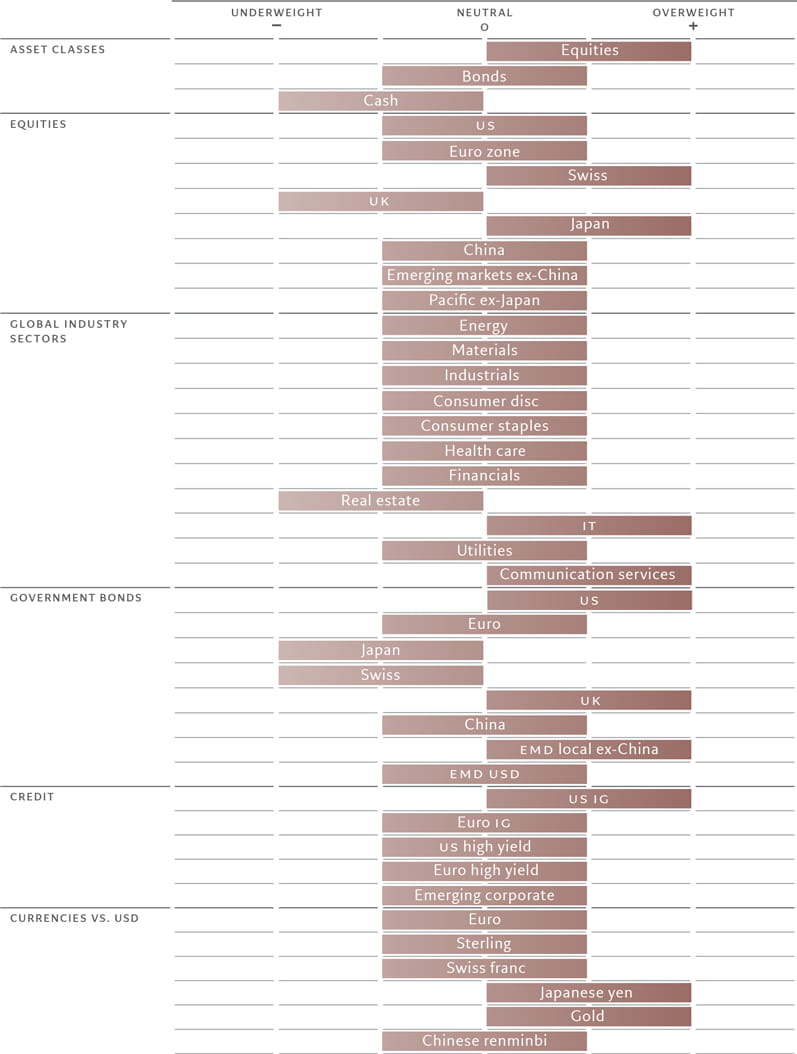

Asset allocation: sticking with equities

While global economic and liquidity conditions are far from rosy, we see pockets of improvement that are supportive for risky assets.

The US economy remains resilient, while China is showing signs of a recovery. Also, most major central banks are likely to begin cutting interest rates in a matter of months and banks are willing to lend more. Partly in response, we have increased our forecast for global corporate earnings this year to 8.1 per cent from the previous 7.2 per cent – largely in line with the consensus estimate.

We recognise that equities are getting expensive, especially in markets like the US and Japan. Yet we don’t believe they are forming a bubble.

Considering all this, the balance of risks points towards a continuation of the equity market rally. We therefore remain overweight equities, neutral bonds and underweight cash.

Our business cycle analysis shows that, in the US, domestic demand, supported by tight labour market conditions, remains the engine of growth.

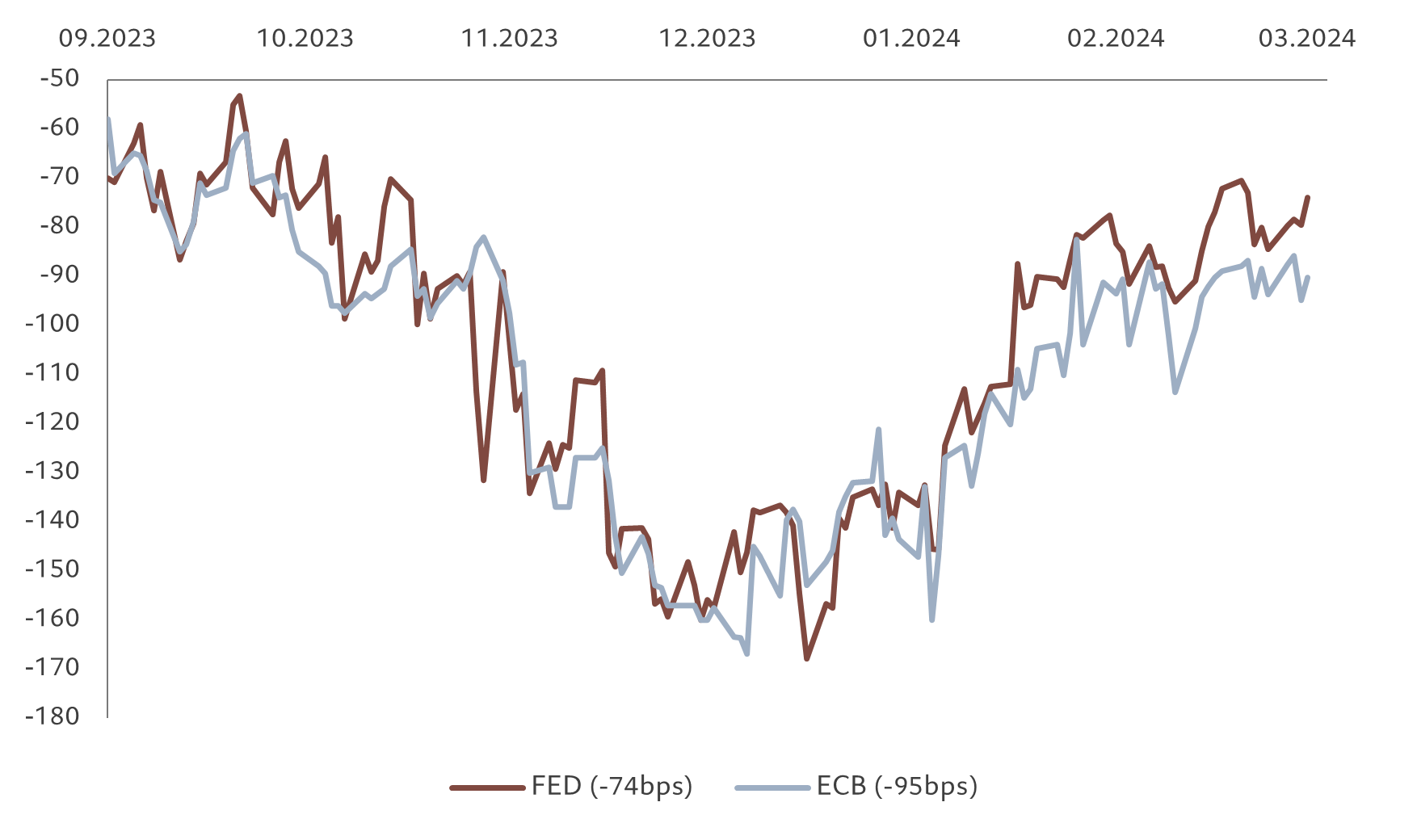

Although economic conditions are healthy, we still expect the US Federal Reserve to begin cutting interest rates as early as June for a total of 2-3 times, even if sticky inflation means the scale of easing is uncertain. We expect Fed funds rate to end the year at 4.50-4.75 per cent.

Other major economies are in a less healthy state.

Japan is flirting with recession with industrial production, retail sales and housing starts all softening. However, domestic demand is resilient and jobs markets remain tight, which support what the Bank of Japan considers as a virtuous cycle of rising income and higher spending.

In a well telegraphed but historic move, the BOJ ended eight years of negative interest rates and other unorthodox policy and raised interest rates for the first time in 17 years. We expect the central bank to lift the benchmark rate by 20-25 basis points this year, but above-target inflation opens the door to further tightening.

That said, interest rate hikes are unlikely to dent the attractiveness of Japanese assets this year as monetary policy still remains accommodative and domestic investors are awash with unattractive cash which stand ready to be deployed.

Growth in the euro zone, while currently weak, is likely to move gradually above potential in the second half of this year as inflationary pressures ease. This should allow the European Central Bank to cut interest rates in the coming months.

China’s economy is showing early signs of bottoming out. Data released so far this year is consistent with a first-quarter GDP reading of around 7 per cent points – a strong start towards our full-year growth forecast of 4.9 per cent. A composite purchasing managers’ survey shows manufacturing and services activity is growing again.

That said, we feel it is too early to be positive about China’s economic prospects after many false starts in the past. What is more, China’s central bank is unlikely to accelerate the pace and scale of monetary policy easing given its focus on deleveraging and maintaining currency stability.

Outside China, emerging economies are growing strongly. We expect the growth gap between developing and industrialised markets to widen further to a two-year high of nearly 3 percentage points on a 12-month moving average basis, which is above the long-term average of 2.1 per cent and points to stronger local currencies in the medium term.

Our analysis of liquidity conditions doesn’t give a particularly bullish or bearish signal for riskier asset classes, although the reading is likely to improve for equities and riskier bonds in the near term as developed central banks join emerging counterparts in easing monetary policy.

Another potential boost to liquidity could come via US and euro zone commercial banks, which are increasingly willing and able to lend, which bodes well for liquidity generated from the private sector.

Our valuations readings show equities are becoming less attractive relative to bonds. The equity risk premium – which measures an excess return investors receive in equities over a risk-free rate – has fallen to 3.5 per cent, compared with a historical average of 4-4.5 per cent. However, global corporate earnings are expected to remain strong, with a consensus forecast projecting “no landing” – or no earnings recession in the next three years.

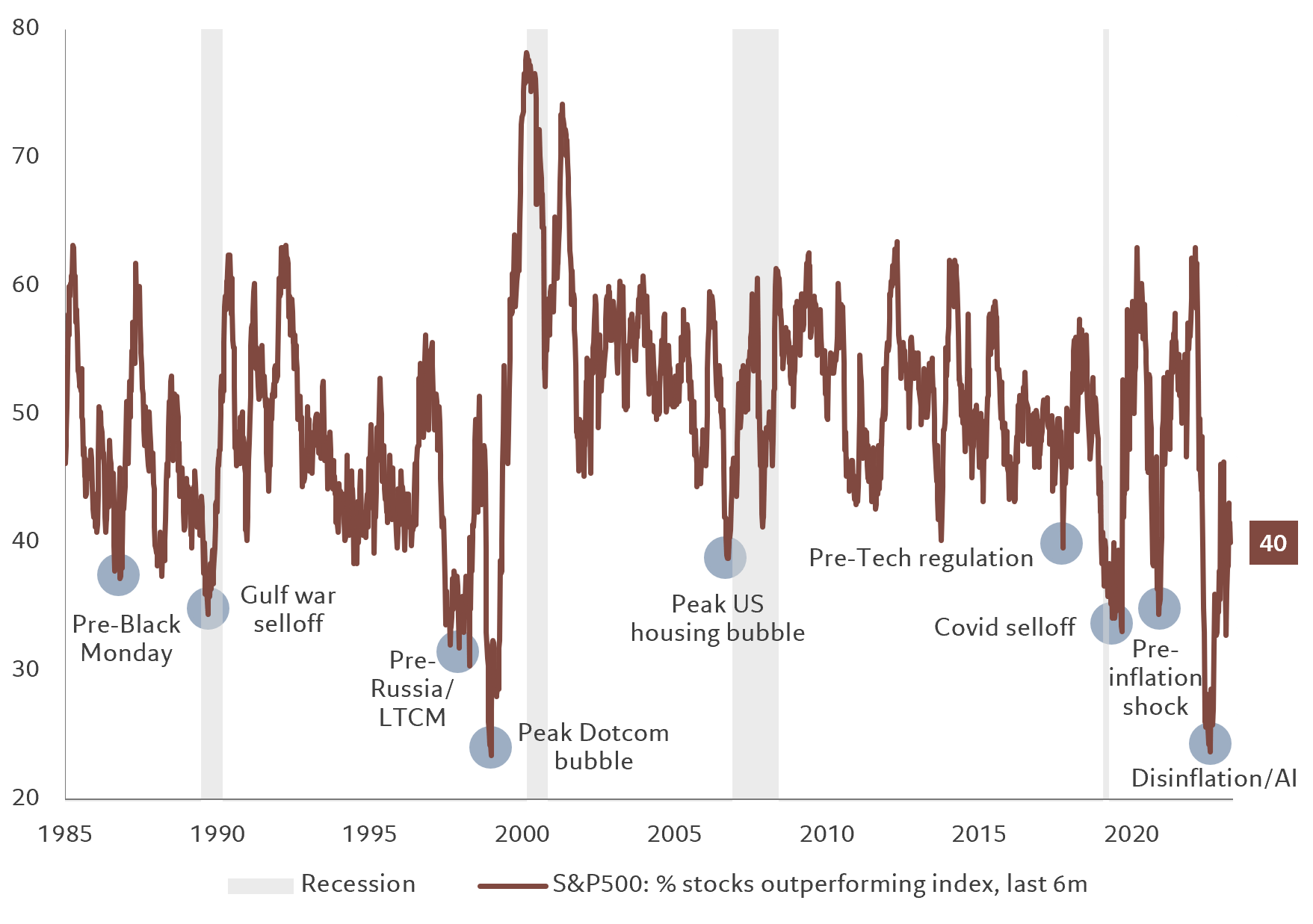

What is more, we don’t think equities have reached what might generally be considered to be bubble territory yet. Our model shows the bubble territory of the S&P 500 index begins at around 6,200 – some 15 per cent above the current level -- with 12-month price earnings of 25 times.

US Treasuries are fairly valued; the benchmark 10-year yield of some 4.3 per cent is more or less in line with what our fair value pricing model shows.

Technical indicators support our overall asset allocation stance. Equities attracted a strong USD52 billion of inflows in the past four weeks, with US equity products being among the most favoured. This trend looks likely to hold firm. Money market funds, in contrast, just registered the largest weekly outflows in five months.