The water efficiency challenge

At a time when the world is consuming its natural resources at an unsustainable pace, businesses should do more than reduce their carbon footprint. It's vital they cut their water use, too.

Written by

Marc-Olivier Buffle

Head of Thematic Client Portfolio Managers and Research

Cédric Lecamp

Senior Investment Manager

The world is waking up to the need to protect the environment for future generations. Cutting carbon emissions is a step in the right direction – one for which businesses are increasingly being held to account, whether that's by regulators, consumers or shareholders. But it is not the only step the corporate world needs to take. Restricting water use is another battleground in the fight for sustainability.

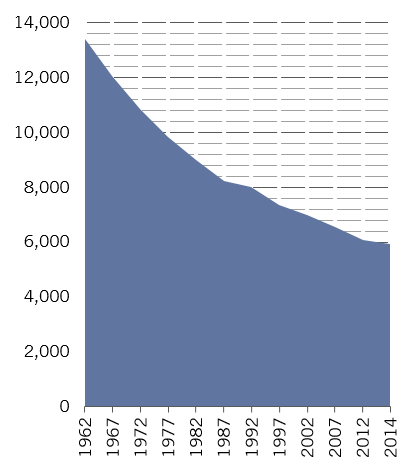

Fig. 1 Running out of water

Global renewable fresh water resources per capita (cubic metres)

Measuring and comparing water useage across industries is the immediate priority. One starting point is the Planetary Boundaries framework, a model that establishes numerical limits for the nine most damaging environmental phenomena facing the planet, from climate change and freshwater use to biodiversity loss and land use.

The framework, developed by the Stockholm Resilience Center, suggests we can sustainably consume up to 4,000 billion cubic metres of freshwater per year – broadly in line with current useage levels, according to some estimates. But by 2030, world water demand is forecast to reach 6,900 billion cubic metres, far exceeding accessible and reliable supplies.1

Around a fifth of all the water used is consumed by industry. Which means businesses have a major role to play in re-imagining how we use and recycle this precious resource. For the world to stay within sustainable boundaries, research shows that businesses should use no more than 52,915 cubic metres of water for every million dollars of revenue they generate.2

Companies that restrict their use in this way are rewarded through cost savings and the reduced risk of exposure to water shocks. They are also more likely to win favour among increasingly environmentally conscious consumers and regulators.

Fair comparison

As with the fight to cut carbon emissions, investors have a key role to play, both by encouraging companies they invest in to embrace water efficiency, and by actively seeking out businesses which have shown particular innovation and progress in this regard.

Ceres, a research and advocacy group focused on sustainability issues, has launched a toolkit to help investors understand water risks and incorporate them in the portfolio allocation process, identifying sectors by high, medium or low exposure to water-related threats. The Boston-based group also suggests that investors make a concerted effort to influence companies’ water risk through shareholder engagement.

The United Nations, meanwhile, has created the CEO Water Mandate and, through its Sustainable Development Goals (SDG), is pushing for universal access to safe water and sanitation.- an initiative that has secured the backing of large, thirsty companies such as Coca Cola, Nestlé, Unilever and Siemens.

The UN focuses on a metric it calls water use efficiency (WUE). This effectively captures the gross value-added economic activity per unit of water consumed by a country, industry or company.

Before WUE scores can be used to inform investment decisions, however, it is essential that they are both comparable and give a true reflection of each company’s exposure. For now, this is probably not the case. WUEs range widely even for companies in the same sub-sector, let alone industry.

Take brewing, a big water user. Overall, the industry produces some 1.9 billion hectolitres of beer a year,3 and – from crop cultivation to consumption – uses at least 60 times as much water in the process.4 Yet within the industry there are huge variations in water consumption from one brewer to another. One international brewer, for example, has reported a WUE score of USD1,850 of gross value-added economic activity per cubic metre of water consumed, while its rival only manages USD270.

The issue is that while the better-scoring brewer is clearly further advanced on the water efficiency path, it is at present hard to do a fair comparison as the calculations can vary widely.

Fig. 2 The full story

Global average water use in production of a t-shirt and the stages involved

For the data to be meaningful, companies must consider their water use across the whole production chain – something which many currently do not do. A typical clothing retailer, for example, will use relatively little water. That ignores the fact that the cotton, from which the garments are made, is very water intensive to produce. Looking at the operation in isolation of its supply chain and products usage downplays the role the company can have in global water efficiency (in this case by raising the issue with their suppliers). It also downplays the extent to which it could be negatively effected in case of a water shock.

What makes the issue even more complicated is the fact that water is a local problem – large reserves in one country cannot effectively be transferred to deal with a drought in another. The location of a company, therefore, can strongly affect the likelihood of it being subjected to water risk and the degree to which it sees water efficiency as a priority.

Investors can help establish standards and promote accountability. It is in our interests to do so – businesses which do not embrace water efficiency face increased risks not just from water shortages, but also from changes in regulation and from increasing environmental consciousness among consumers. Much as the carbon footprint is today becoming a consideration in the construction of portfolio construction, water use can in future be an important input.

Circular approach

Being water efficient means not only means using less, but also reusing more. Some of the world’s leading industries are already adopting a circular economy approach, treating waste water as a resource rather than as something to be disposed of. As our society – from politicians to consumers – becomes more aware of environmental challenges, companies that are in a position to demonstrate a circular approach to water use will benefit from improved perception and reduced reputational risk.

Some industries clearly use more water than others, and thus have more scope to push through change and to benefit. Companies involved in food production are obvious candidates. In some regions, too, there is greater impetus for change than in others due to local water conditions. However, the problem is a broad one – everyone uses water and, in an increasingly interdependent and interconnected world, virtually all major businesses are exposed to water scarcity risk at some point in their operations. Investors with deep insight into water use and efficiency thus have the potential to identify hidden risks and opportunities.

Good environmental management is a useful metaphor for a soundly run business. That is true for carbon emissions, and it is also true for water efficiency.

read more about thematic investing

Why the taps won't run dry

Technology holds the key to resolving the world's growing water shortage problems. Thematic investors can make the most of the opportunity.

March 2019

Thematic equities: their use in a diversified portfolio

Investors can make an allocation to thematic equities whichever portfolio construction approach they use.

December 2019

Living beyond our means: Earth Overshoot Day

Humans have consumed a year's worth of natural resources in less than seven months. Our model quantifies the environmental impact of over-consumption.

January 2020

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer. This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.