Wanted: a 21st century grid to power a carbon-free future

Renewable energy has become cheap and abundant. Now we need advanced grid infrastructure to use more of it.

Written by

The Thematic Advisory Board

Share this article

Indiana is the second biggest coal-consuming state in the US. It is also among America's top 10 producers. So why has it just decided to ditch coal? The simple answer is cost.

Having mined coal since 1830s, Indiana is ditching fossil fuel in favour of solar and wind because, says its major utility, the move will save consumers billions of dollars.

Indiana is not alone. In other US states, and in countries around the world, the cost of producing renewable electricity has fallen sharply, enabling solar and wind power to dethrone fossil fuels.1

That’s encouraging news as cities and countries battle to cut planet-warming carbon emissions.

However, cheap and clean energy is of no use unless it’s delivered to where it’s needed, day and night without fail. This is where the power grid comes into play.

Power grids match the amount of electricity being generated with the load, or the amount being consumed. But today’s grid infrastructure, already under stress from extreme weather events such as hurricanes or wildfires, is ill-equipped to deal with the rush of renewables.

The intermittent nature of solar or wind means these power sources are also ill-suited for large-scale energy distribution.

This is why the world needs to develop advanced transmission infrastructure.

To investigate possible solutions, members of the Pictet-Clean Energy Advisory Board (AB) and the strategy's investment team recently visited the National Renewable Energy Laboratory (NREL) in Denver and the Electric Power Research Institute in Palo Alto, two organisations renowned for their pioneering renewables research.

There, our AB members saw for themselves advances in renewable energy technology, and were provided with fresh insights on infrastructure needs around the adoption of electric vehicles and the challenges and opportunities involved in integrating a growing fraction of renewables into the power grid.

Breaking the grid-lock

The current grid is based on a one-way system in which electricity flows from power plants to homes and businesses. It relies on alternating current (AC) for both long distance transmission and local distribution.

AC has changed little since its development in the late 19th century, when it emerged victorious from the War of the Currents to become the standard for electricity grids worldwide.

Using a transformer, AC can be easily converted to different voltages. But its major shortcoming is that it loses power in transit. For a given voltage, an AC system has roughly twice the loss of a DC system, which can transmit energy more cheaply and efficiently over very long distances.

AC’s constraints become more obvious when it comes to distributing renewable energy because solar, wind and hydroelectric power is usually generated far away from where the energy is used.

Because of this, AC grids’ renewable capacity is limited to just 15 per cent of their total power mix, our AB members estimate.

Raising the percentage could destabilise the grid and lead to regular blackouts.

This is where DC could make a difference.

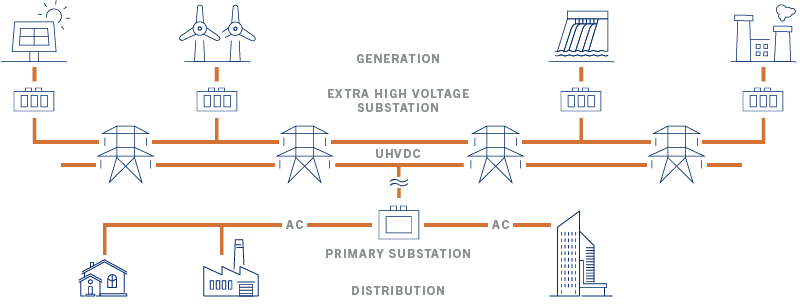

power play

How UHVDC will accelerate integration of renewable energy in grid

Source: Pictet Asset Management, Tepco, CEERT

In its modern form, ultra high-voltage direct current (UHVDC), is even more powerful, capable of using voltages as high as 1,100kV, compared with conventional DC’s 1.5kV.

UHVDC can also link unconnected AC transmission systems across different areas (see chart). This means a UHVDC-based macro grid lets operators tap into different clean energy sources hundreds or thousands of miles away throughout the day, and to effectively switch between sources depending on demand and weather.

Almost a decade after becoming the first country to adopt UHVDC, China debuted the world’s longest and most-powerful UHVDC line in early 2019. The new link stretches over 2,000 miles – more than the distance between London and Moscow. It delivers 66 billion kilowatt/hour of electricity from the country’s far northwest – home to abundant solar and wind power – to the heavily populated east, meeting demand of 50 million households.

HVDC is also gaining traction elsewhere, Europe is also planning to upgrade the grid infrastructure with an ambitious aim of turning itself into a "copper plate", in which a strong pan-European transmission network will make it easier to distribute power beyond borders, from sunny or windy regions to rainy and cloudy areas.

Germany, for example, is developing a HVDC grid link to transport renewable energy from the windy north to high-consumption regions of the south.

The 800km Sudlink project should help Germany achieve its national target of generating 65 per cent of its energy needs from renewable sources by 2030, compared with the current 38 per cent.

Critics say UHVDC's high upfront costs are a significant obstacle to its adoption.

Yet the long run benefits could be huge.

According to our AB members, the infrastructure projects in Europe usually pay for themselves in three to five years thanks to efficiency savings.

The grid infrastructure projects in Europe usually pay for themselves in three to five years thanks to efficiency savings.

Wyoming's wind

Crucially, the US, the world’s biggest energy consumer, has also become a DC convert.

The USD3 billion TransWest Express Project aims to install a UHVDC transmission line to bring wind power from Wyoming 730 miles to California, which is hungry for clean energy to meet its carbon reduction targets.

NREL estimates that the line will save USD1 billion per year for Californian consumers.2

Research by the Earth System Research Laboratory found that power grids like these that make better use of abundant wind power potential could cut carbon emissions by as much as 80 per cent compared with 1990 levels.3

Investing in the world’s transition to clean energy system

Thanks to new and innovative grid technologies, renewable energy has the potential to pick up speed. This represents a bright future for investors, who should benefit from a long-term transition to a low-carbon world.

The Pictet-Clean Energy portfolio invests in companies that are playing an important role in this clean energy transition.

The high voltage DC industry presents a wealth of investment opportunities as the market is poised to grow at a compound annual rate of almost 9 per cent to reach USD16.3 billion by 2026.4

Technologies that support the HVDC system should also experience growth. Take for an instance industrial semiconductors, which are critical in running the electric grid.

Silicon chips are needed to convert power between different AC and DC voltages and in different frequencies, which helps minimise power loss and maintain the stable flow of electricity.

Demand for industrial semiconductor is expected to double between 2016 to 2022 to USD81 billion, registering 10 percent-plus growth every year.5

Each thematic strategy benefits from a dedicated advisory board made up of eminent scientists, business leaders and academics. This enables us to test our views against experts in their respective fields, providing us with a deeper understanding of the regulatory environment and the trends supporting the theme.

Share this article

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user experience and to collect statistical data. You may refuse to accept cookies or change your settings by clicking the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.