Asset allocation: more pain to come

The global economic outlook is darkening again as tighter monetary policy around the world and surging energy prices continue to undermine consumer confidence and corporate earnings growth.

Major economies are flirting with a recession. Europe is feeling the chill more than most other regions as the soaring cost of living and energy shortages force consumers to tighten their belts, banks to slow lending and companies to delay capital spending plans.

All of this augurs badly for corporate earnings in the coming months.

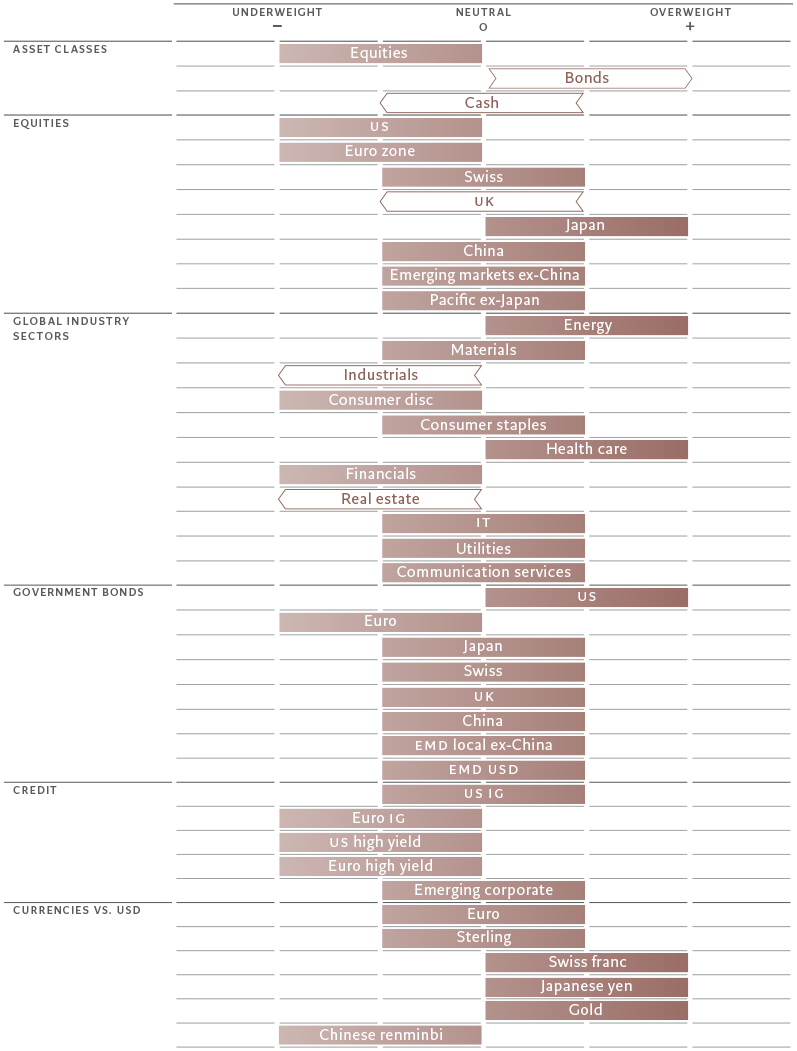

While the equity market sell-off this year has driven investor risk appetite to record lows – a point where stocks and other risky asset classes tend to stage a rebound - we see risks of a further correction. This is why we maintain our underweight position in equities.

We’re unlikely to change this stance until we see stabilisation in corporate earnings revisions, a steeper yield curve and a further cheapening of cyclical stocks.

By comparison, some areas of the bond market are beginning to look attractive, however, as yields are climbing to levels that are increasingly at odds with economic fundamentals. Headline inflation has likely peaked in the US, with inflation expectations also having slipped in recent months. The New York Federal Reserve’s monthly survey shows that consumers in August saw inflation at 5.75 per cent over the next 12 months, the lowest since October 2021. Against this backdrop, we upgrade bonds to overweight, with a preference for US Treasuries – a haven in times of turbulence. We also cut cash to neutral.

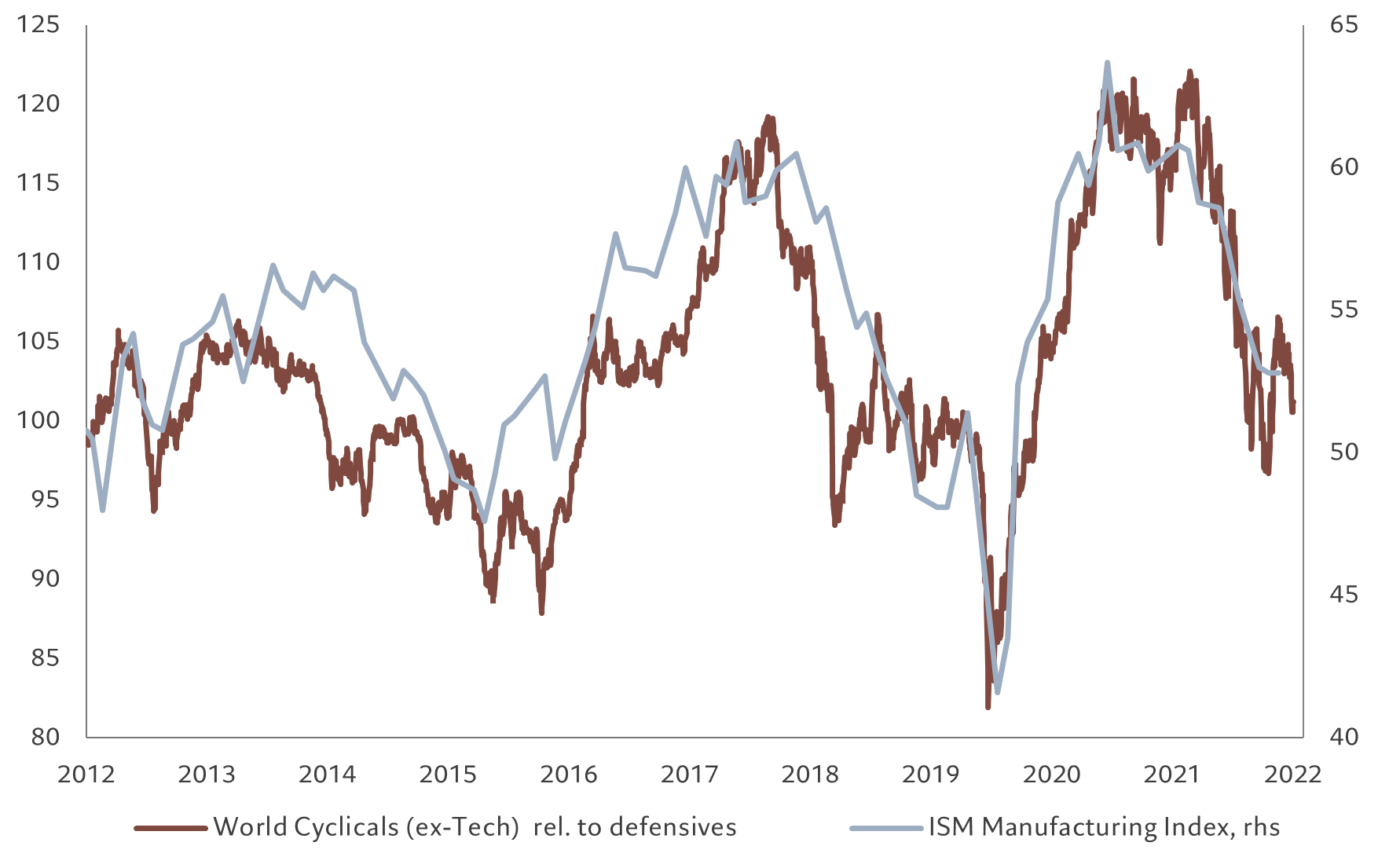

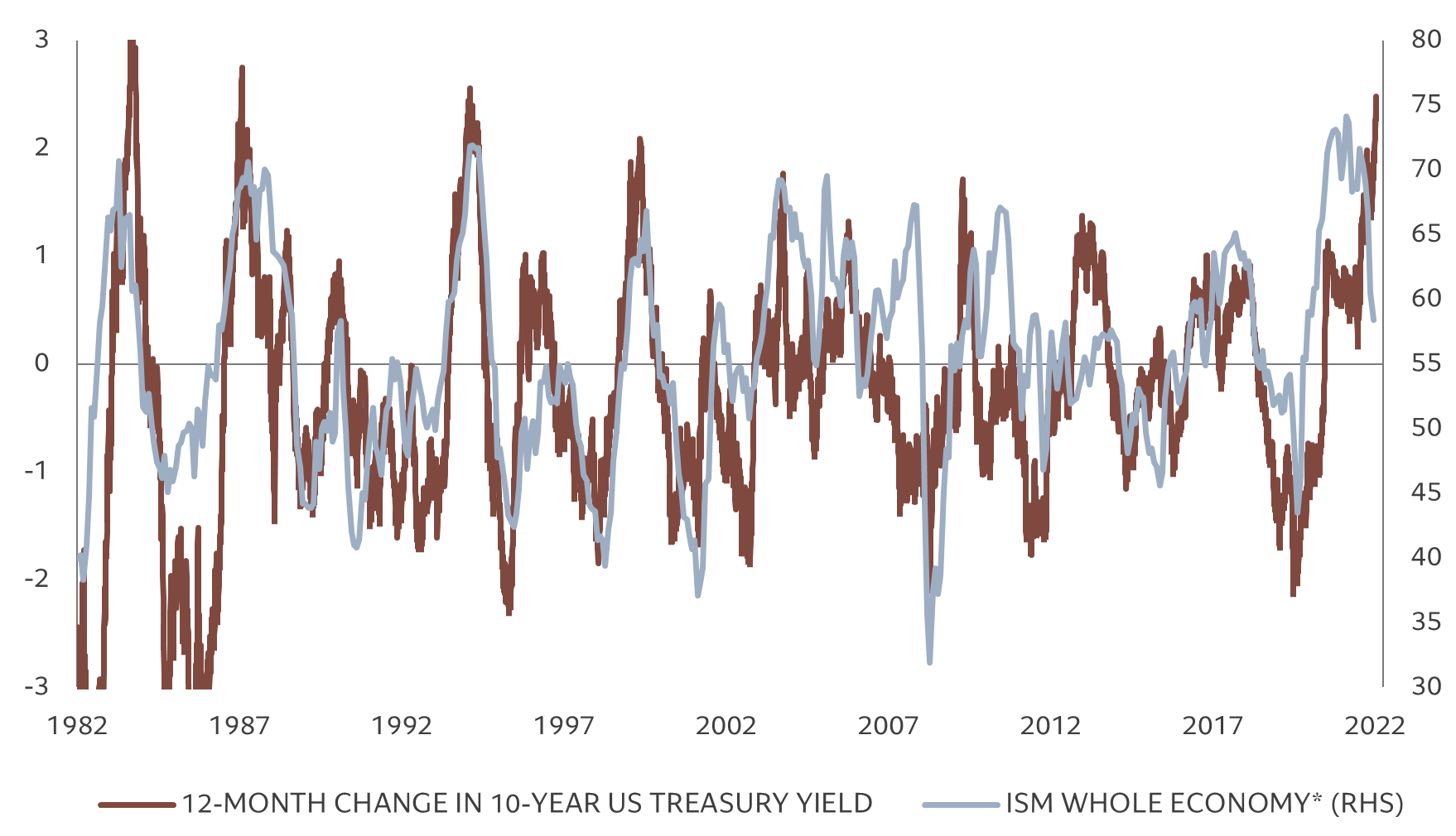

Our business cycle indicators show a clear slowdown in global economic growth. As Fig. 2 shows, rising borrowing costs tend to exact a heavy toll on global business conditions.

The outlook has deteriorated in the euro zone in particular, where consumer confidence has plunged to an all-time low and energy rationing poses further risk to industrial sectors. With the euro zone economy expected to contract towards the end of this year, we have cut our 2023 real GDP forecast to 0.2 per cent from 1 per cent.

The growth outlook is also weak in the US, although there are some positive signs that testify to the resilience of the world’s largest economy. The US labour market remains tight with jobless claims now trending down. Consumer confidence, meanwhile, has improved for the second consecutive month thanks to easing inflation worries.

That said, surveys also show companies remain reluctant to boost their capital spending while the housing market is confronting a slump in construction activity, pointing to a further 10 per cent decline in property prices over the next six months.

What’s more, typical mortgage payments as a proportion of income stand at their highest levels since the 1980s.

We’re becoming cautious on Japan’s economy whose leading indicators have slowed down. Manufacturing activity is contracting and weak global demand is pressuring the export sector.

The prospects for the UK economy remain weak, too.

The government’s plans to deliver the biggest tax cut since 1972 and ramp up borrowing at a time when the country’s consumer price index hovers close to a 40-year high has led investors to question the country's fiscal credibility, giving rise to a sharp sell-off in sterling and gilts.

Consumer confidence stands at an all-time low with inflation-adjusted wages expected to contract 5 per cent. We expect the UK economy to fall into recession from the fourth quarter of this year with full-year growth to be at zero next year.

Our liquidity indicators show tighter conditions in major economies, especially in the US and UK, as central banks continue to reverse pandemic-era monetary stimulus.

At the same time, bank credit, which has until recently partially offset the effect of central bank tightening, is finally slowing down, in line with leading indications from credit standards.

China is the only country showing easier liquidity. The People’s Bank of China is lowering funding costs and offering targeted easing measures to revive credit demand.

Our valuation model backs up our positive stance on bonds.

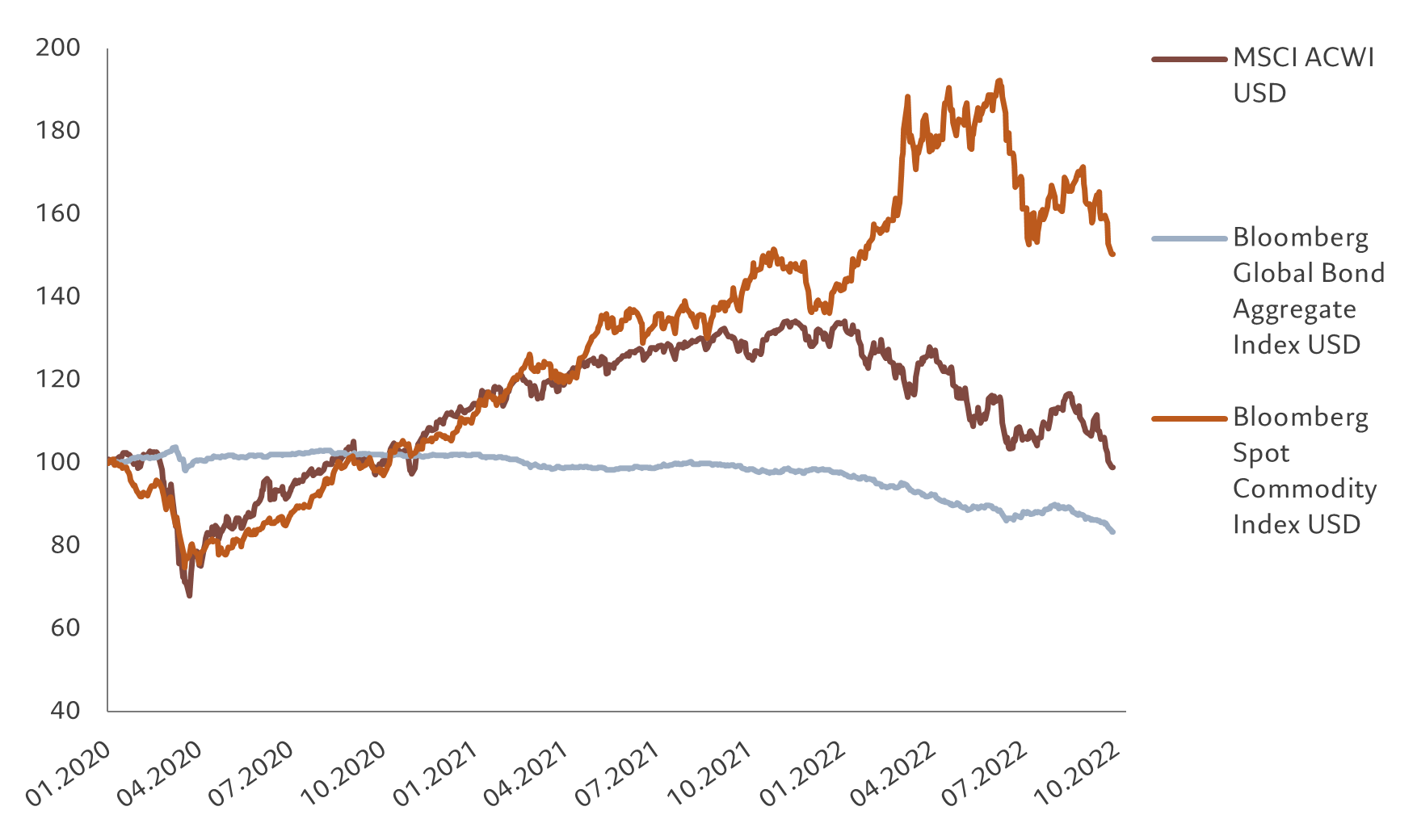

Global bond yields are now at the highest since mid-2011 following a recent sell-off.

Equities are on the verge of becoming cheap for the first time since April 2020 after a 9-per cent decline in world stocks in September alone – which was driven entirely by a contraction in earnings multiples.

As a result, the global 12-month price earnings ratio has fallen to 13 times, below the low seen in June.

What is more, the pace of contraction is consistent with a sell-off typically seen during a recession.

Our models suggest a rebound in multiples of 5-10 per cent over the next 12 months, assuming that 10-year yield on US Treasury Inflation Protected Securities (TIPS) falls to 0.75 per cent.

Our 2022 global earnings growth forecast, meanwhile, stands at 2 per cent, significantly below market consensus.

Within equities, we’re becoming more cautious on cyclical sectors that are growth-sensitive, such as industrials and real estate.

Our technical indicators show investor risk appetite close to record low levels, with equity funds losing USD25 billion in flows in the past four weeks.

While a technical rebound cannot be ruled out at this depressed sentiment level, our negative trend score suggests taking an underweight equity position over our investment horizon.