Asset allocation: steady course through troubled waters

Clouds are gathering over the global investment landscape: Washington and Beijing are rattling sabres on trade, the US Federal Reserve has become more hawkish and world economic growth has turned lower at a time when earnings forecasts are running stubbornly high.

Some turbulence is to be expected across financial markets, but we do not think it will turn into a full blown storm. This is a time for a steady hand on asset allocation rather than for rash movements in or out of major asset classes.

April 2018

On balance, our analysis suggests retaining a neutral stance on equities, and an underweight on bonds, which are already feeling the pinch from tighter monetary policy. Given the relatively jittery investor sentiment and the potential for more short and sharp market jolts, we also favour an overweight in cash – both to reduce risk exposure and to be ready to invest in any opportunities that may arise.

Firstly, we believe an all-out trade war is in no one’s interest, and therefore some kind of compromise will probably be reached. The more conciliatory moves from the US administration in recent days – including the recent trade agreement with South Korea – support this view.

The economic outlook is also not as worrying as it may at first seem. While the momentum of world growth shows signs of topping out, at 3.6 per cent annualised it is still running well above potential. Our business cycle indicators show the US looking particularly strong, with its leading indicator hitting a six-year high. We therefore see scope for the world’s largest economy to beat consensus forecasts in the second quarter of the year, as President Donald Trump’s tax cuts boost business investment. On a global level, that should help to offset the weaker activity in China’s industrial sector.

True, the expansion will probably still fall short of the lofty levels factored into earnings forecasts (see “Regions and sectors”). But any disappointment may be easier to swallow after the recent market correction, which has pushed stock prices down to much more sustainable levels.

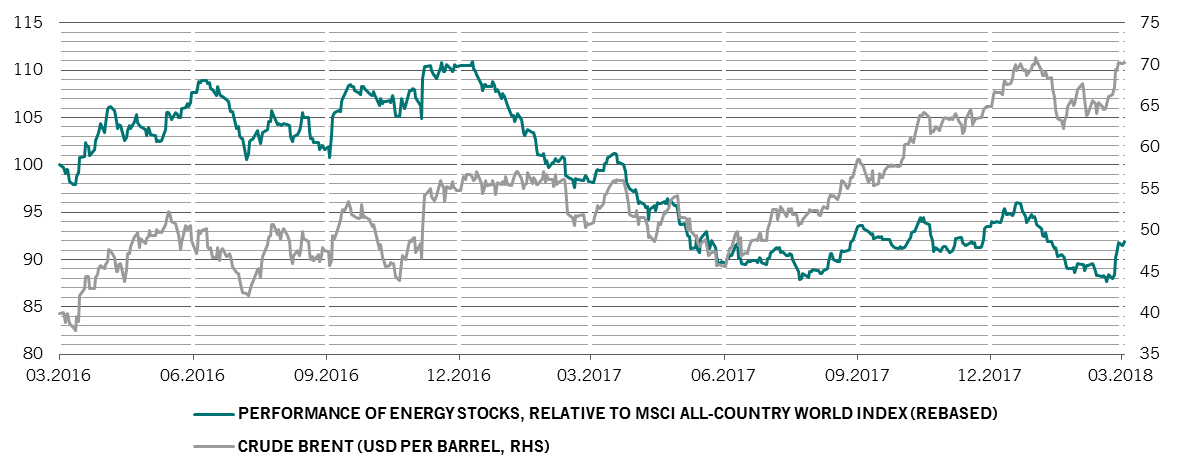

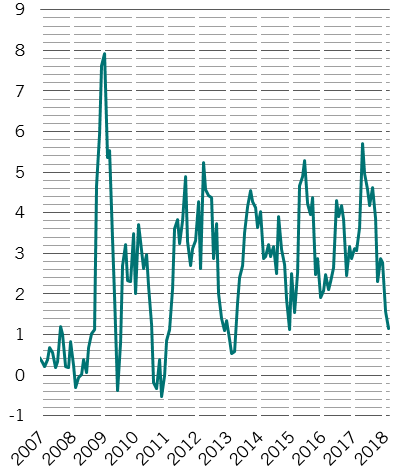

Liquidity is getting tighter, but in a steady and controlled manner (see chart). According to our indicators, liquidity in the US tightened in January, while conditions in Japan turned to neutral from expansionary in February, and those in the euro zone followed in March. We would expect this trend to continue, leading to a gradual – rather than sudden – increase in bond yields. We are also closely watching the rise in short-term LIBOR rates in the US for signs of further tightness in funding markets.

According to our valuation model, equities have moved from expensive to neutral for the first time since August last year. This is true regardless of whether you compare prices to earnings, book value or dividends.

Technical indicators show particularly negative trends in investment grade and high yield bonds, in contrast to positive signals on emerging market local currency debt. We also take comfort in the fact that the extreme levels of short positioning in VIX futures has completely been reversed, which reduces that vulnerability for the market.