The coronavirus pandemic threatens to accelerate de-globalisation. But there are reasons to hope it won't.

Written by

Patrick Zweifel

Chief Economist

Share this article

The coronavirus pandemic has cast a dark shadow over global trade. In the short term, lockdowns across the world have caused an unprecedented collapse in cross-border commerce, a rational response, guided by public health considerations. But the fear is that these negative effects will persist long after the crisis has passed. This, though, shouldn’t be a foregone conclusion.

There are good reasons to believe that while the web of international economic relations is likely to change, perhaps significantly, trade won’t be damaged catastrophically. Instead, some of the flows of physical goods will be replaced by digital services. Meanwhile, supply chains are likely to broaden and become more regional.

Before the pandemic

The main fear is that a reversal in globalisation that started with the global financial crisis in 2008 (GFC) will be exacerbated by the coronavirus pandemic. Brexit, President Donald Trump’s trade wars, strains within Europe over migration, rising populism challenging elites, onslaughts against multilateral institutions like the World Trade Organisation are all routinely cited as signs of the shift against trade and open borders.

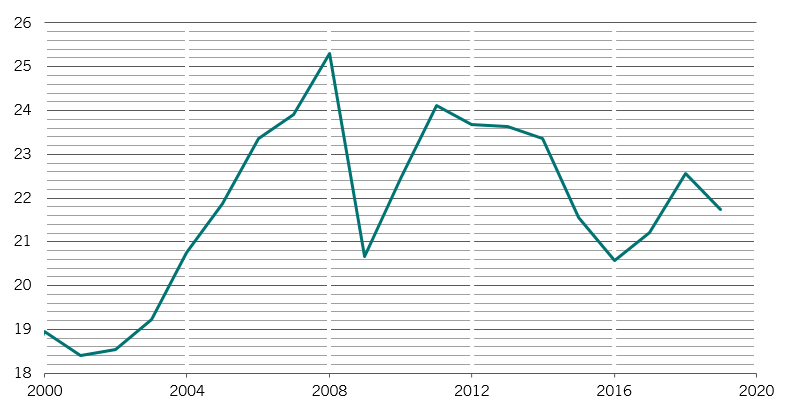

Fig. 1 - Global trade slips...

Global trade as a % of global GDP

Source: Pictet Asset Management, IMF, CEIC. Data covering period 31.12.1999-20.04.2020

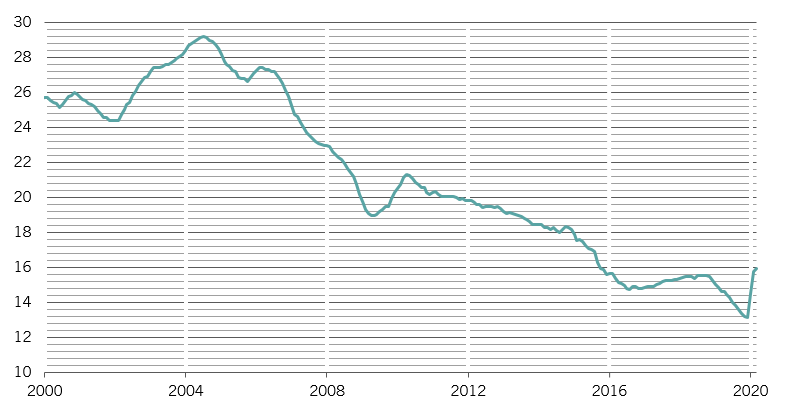

Globalisation peaked with the GFC. In 2008, word trade of goods had hit a high of 25.3 per cent of global GDP. By 2019, that proportion had dropped to 21.7 per cent. To be sure, a rise in protectionism was a contributing factor – in that decade, restrictive trade measures were imposed on USD1.5 trillion of imports, or 7.5 per cent of global trade in 2018. But there were also two other factors that have little to do with anti-globalisation movements. First, weak growth in post-GFC investment held back demand for investment-related imports, the most trade-intensive component of domestic demand. And second, as emerging economies, led by China, matured, they became less of a waystation in the global supply chain – most high-end manufactured goods frequently cross and re-cross borders on the way to being finished products. For example, in 2004 China’s imports for re-export were worth 29 per cent of total exports. By 2019 that proportion had dropped to 13.2 per cent.

The corona conundrum

Undoubtedly, international integration was a major factor in the speed at which this pandemic spread. The virus originated in a central Chinese marketplace, probably sometime in the final quarter of 2019. By the end of the first quarter of 2020, all the world’s leading economies were in some degree of lockdown. That's no surprise in an era of mass tourism: today, thousands of flights connect the most disparate parts of the world and huge cities double up as major international transport hubs.

Governments coming out of this crisis will undoubtedly think twice about the benefits of global integration and interdependence. Barriers to travel are likely to prove sticky, much as security measures have in the wake of 9/11.

Fig. 2 - ...as China's economy matures

Chinese imports for re-export as % of total exports

Source: Pictet Asset Management, IMF, CEIC. Data as at 20.04.2020

China could be the target of new restrictions – populist politicians elsewhere have argued that it needs to be “punished” for being the source of the infection.

Meanwhile, global supply chains have been heavily disrupted by the lockdown as factories have been shut down for the duration. Companies could well respond by taking measures to reduce their vulnerabilities.

A new globalisation

But while there are risks to globalisation in the post-coronavirus world, the likelihood is that international trade takes on new forms rather than being undermined.

There could well be less trade in physical goods and less mobility of people. But digital globalisation will undoubtedly become more important. The global lockdown has shown both companies and governments how much can be achieved through the internet – whether it’s the effectiveness of remote working and the practicality of online services. Video-conferencing can be much more efficient and time-saving than in-person meetings. E-learning can be effective, potentially opening up high quality education to many more students.

Although companies may be inclined to bring some production home, the principle of comparative advantage will still hold. It will always be more economically efficient to source some goods and materials from other countries. Instead, companies could shift to being less reliant on single sources, making their supply networks more resilient by diversifying their supplier networks and building in some redundancy. That might increase the cost of production somewhat, but companies could well see this as insurance against broken supply chains.

Shortening supply chains could make trade more regional – as has happened in Asia over the past three decades, including since the GFC. Intra-Asian trade represented 28 per cent of total Asian exports, rising to 42 per cent in 2008 and 46 per cent in 2018. Where this raises labour costs, companies can compensate by moving towards greater automation.

As for China’s role in the world, its alacrity in providing medical aid and emergency supplies to many countries will surely have won it friends around the world, showing the necessity of multilateral cooperation, even at a time when, in other respects, countries have been closing themselves off. This pandemic has fostered unparalleled international collaboration in medical research. China has been pivotal to this effort, having been the first to suffer the virus and given the scale of its scientific community and facilities.

Yes, trade relations always come with risks. Yet the benefits of globally interconnected economies mustn’t be understated – they are far greater than the costs. Recent decades of rising global trade, prompted by falling barriers like tariffs, have lifted hundreds of millions of people out of poverty – not just in Asia, but across the world. We mustn’t allow the pandemic to undo all that’s been achieved.

Patrick Zweifel joined Pictet in 1997. He is Chief Economist at Pictet Asset Management, having assumed the position in 2009. Before that, he was head of the “Macro Research Team” at Pictet Private Wealth Management, where he was responsible for emerging markets and Japan, and for the development of quantitative models on major asset classes. Before joining Pictet he was a research assistant in econometrics and monetary theory and worked on international research projects for the World Bank and the European Union. He holds a PhD in Econometrics from the University of Lausanne.

Share this article

Important legal information

The Pre-Contractual Templates (PCT) when applicable, the Key Information Document (KID), as well as the Prospectus must be read before any decision to invest. The Prospectus (in English and in French), the PCT when applicable, the KID (in French and in Dutch), as well as the latest annual and semi-annual reports (in English and French) are available free of charge at our financial Belgian agent CACEIS Belgium S.A., 86C /b320, Avenue du Port, 1000 Bruxelles or at the management company, Pictet Asset Management (Europe) SA, 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, as well as in digital format at www.assetmanagement.pictet.

The summary of investors rights is available here and in French and in Dutch at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

Claims and Mediation Service: For any claim you can contact Pictet Asset Management (Europe) S.A., Compliance Department, 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg or the Consumer Mediation Service (Service de Médiation pour le Consommateur), North Gate II, Boulevard du Roi Albert II 8 in 1000 Bruxelles or at www.mediationconsommateur.be. The Mediation Service may suggest solutions for the settlement of the dispute. In the absence of agreement on the proposed solutions, each party may bring proceedings before the competent courts.

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. Pictet Asset Management (Europe) S.A. has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future.

Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

This marketing material is not intended to be a substitute for the fund’s full documentation or any information which investors should obtain from their financial intermediaries acting in relation to their investment in the fund or funds mentioned in this document.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user navigation and to collect statistical data. To refuse the use of cookies, change your settings or for more information, please click on the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.