EM Monitor – the opportunity from dispersion in emerging market debt

March 2021

Marketing Material

EM: this time it's different(iation)

Digging under the surface of emerging market fixed income reveals multi-layered dispersion, both across countries and capital structure.

Written by

Ketan Gada

Head of Total Return EM Fixed Income

Gareth Payne

Head of Credit & Alternative Fixed Income Client Portfolio Management

Share this article

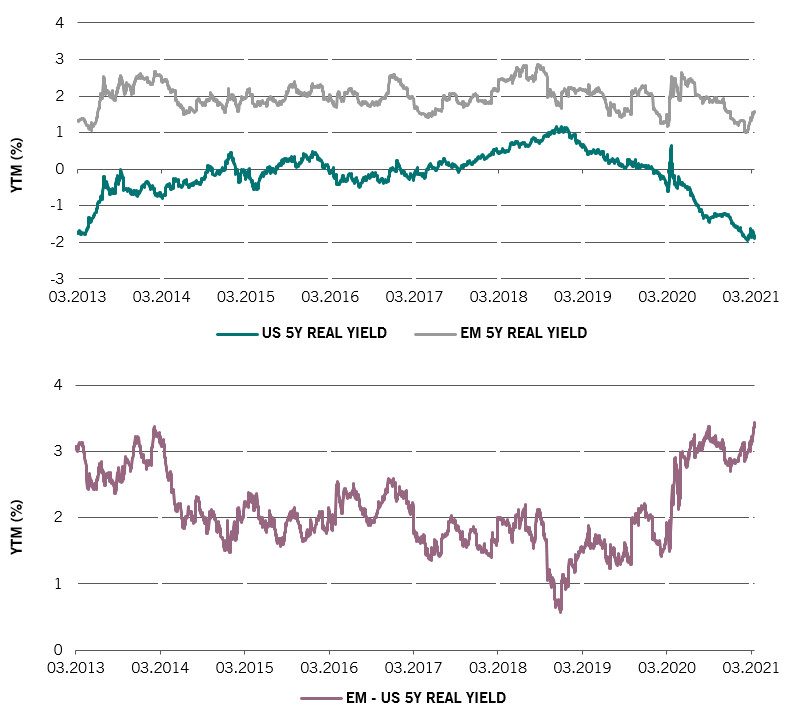

Real yield advantage

In an income-starved world emerging market local currency debt offers an attractive inflation-adjusted yield (real yield) pick-up over developed markets, as the charts show below. This is despite EM real yields being some way off their absolute highs.

Pick me up...

Fig.1: EM vs DM real yield evolution and differential (bottom chart)

Source: Bloomberg, JP Morgan. March 2021. The EM real yield is calculated by taking equal weighted country yield of countries in JP Morgan GBI-EM Global diversified index minus the latest CPI print for: Poland, Hungary, Romania, Russia, Turkey, South Africa, Mexico, Brazil, Colombia, Chile, Peru, Indonesia, Philippines, Malaysia, Thailand and using the Bloomberg 5Y generic bond yield - latest CPI for China

The long and short of it...

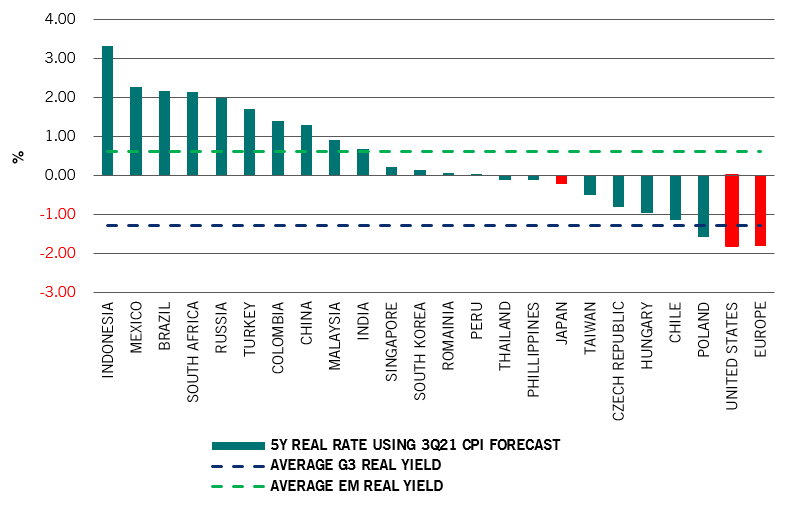

The asset class has more dimensions to offer however. As a long-short manager we are continually looking to exploit the dispersion within emerging market fixed income – see Figure 2 for the wide divergence of real yields across countries.

EM is not a homogeneous asset class and taking a purely top-down view risks overlooking many critical differences below the surface. What is required is individual country and asset selection. We believe a strategy that uses long and short positions is particularly well suited to generate excess returns from such dispersion.

Real yield dispersion

Fig. 2: EM and DM real yields

Source: Bloomberg, JP Morgan. March 2021.

Differentiation goes deeper

Dispersion in real yields is just one part of the puzzle when looking to unearth alpha in emerging markets. Also important are GDP growth dynamics, fiscal and monetary impulses, and technical factors such as momentum, flows and local policy.

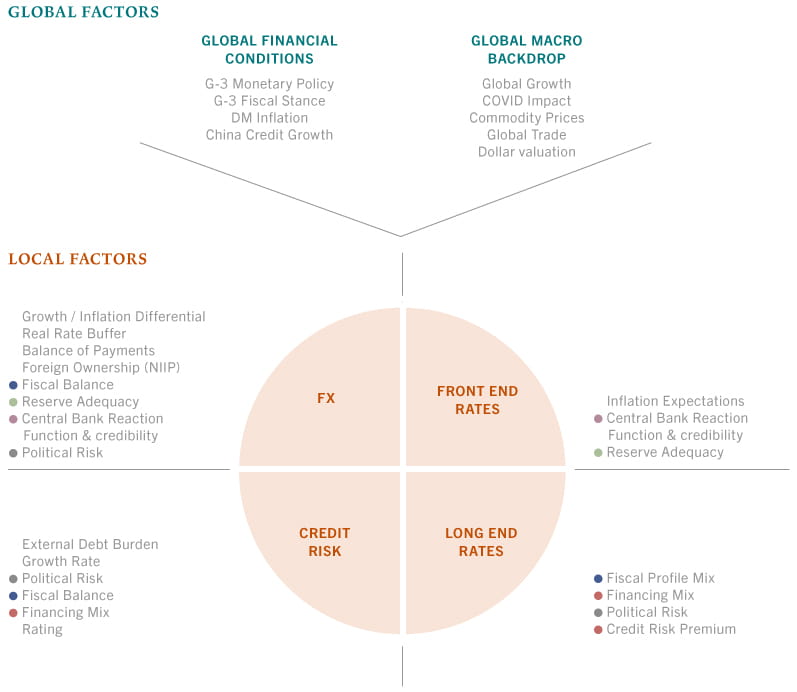

The intersection of global and local factors in EM fixed income investing

Fig. 3: Our framework for blending top-down and bottom-up factors

Source: Pictet Asset Management

Figure 3 is our framework for analysing the EM opportunity-set. First comes an assessment of global financial conditions and the macroeconomic backdrop. Next we unpeel the layers of how these impact each emerging market from the bottom-up. Impacts are not uniform given the idiosyncrasies of each country. An added dimension is asset reaction function, as macroeconomic factors may have differentiated effects on the different parts of the EM capital structure. For example on rate curves, sovereign credit or the currency of a country.

The aim is to decide for any given market and specific debt instrument if the potential return adequately compensates us for the risk profile of local rates, FX volatility, inflation and domestic institutional risks. The challenge is using the correct lens depending on the country in question and, critically, assessing time horizons.

Dispersion in a post-Covid world

We think the value of our long-short approach has never been more relevant than today. Especially as we look at the massive fiscal response to Covid-19 and assess each country’s ability or willingness, to tighten the purse strings and the pace at which that may happen.

Some of the highest yielding countries, such as Brazil, South Africa and Turkey are at a crossroads. Their loose policies in 2020 will make the year ahead very challenging as they look to re-open and rebalance their economies. The fiscal deterioration has impacted their external credit worthiness, causing local rates markets to begin to price in a higher credit risk premium.

Some of the highest yielding countries are at a crossroads, but we don't expect a systemic crisis for emerging markets.

But we don't expect a systemic crisis for emerging markets. The backdrop of accommodative global central bank policy and huge fiscal provision, plus a better starting point for many of the EM countries, should ensure that.

How each emerging country emerges from today’s unprecedented environment will vary. Widely disparate economic and fiscal metrics, fundamentals, socio-economic backdrops and political willingness to adapt, will all play a part. We believe EM is a multi-layered landscape that lends itself to a long-short approach, and, for nimble investors with strong analytical skills, offers excellent opportunities to generate uncorrelated alpha.

About

Ketan Gada

Ketan Gada joined Pictet Asset Management in 2016 as a Senior Investment Manager in the Total Return Emerging Markets team.

Before joining Pictet, Ketan was a Partner and Senior Portfolio Manager at Quadra Capital Partners, where he managed a Emerging Markets Long/Short fund. Prior to Quadra, he spent ten years at Blackrock and Barclays Global Investors as a Managing Director running Emerging Markets strategies within the hedge fund Fixed Income Global Alpha.

Ketan began his career in 1998 at Cargill managing proprietary Emerging Markets risk.

Ketan holds a Master of Business in Finance and Strategic Management from the University of Minnesota and a BA in Finance from the University of St. Thomas.

About

Gareth Payne

Gareth Payne joined Pictet Asset Management in February 2019 and is Head of Credit & Alternative Fixed Income Client Portfolio Managers.

Before joining Pictet, Gareth was the Client Portfolio Manager for Man GLG’s Credit and Convertibles business with responsibility across both alternative and long-only strategies. Prior to that Gareth worked in a number of business development roles at Man’s multi-manager hedge fund unit, FRM. He began his career in 2007 at Lehman Brothers in London.

Gareth holds a Masters and BA from the University of Cambridge

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user navigation and to collect statistical data. To refuse the use of cookies, change your settings or for more information, please click on the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.