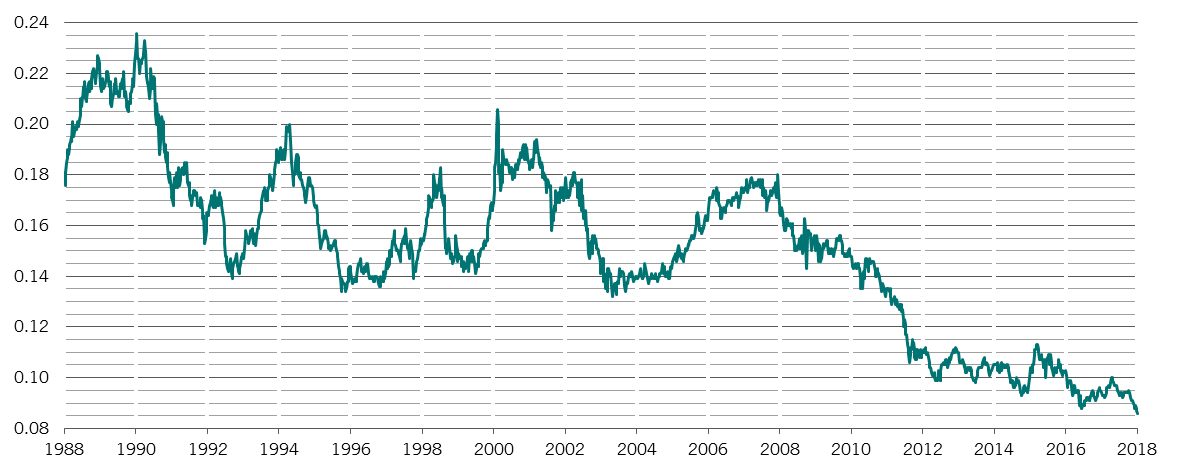

Our valuation gauges suggests stocks have limited room to rise further. With money supply rising at a slower rate than the growth in industrial production2 – a differential that serves as our gauge of excess liquidity – earnings multiples could contract by 5-10 per cent over the course of the year. Also, the scope for company earnings growth to beat consensus expectations is limited given the strong upward revisions to profit forecasts in recent weeks. In the US, we believe that a boost from tax cuts is nearly fully discounted by stock markets, not least because analysts raised their estimates for profit growth this year to 17 per cent from 11 per cent shortly after the tax programme was passed.

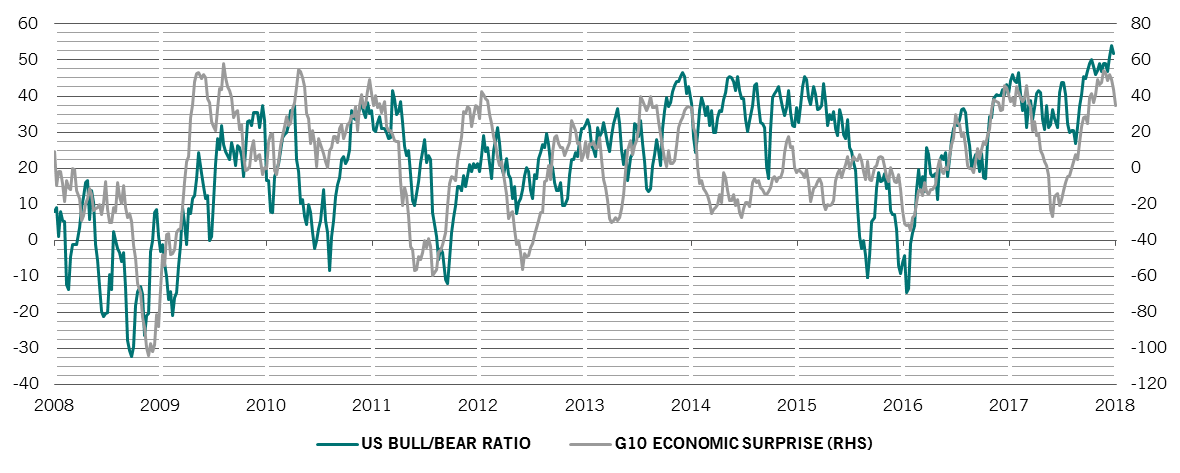

Our sentiment readings have turned negative for equities as they are beginning to signal investor exuberance. The US “bull bear ratio” – which compares the number of bullish and bearish investors – indicates that bulls are firmly in control. Reinforcing the view that investors may be too complacent, IPO activity has been strong and the stock market has seen record four-week inflows of USD77 billion in January into global equity mutual funds and ETFs.3