The trouble with bonds

Quantitative easing and its effects on fixed income markets are here to stay. Investors ignore that at their peril.

Written by

Andres Sanchez Balcazar

Head of Global Bonds

Quantitative easing has turned the fixed income world upside down. But even though central banks are starting to reverse their emergency policies, QE isn’t going away completely. For investors, this means adopting new rules.

In many ways, bond investors have been guinea pigs over the last 10 years of QE. They were part of a massive experiment, one in which central banks expanded balance sheets to provide liquidity to the market and have ended up owning more than 20 per cent of outstanding global bonds. Throw in tighter regulation, and the effect has been to change the structure of the financial system, leaving banks a significantly less important source of credit.

In 2007, 61 per cent of debt instruments in non-financial firms were bank loans. Last year that figure was 45 per cent.

Bond managers and investors have felt like guinea pigs over the last 10 years of QE.

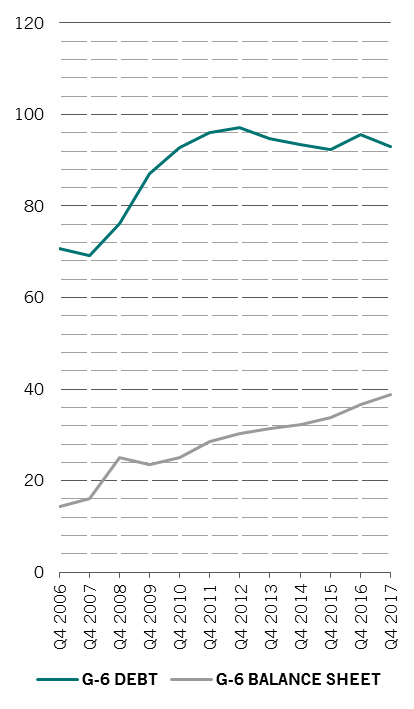

And investors are stuck with QE. Not only is it now an essential part of central bankers’ toolkits for supporting economies when interest rate cuts aren’t likely to be effective, but high government debt levels – they're touching 120 per cent of GDP among G-7 countries – make QE an important backstop for when the markets struggle to absorb fresh bond issuance.

That’s the first and most important of the eight lessons that I believe will help us navigate this new world of QE: QE is here to stay.

Next is that even with QE, the law of diminishing returns holds. Early rounds of stimulus are more effective than later ones. Which is a worry if the next crisis rolls around before central banks have been able to restock sufficient monetary ammunition.

What is more, given QE’s permanent, if variable, role, it’s important for investors to forget about GDP forecasting when talking about the credit cycle. Instead, they should pay attention to what’s happening to central banks’ balance sheets and to their guidance. That's necessary because QE has disconnected the credit cycle from the economic cycle.

It’s also important to retain plenty of flexibility. Investors shouldn’t just rely on market liquidity to satisfy their investment needs. By trying to shore up banks’ balance sheets, central banks reduced liquidity in markets. It means investors have to be prepared to absorb more shocks in future.

Keeping pace with debt

G6 central bank balance sheets and national debt as % of GDP

Fifthly, it pays to think a bit differently by taking a contrarian stance or buying out-of-favour assets. Ugly can be beautiful. Before QE, investors would have done well by investing in the previous year’s best performing sectors. After QE, the strategy that worked best was to buy the 'losers’, assets that are out of favour but still have value.

The sixth lesson is that the yield curve matters. As an investor, the most important decision you’re going to make is duration, or whether to raise or lower your portfolio's sensitivity to changes in interest rates. Before the crisis, curve positioning and duration decisions went pretty much hand in hand. Back then, investors had two basic curve strategy options, depending on how they saw central bank policy unfolding.

If they expected rate cuts, they’d use bull steepeners, under which shorter dated bonds are expected to outperform long-dated ones. Or, if investors envisaged rate rises, they’d set up bear flattener trades, which are designed to benefit from a sell-off in shorter-maturity debt. But since the crisis, other types of yield curve strategies are just as common as a result of central bank bond buying.

Then there’s the matter of changes in the relationship between different fixed income assets. There have been several instances in which assets that usually move in lockstep with one another failed to do so for long periods, and vice versa. In other words, bond investors cannot rely on historic market correlations.

Before the crisis, investors could rest assured that they would achieve a decent amount of diversification by combining safe government bonds and credit in their portfolios. And that the correlation of returns between the two was relatively stable. But after the crisis, this correlation has fluctuated. This is a new risk and it’s not going to go away.

And finally, zombies can be opportunities. Once upon a time, companies that struggled to pay the interest on their debt would fail. But with low interest rates and investors willing to refinance these companies, there has been a fairly gradual increase of the number of such zombie firms globally. Before the crisis, credit managers would do their credit work and make their selections only from among companies that could actually pay their interest costs. But after QE, that probably was not the right answer. You had to pick some of the zombies to outperform.

By the same token, investors need to be aware that as central banks remove liquidity from the system, as they try to reverse QE, credit markets are likely to be most vulnerable. That’s where the rubber hits the road.

Ultimately, investors need to bear in mind that the fixed income markets’ transformation since the financial crisis is here to stay.

We need to face reality and think that maybe the lessons we’ve learned over the last 10 years will also apply over the next 10.

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer. This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.