The analysis provided in this study makes a strong case for the inclusion of thematic equities in a diversified portfolio.

A potential shortcoming of this analysis is that the data were taken during a period in which equity markets were enjoying an almost uninterrupted rally thanks mainly to exceptionally low interest rates.

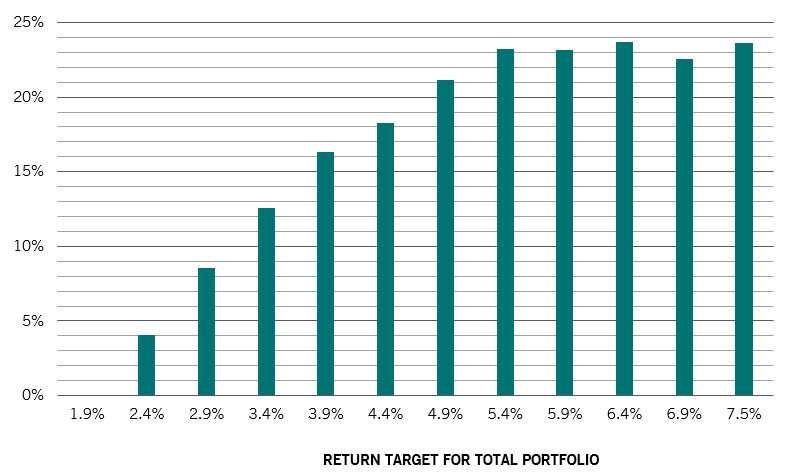

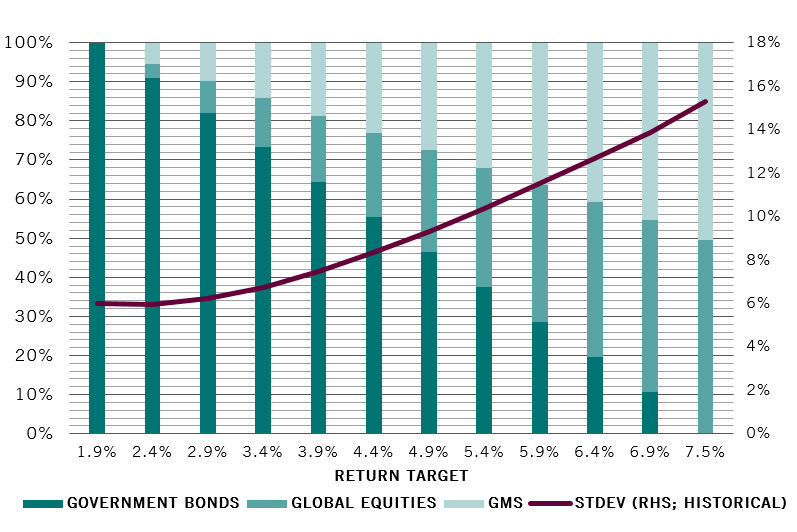

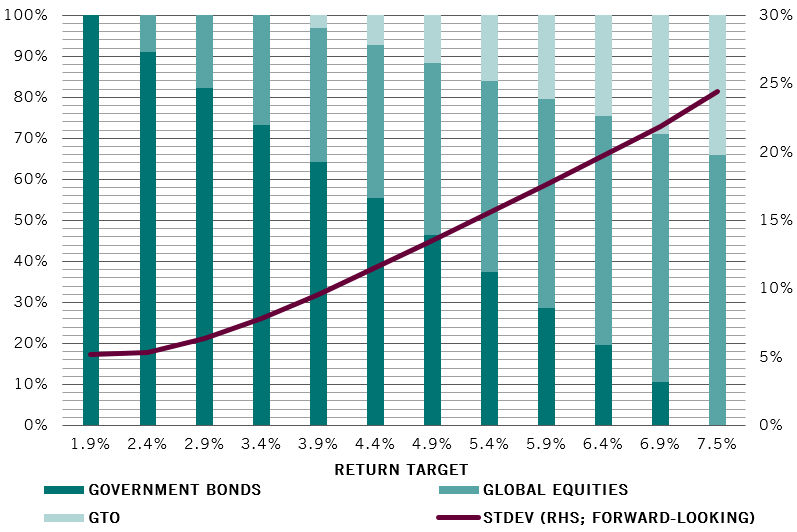

During this period, thematic equities have on average outperformed global equities. However, the results are not heavily reliant on forward-looking return assumptions. For a number of optimisation runs, no return advantage was assumed for thematic over global equities. In other instances, when the portfolio’s estimated risk was higher, the excess return required to justify a significant allocation to thematic stocks was a modest 25 basis points per year.

This means that, for these results to be no longer valid, it would require a profound change in both the correlation of returns between thematic stocks and mainstream asset classes and in thematic stocks’ risk.

While we cannot exclude this possibility, such a scenario looks improbable - thematic stocks should retain their distinctive risk-return profile. This is likely for a number of structural reasons.

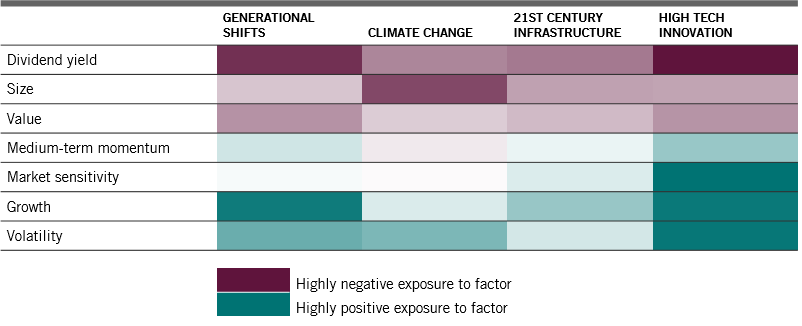

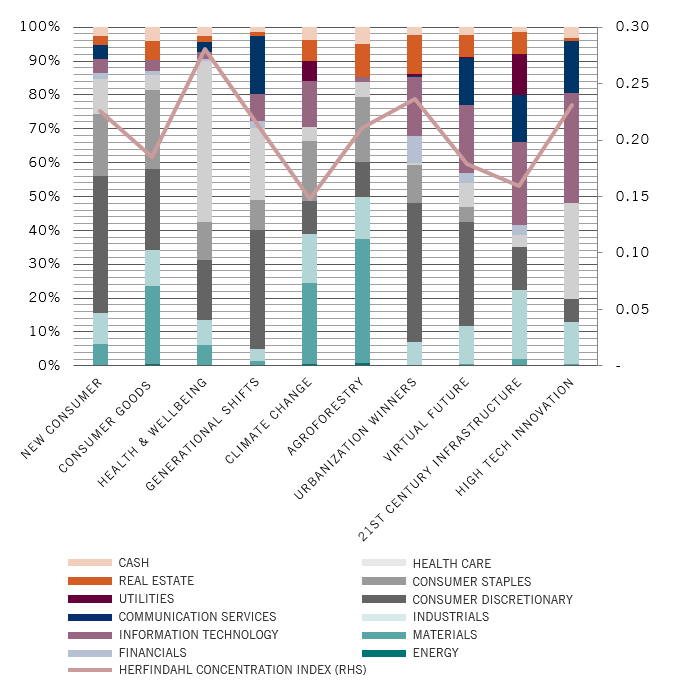

To begin with, there’s the make-up of thematic investment universe itself. It consists to a much less degree of large mega-cap companies than traditional indexes. This has significant investment implications.

There is a large body of evidence showing that the stocks of specialised firms do better than those of large, diversified companies over the long run. Essentially, large firms suffer from what is known as the “conglomerate discount”. Put another way, broadly diversified companies are worth less than the sum of their parts.

Thematic equities have on average outperformed global equities.

By contrast, specialised firms – sometimes known as “pure play” companies – typically have a much clearer view of their strategic priorities and concentrate spending in areas that promise the strongest growth. Their capital allocation is more efficient which, in turn, builds a premium into their share prices over time, the BCG research found. Our thematic strategies are designed to take advantage of this tendency. For each thematic strategy we manage, there are explicit rules for the construction of the portfolio. Each stock must have a high “thematic purity” for it to qualify as a potential thematic investment. Thematic purity is a proprietary, numerical indicator of how specialised and thematically-aligned a company’s activities are.

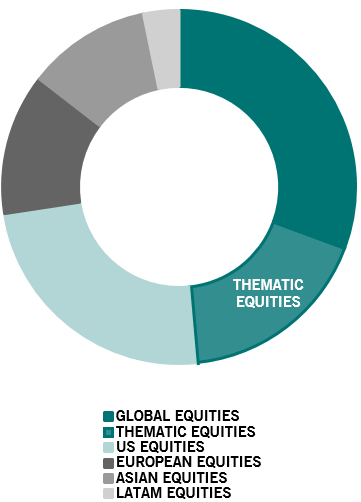

Companies that qualify as thematic investments share another attractive attribute that has a bearing on investment returns. Because they are specialised in their activities, they have little in common with the huge, diversified multi-nationals that dominate mainstream equity indices such as the MSCI World or the S&P 500 Index.

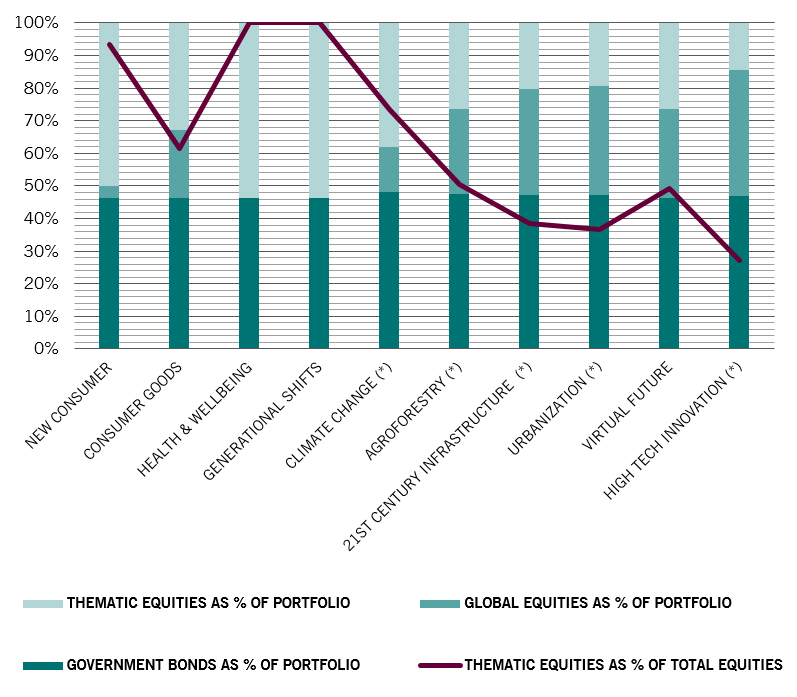

This carries over to the portfolio. The investment approach is index-unconstrained, delivering a portfolio that bears little, if any, resemblance to those whose reference index is a mainstream equity benchmark. Thematic strategies’ high active share is an indication of this.

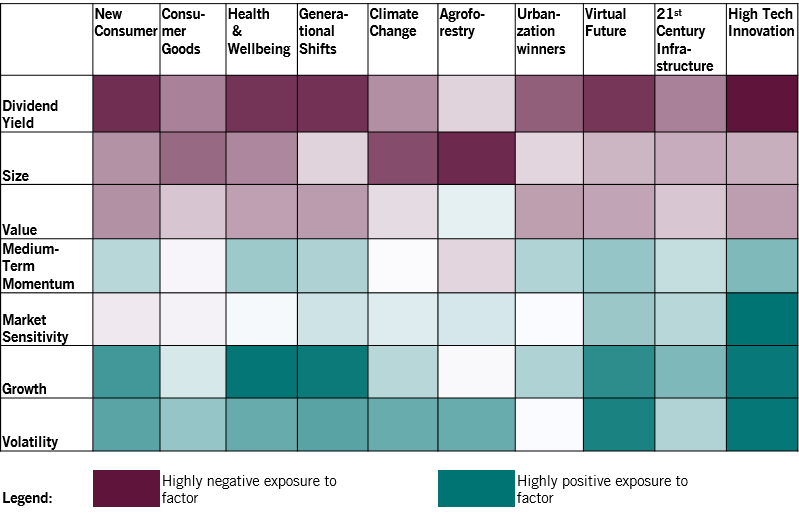

And while the risk and performance of thematic equities may vary over the different phases of the market cycle, their structural design features should lead to portfolios with market characteristics that are relatively predictable over full market cycles.