Overview: Less of the same

For all the fears that markets are at a turning point, next year is likely to result in a continuation of 2021’s trends, albeit with ‘less of the same’. The economic and market recovery triggered by the removal of Covid lockdown measures is intact, if in its final phases.

Record valuations, tighter monetary policy, expansionary fiscal measures and surging inflation point to modest gains for equities in 2022 following the market’s robust recovery from pandemic lows. A US rate hike next summer will push up global bonds yields, though the magnitude of the move will be mitigated by the fact that the US Federal Reserve and other central banks remain concerned about maintaining growth and employment rather than sticking narrowly to their inflation remits.

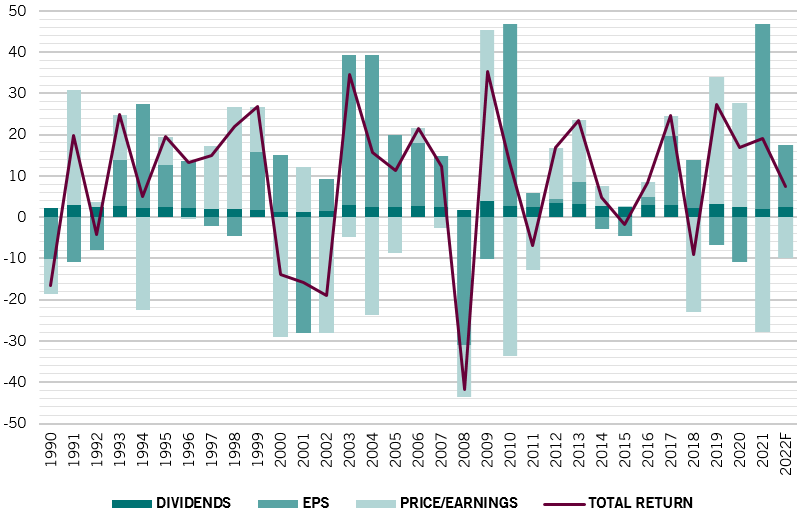

Based on our asset allocation framework, which takes into account economic conditions, liquidity, asset class valuations and technical readings, we expect equities to deliver single-digit returns for global stocks in 2022, with strong growth in corporate profits more than offsetting a contraction in equities’ earnings multiples.

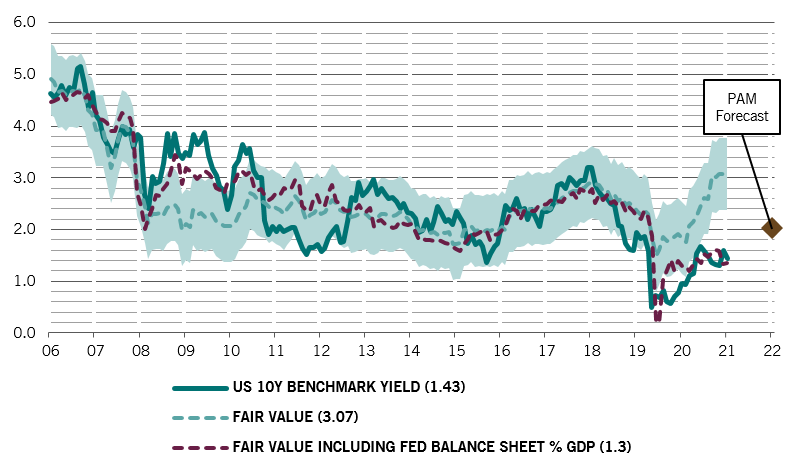

Conditions for bond markets will be tougher, however, with US Treasuries (which set the trend for the fixed income market generally) expected to post losses on the year even though yields on the 10-year note will struggle to rise above 2 per cent. With real yields on inflation protected bonds at an all-time low, this part of the market will also fail to deliver for investors. In currency markets, the dollar will remain well supported despite trading well above fair value, largely thanks to the relative strength of the US economy.

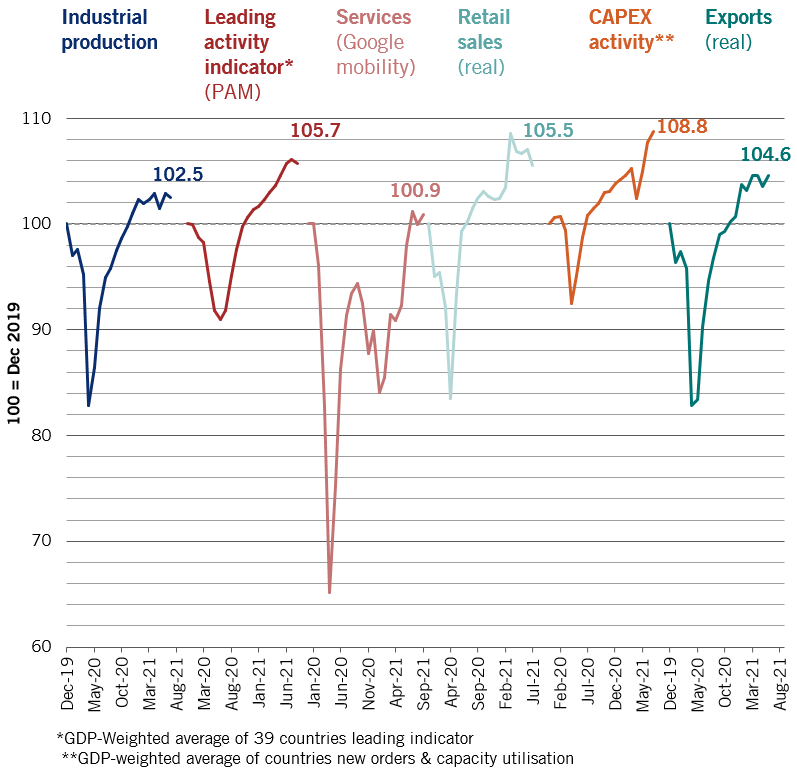

Global economic indicators, Dec. 2019 = 100

We believe the global economy will remain strong – at the very least returning to pre-pandemic trends of activity – with both growth and inflation above trend for another year. Vaccines, new anti-viral therapies and sensible precautions should limit the impact of Covid.

Consumption of services should pick up, closing the gap with goods consumption – and there’s significant upside here: hotel bookings and air travel reservations are still less than half of their pre-pandemic levels. At the same time, supply bottlenecks should ease with the lessening of mobility restrictions in key Asian economies . Not only will this feed end demand, but it will also allow for depleted inventories to be restocked. Overall, growth looks set to be comparable across regions and sectors and by the end of the year, and the global economy will broadly be back to normal (see Fig. 1).

Overheating risks

Although with inflation marching higher there are concerns about stagflation, if there is a risk to our base case scenario, it’s that economies will overheat. Record corporate profits are boosting investment, while strong growth in both jobs and wage will feed through into higher consumption, as will a drawdown in what are record levels of excess savings globally. Notwithstanding some parallels with the 1970s, the global economy won’t be hit by a structural inflationary shock equivalent to the end of Bretton Woods, and thus the gold standard, in 1971.

For the first time in living memory, the US economy will outperform China’s, growing at 5.6 per cent in 2022; it will also register a positive output gap - one that the IMF estimates will be the largest in three decades. Inflation, driven by demand, will persist and unemployment will fall. Europe and Japan will also continue to recover, although lagging the US. We expect a similar outcome for the UK but with Brexit and potentially coordinated monetary and fiscal tightening creating uncertainty.

As for China, the start of the year is likely to be weak, a hangover from past monetary tightening and 2021’s regulatory clampdowns. But the second half of the 2022 should see a brisk recovery – with the caveat that there’s significant risk of a policy mistake that could damage the property sector, which accounts for a quarter of national output.

Even though, on balance, we sanguine about global growth, there are three specific risks to consider. Rising inflation – for instance a rapid surge in oil price to USD100 a barrel and beyond– could seriously dent demand. Further regulatory clampdowns in China can’t be discounted, either. And then there's Covid– or more specifically the possibility that an even deadlier new variant that evades current vaccines could arise.

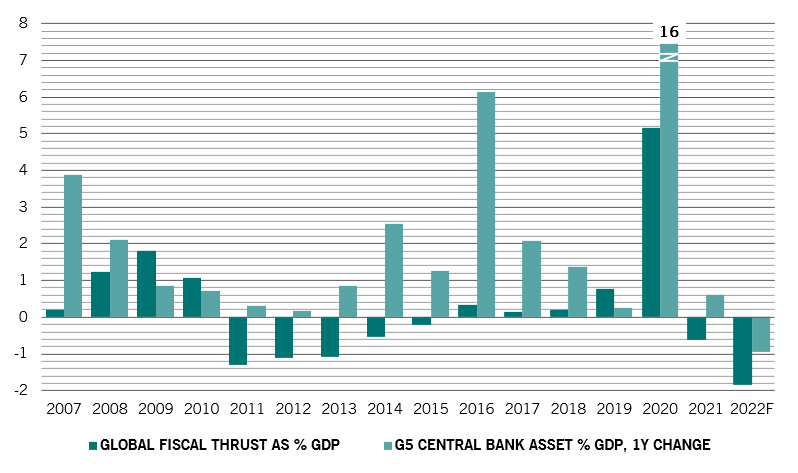

Global fiscal and G5 monetary stimulus, % of GDP

Monetary policy is set to become less loose in 2022 (see Fig. 2)– even if there’s no outright U-turn. Emerging economies have already started to tighten and their real rates stand at 3 percentage points above those in developed markets, which is close to previous cyclical peaks. We expect the major central banks to expand their aggregate balance sheet by some USD1 trillion next year , compared to a USD2.7 trillion expansion in 2021. That’s less than the expansion of overall economic activity, meaning that excess liquidity will be shrinking for the first time since the global financial crisis. Nonetheless, real interest rates will remain negative despite the Fed’s tapering of quantitative easing and its expected rate hikes at the back end of next year.

Although the US central bank will be monitoring economic developments, it’s hard for it to shift track once a policy course has been settled on. For example, in December 2015 it hiked rates even though core inflation was well below target and leading indicators were hinting at economic contraction.

By contrast, the European Central Bank appears to be considerably more reluctant to move towards policy tightening. There’s more of a mixed outlook for the Chinese central bank which is having to balance between a soft economy and rising inflation.

Historically, at the start of a US monetary tightening cycle, equity returns drop to below the long-term average, though performance still tends to be positive. Any sudden declines in prices or increases in market volatility tend to be short-lived, even if they can be severe at times.

But the warning stands: asset prices generally are richly priced after a decade of quantitative easing and cheap money and rising demand for financial assets from ageing populations. True, there remain pockets of value – energy, mining, Chinese property, Brazilian and Turkish equities, for instance – but many of these assets are all but uninvestible for many investors. Instead, investing has become a matter of finding relative attractiveness. Even so, as former Fed chairman Alan Greenspan once said: “history has not dealt kindly with the aftermath of protracted periods of low risk premiums.”