European property: a rare source of yield

Why real estate remains a fertile hunting ground for long-term investors in search of attractive yields.

Written by

Zsolt Kohalmi

Deputy CEO & Global Head of Real Estate

Forget truffles. Today, the really hard thing to find is a positive real yield. In Europe, the real estate market is one of the few potentially fertile hunting grounds.

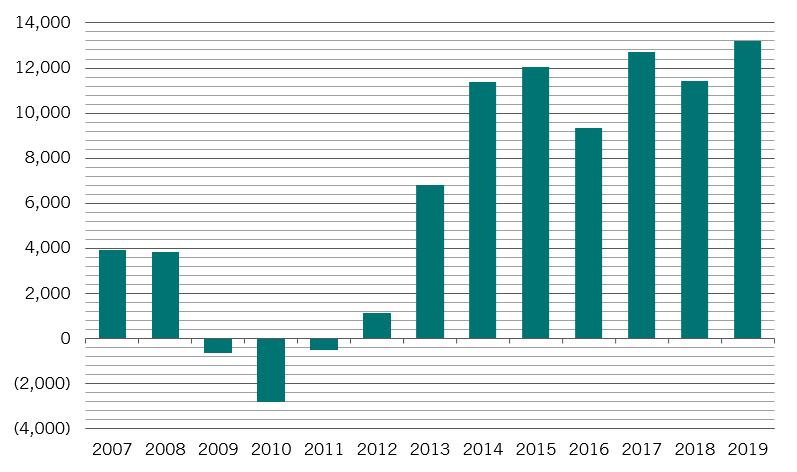

With most major central banks still pumping out stimulus, we expect property’s investment appeal to remain strong, particularly among institutions with longer-term liabilities, such as pension funds.

But popularity comes at a price – the greater the weight of capital, the greater the chance of a bubble forming.

Fig. 1 Booming demand

Global direct property asset flows, USD million

Housing shifts

That is why it is important to understand the structural forces at play in real estate.

For one thing, as a society, we are getting older. Today, one in five people in the European Union is aged 65 or over, up from one in six a decade ago. By 2100, the forecast is that it will be nearly one in three.1

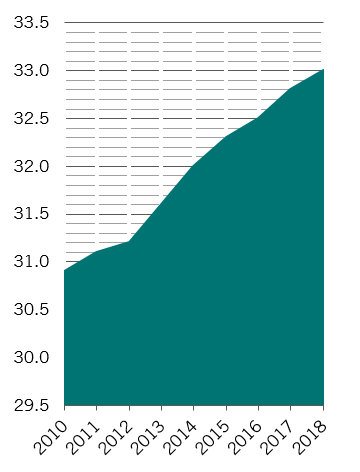

There has been a sharp increase in one person households – in 2015 they surpassed the number of two-person households for the first time since EU records began, according to Eurostat data. Add in the growing problem of affordability , and it becomes clear that for an ever larger number of people, the stereotypical three bedroom, two-storey family home is no longer realistic or desirable.

Demand for housing for the elderly and for smaller homes is on the rise, while houses with communal spaces and other shared services will also become more common. Such trends are already having a profound effect on the dynamics of the real estate market.

When considering investments in residential property, it is also important to understand trends in regulation. Recent legislation passed in Berlin, for example, will freeze rents on around 1.5 million homes over the next five years. Similar measures are being debated in other parts of Europe such as Denmark and the UK.

Fig. 2 Single living

EU-28 one person households, as % of all households

Prospects for the retail real estate sector aren’t especially clear either as it too is facing structural change. Bricks and mortar retailers will likely remain under significant pressure over the coming year – primarily in the UK, but increasingly also in other parts of Europe as online shopping continues to gather pace.

Monsoon Accessorize, Clarks, Ann Summers and River Island are just a few of the UK High Street names who have negotiated reduced rents in 2019. In such an environment, investors need to find a very special situation at a very special price to justify an allocation to retail real estate.

On the flip side, 2020 should see a rise in office rents in a number of countries, driven by high occupancy rates. This is particularly true for gateway cities in Southern Europe.

More broadly, though, at this very late stage in the economic cycle, many regions which look cheap are so for a reason. Lisbon, for example, is often cited as offering better value than other key European cities, but we believe this pricing fairly reflects the liquidity risks.

The UK is another place that is seen as relatively cheap compared to Continental Europe. But, here too, the lower prices reflect greater risks – in this case uncertainty around Brexit, which persists despite the recent election victory by the Conservatives. We believe that trade negotiations could last over the allotted one year that is targeted by the UK government. That’s not to say that there are no attractive opportunities in the UK – there are many, but you need to pick your entry point very carefully.

Consequently in 2020, we are looking for opportunities on a micro basis – considering the merits of each individual building, rather than taking a macro-based bet on a particular location.

read more about investing in real estate and other alternatives

Building a sustainable real estate portfolio

The property industry is the largest emitter of CO2. By making buildings more sustainable, we can help the environment and boost returns.

August 2021

Demystifying alternative investments

Alternatives are prized by investors. They're also in short supply.

March 2018

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer. This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.