Asset allocation: complacency setting in

With the number of new coronavirus cases seemingly peaking, and some countries in Asia and the euro zone emerging from their lockdowns, economic conditions are stabilising a little. Stimulus - delivered in generous amounts and at speed - has played a major role in stocks' recent recovery.

Even so, there is bound to be more turbulence ahead - not least the possibility of further waves of the virus. We therefore retain a neutral stance on equities, bonds and cash, and have shifted allocations among regional equity markets and fixed income assets to reflect the risks and opportunities we see emerging over the coming months.

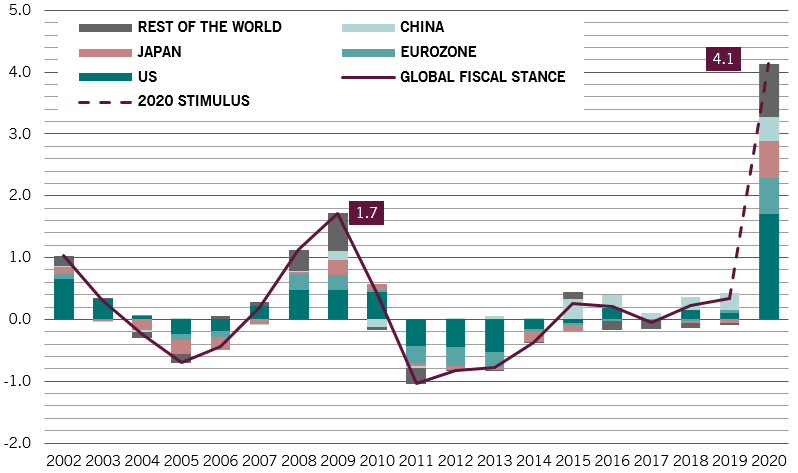

Our business cycle analysis shows the global economy will contract by 3.3 per cent this year, before recovering to grow by nearly 6 per cent in 2021. To limit the contraction, governments and central banks the world over have delivered stimulus on an unprecedented scale. We estimate the global fiscal impulse to be worth around 3.9 per cent of GDP – slightly more than double the 2009 response.

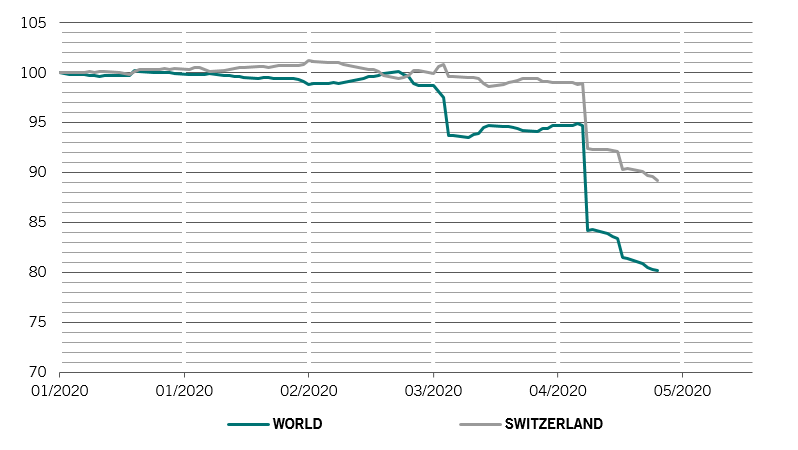

There are some early signs the stimulus is starting to work; we are now taking a slightly more constructive (or at least, less pessimistic) view on the short-term economic prospects for the US, Australia, Switzerland, China and the rest of emerging Asia.

However, in other parts of the world, the stimulus has so far been insufficient. Some areas, such as parts of Latin America, are hampered by their external trade balances and pre-existing problems. Others, like the euro zone, have the scope to do much more when it comes to stimulus measures.

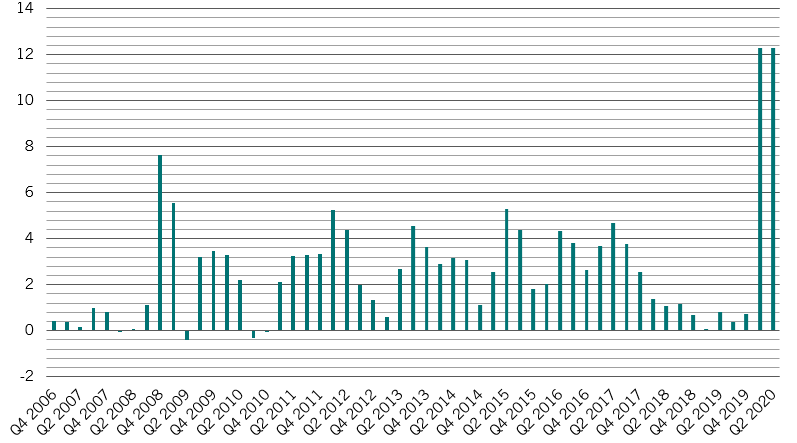

Encouragingly, we are now seeing more from China, which had up until now been a clear laggard in stimulus provision. China’s credit impulse,1 a broad measure of credit and liquidity to the real economy, surged to a decade-high above 9 per cent in March.

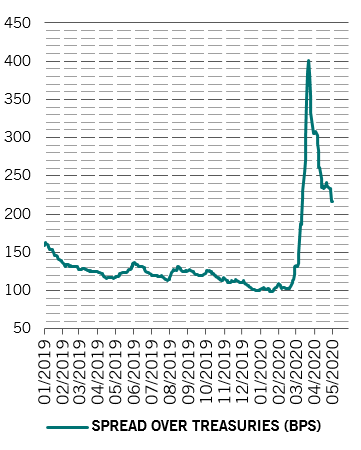

Across the board, valuations for mainststream asset classes are less attractive than they were at the end of March. Developed government bonds in particular are looking very expensive. Our valuation model suggests that equities should outperform bonds by 10-15 per cent over the next 12 months.

This view is supported by our sentiment indicators, which marginally favour riskier asset classes. Investor positioning in equities is far from overstretched and record inflows into money market funds suggest there is plenty of cash to be deployed. Globally, net assets in money market funds have ballooned by USD1 trillion over the past month.