Select your investor profile:

This content is only for the selected type of investor.

Institutional investors and consultants or Investisseurs particuliers?

Demystifying Bitcoin

As the price of Bitcoin booms, investors are taking an ever more active interest in it. But how close is the cryptocurrency to becoming a genuine investment asset?

Written by

Luca Paolini

Chief Strategist

It’s no coincidence that Bitcoin is back in the headlines just as concerns about inflation start to rumble.

That’s because cryptocurrencies, among which Bitcoin has the highest profile, have become barometers of sentiment about aggressive central bank monetary policy and financial repression. For the past decade, central banks have propped up their economies in the wake of the global financial crisis by driving interest rates and bond yields down below the rate of inflation, in effect forcing negative inflation-adjusted returns onto investors. That became even more pronounced as policymakers responded in even more emphatic fashion to the economic crisis caused by the Covid pandemic.

At the same time, distrust of government surveillance is growing as ever more of our lives move online. An anonymous digital currency becomes attractive.

But there’s a lot that can potentially go wrong for Bitcoin. So much so, that it would be hard to justify the digital currency as anything other than among the most speculative investments.

Crypto appeal

Bitcoin has been on a tear lately amid concerns that central banks have taken quantitative easing and other stimulus measures too far. The growing fear is that monetary authorities are gradually monetising government deficits, which is to say that they’re permanently funding government overspending as a means of underpinning their economies in the wake of the Covid pandemic.

That’s an issue, because historically debt monetisation has been a precursor to uncontrolled inflation.

But even those who don’t worry about this sort of extreme outcome have reasons to like Bitcoin. Just the fact that central banks are depressing government bond yields to below even today’s low rate of inflation – known as financial repression – has reduced the opportunity cost of holding assets that don’t generate income, assets like Bitcoin.

More recently the cryptocurrency has had a modest positive correlation with equities and gold and a negative correlation with US Treasuries and the dollar.

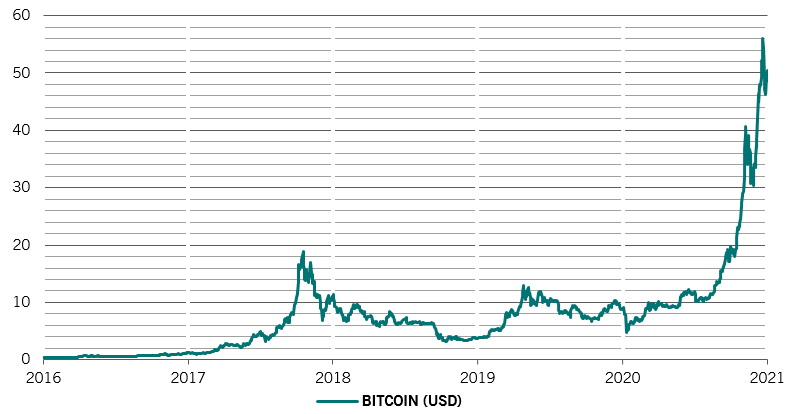

Bitboom

Bitcoin price (USD, '000)

Transaction detraction

Bitcoin may be making inroads into normal commerce, but it has a long way to go before it becomes a substitute for currencies. It is still cumbersome to use, it isn’t widely accepted and stories are legion of people forgetting their passwords or suffering hardware problems so that they no longer have access to their Bitcoin wallets – some 20 per cent of the cryptocurrency is said to be in this limbo.1

Furthermore, blockchain, the database used to record Bitcoin transaction, is limited in how many transactions it can execute – estimated at between three and nine per second. Factor in high transactions costs and Bitcoin’s attractions fade relative to more liquid assets.

US Treasury Secretary Janet Yellen recently warned that Bitcoin is extremely inefficient for conducting transactions, and at the same time warning that it is a highly speculative asset.

Its recent price moves have raised doubts over Bitcoin’s potential as an alternative to safe assets or as a store of value. On Feb 21 it peaked at USD58,000. The following day it had dropped back down to USD47,000 – where it was a week earlier. Nor is this sort of volatility new – Bitcoin’s dollar price has always swung wildly.

One key problem for investors is that Bitcoin is impossible to value. It’s not a claim on any underlying asset – it is the asset. It generates no income. And unlike, say, gold, it has no long history during which it’s been able to develop a widely held reputation as an alternative store of value. It is thinly traded, frequently associated with illicit transactions and subject to wild swings of sentiment.

And it subject to considerable risks.

Attracting the wrong sort of attention

The more Bitcoin attracts speculative interest from amateur investors, the more regulators that exist to protect them will take note. At its recent peak, the total value of all Bitcoins in existence was estimated to have reached USD1 trillion. Although not yet seen as a potential systemic risk for the financial system, that’s a big enough market to draw regulatory scrutiny. That’s aside from the fact that legal authorities are already taking an interest in its role in the black economy. Meanwhile, Bitcoin mining is highly concentrated, mainly among Chinese operators.

Although Bitcoin’s big appeal is its anonymity, there’s the possibility that existing authorities could chip away at that if they were to provide something similar. Yellen recently noted that while there are a great many issues that would have to be resolved before digital dollars could be created, the venture “is absolutely worth looking at.” She added that a “digital dollar could result in faster, safer and cheaper payments.” A digital dollar that also gave its users anonymity would potentially be attractive – dependent on the sorts of guarantees the government would be willing to provide.

The more Bitcoin attracts speculative interest from amateur investors, the more regulators that exist to protect them will take note.

Bitcoin’s biggest remaining draw would then be its limited supply – there is a built-in supply limit of 21 million units. And it takes ever more computing power to mine each additional Bitcoin, making it immune to the sort of debasement of traditional currencies that many of its supporters fear.

But even here, Bitcoin faces threats. Bitcoin mining already consumes more electricity than Argentina, according to one estimate.2 The Iranian government has blamed local blackouts on power hungry Bitcoin mining operations.3 Which gives governments just another reason to take aggressive action against Bitcoin.

The cryptocurrency routinely captures headlines and has substantial and vocal support on internet chatrooms. But the risks are heavily stacked against it ever becoming a serious and substantial investment vehicle, much less a replacement for the dollar.

related articles

Demystifying equity factors

Factor investing has become increasingly popular. Here's what it is and how it works.

September 2019

Demystifying sustainable investing

There's much more to responsible investing than avoiding "sin" stocks. And it can make financial sense too.

April 2019

Demystifying long/short equity strategies

When markets encounter turbulence, it is tempting to eliminate stocks from your portfolio. But, for many investors, allocating capital to long/short equities might be a better option.

March 2020

Important legal information

The Pre-Contractual Templates (PCT) when applicable, the Key Information Document (KID), as well as the Prospectus must be read before any decision to invest. The Prospectus (in English and in French), the PCT when applicable, the KID (in French and in Dutch), as well as the latest annual and semi-annual reports (in English and French) are available free of charge at our financial Belgian agent CACEIS Belgium S.A., 86C /b320, Avenue du Port, 1000 Bruxelles or at the management company, Pictet Asset Management (Europe) SA, 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, as well as in digital format at www.assetmanagement.pictet.

The summary of investors rights is available here and in French and in Dutch at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The NAV are available at www.beama.be.

Claims and Mediation Service: For any claim you can contact Pictet Asset Management (Europe) S.A., Compliance Department, 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg or the Consumer Mediation Service (Service de Médiation pour le Consommateur), North Gate II, Boulevard du Roi Albert II 8 in 1000 Bruxelles or at www.mediationconsommateur.be. The Mediation Service may suggest solutions for the settlement of the dispute. In the absence of agreement on the proposed solutions, each party may bring proceedings before the competent courts.

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. Pictet Asset Management (Europe) S.A. has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future.

Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

This marketing material is not intended to be a substitute for the fund’s full documentation or any information which investors should obtain from their financial intermediaries acting in relation to their investment in the fund or funds mentioned in this document.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.