Select your investor profile:

This content is only for the selected type of investor.

Individual investors?

High yield's turn to shine

A strengthening economy and ultra-low interest rates bode well for European short-term high yield bonds.

Written by

Prashant Agarwal

Senior Investment Manager

Audrey Laurencet

Senior Portfolio Analyst

The global economy is recovering from the effects of the pandemic and corporate earnings are picking up, thanks in part to generous monetary and fiscal stimulus. Interest rates remain at low levels, and are expected to remain so for the long haul. History shows this is the kind of environment in which speculative grade credit does well.

The combination of improving economic and corporate earnings prospects and low debt servicing costs reduces the risk of default. Which means that high yield should continue to be one of the very few areas of the fixed income market where investors can still pick up a positive real return.

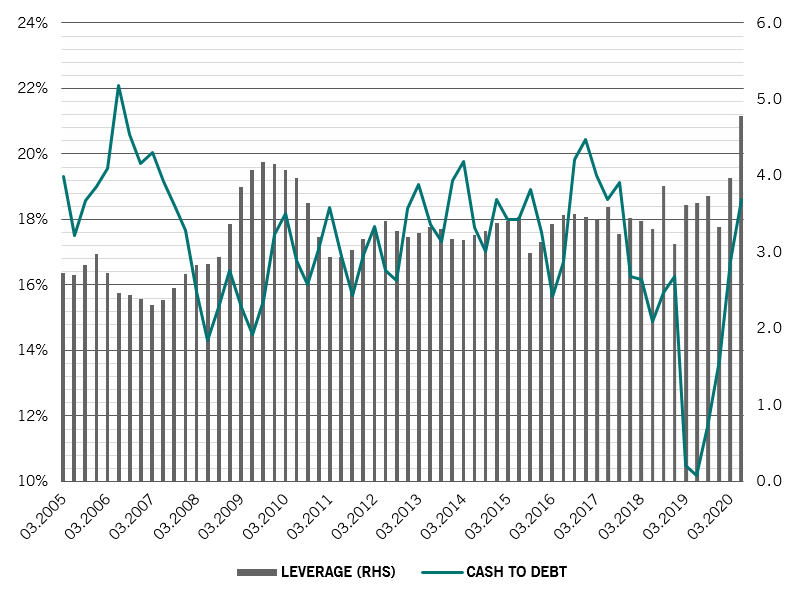

The economic picture is more encouraging than it has been for months. This follows a weak second quarter, when leverage among European high yield companies hit a multi-year high of 4.8 times, EBITDA dropped 47 per cent year-on-year and debt rose by 23 per cent (see Fig. 1). Recent data indicate that activity in Europe is now back to around 80 per cent of pre-Covid levels. Demand for cars, a leading indicator of economic growth, has bounced back to just 20 per cent below its six-year trends vs 80 per cent in the spring. We are therefore confident of seeing further positive surprises – both in macro-economic data and corporate earnings in the coming months. This has yet to be reflected by financial markets.

Fig. 1 - Peak leverage, strong cash

Leverage (times) and cash-to-debt ratio (%) for European high yield

Prospects for speculative-grade companies look better still once fiscal and monetary policy are taken into account. The European credit market has benefited from unprecedent interventions from central banks and governments, which have stepped in speedily to protect viable businesses and limit the number of corporate defaults. The scale and speed of such interventions – which has included programmes such as furlough schemes and government guaranteed loans – have been impressive.

For their part, companies have strengthened their liquidity positions and balance sheets, by drawing on their credit lines, issuing new debt, cutting costs and reducing capital expenditure. The cash to debt ratio among speculative-grade companies in Europe has as a result risen from 10 per cent a year ago to 19 per cent in June 2020.1

Obviously not every company will come through this crisis unscathed – but the impact is likely to be less than originally expected. In March 2020, Moody’s central scenario assumed default rates of 7-8 per cent default rates for high-yield issuers. Since then, however, conditions have improved, prompting Moody’s to cut its default rate forecast to 4.9 per cent in August. There is a strong chance that defaults have peaked. Corporate Europe is in stronger health.

The opportunity set

Some investment opportunities are more attractive than others.

Bonds issued by French and German companies, for example. Among major developed nations, France and Germany led the way in terms of support for businesses with packages worth EUR16.2 and EUR14.3 billion respectively – more than double that of third-placed Italy.2

The pandemic has also deepened the pool of attractive high-yield bonds. The economic fallout from Covid-19 has caused a spike in the number of fallen angels, companies that have just lost their investment grade status. In the first eight months of 2020, Europe saw some EUR45 billion of fallen angels and that amount can be expected to nearly double by year-end.3 This creates a long term opportunity as many of these firms are strong, resilient businesses. The addition of fallen angels increases the size and improves the quality of the high yield market – augmenting an already large cohort of BB-rated companies.

This year’s pandemic shock has been different from the 2008 financial crisis as far as its impact on individual industries is concerned. In 2008-9, financials were the hardest hit; industrial companies also suffered as is common during recessions. This time, however, many factories were able to continue operating partly thanks to increased automation. Chemical and shipping companies fared much better in this crisis than in 2008-9. Instead, the economic impact was most felt by the services sector. Market pricing has yet to reflect this resilience in our view.

Elsewhere, in some of the hardest hit sectors like travel and retail, there is a tendency for all companies to get tarnished with the same brush despite possessing very different financial profiles. An online travel agency with limited fixed costs, for example, is in a far stronger position than a car rental operator. DIY shops have also held up relatively well as families spent more time at home and decided to improved their dwellings. Retailers with e-commerce operations have also proved resilient while those who rely on physical outlets have suffered.

Consequently, retail focussed real estate investment trusts (REITs) are among the worst hit, while residential REITs fared much better. The sports ban and closure of gaming avenues has benefited gaming companies with online presence.

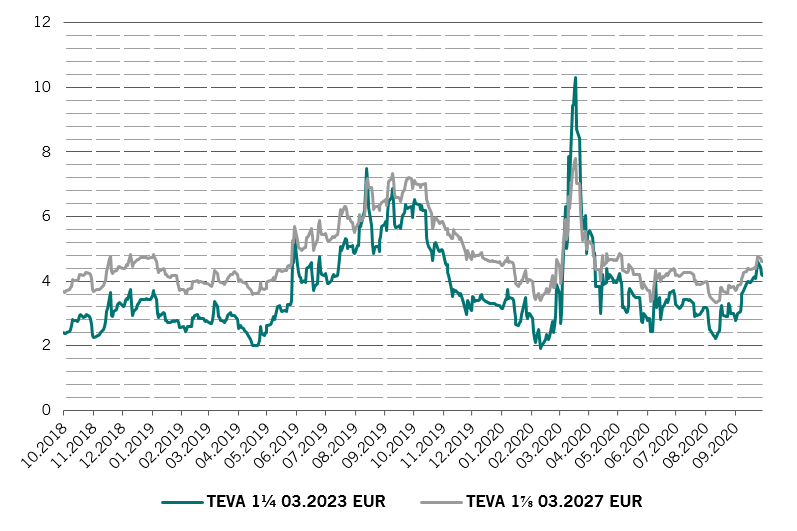

Fig. 2 - Flat curve

Teva Pharmaceutical Industries' bonds compared, yield to worst (%)

With central bank and governments both focused on providing financial support that extends out by months rather than decades, shorter dated credit is particularly appealing. The high yield curve is nearly flat. For instance, Teva Pharmaceutical Industries’ 2027 bond is currently trading only 42bps wider that its 2023 bond (see Fig. 2). By investing in shorter maturities investors thus get similar return while taking on less duration risk.4

We believe the flat curve reflects doubts about the sustainability of the economic recovery and corporate prospects. If such concerns turn out to be misplaced, the curve will likely revert to its usual upward-sloping shape, creating an additional source of return for short-term bonds.

Overall, then, the spread offered by short-term high yield bonds provides more than adequate compensation against the risk of default. We expect European short-term high yield credit will generate positive returns of 3-5 per cent in the next 12 months. As compared to other alternatives within fixed income, this is an opportunity not to shrink away from.

read more about fixed income investing

Chinese onshore bonds: going mainstream

The inclusion of renminbi-denominated debt in the flagship global benchmark bond index will transform the asset class into a strategic investment.

February 2020

Strategic credit: a nimble approach for an uncertain world

Jon Mawby discusses the advantages of active credit allocation in portfolios now that government bonds no longer serve their traditional purpose.

September 2020

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer. This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.