INFLATION RISKS - ABSOLUTE RETURN FIXED INCOME APPROACH

May 2021

Marketing Material

Investing whatever the (inflation) weather

Concerns about an overheating economy are growing and investors are scrambling to get the clearest view possible on inflation. We believe a better approach is to position for the risks. Here’s how.

Written by

Andres Sanchez Balcazar

Head of Global Bonds

Share this article

Let’s talk about inflation. The steady removal of lockdown restrictions, tremendous amounts of public spending and loose central bank policies are creating a lot of anxiety about a possible overheating of the economy. There are grounds for concern – inflation has a major bearing on asset prices. Still it is – and has always been – extremely tough to gauge; many economists have made big forecasting errors in trying to predict its path.

Which is why we look at inflation using a risk management approach. Rather than trying to predict exactly how inflation might evolve in the next few years, we focus on where the greatest risks lie and choose the most effective way to hedge against them. Actively trying to protect against tail risks – scenarios that lie beyond the regular realm of expectations – is an integral part of our process.

Most of the anxiety about inflation stems from a surge in government spending – public expenditure in most developed economies is now running above 4 per cent of GDP. Only a couple of years ago, 2 per cent was thought to be excessive. And there is more largesse to come, particularly in the US. Traditional economic theory, as espoused by John Maynard Keynes, suggests that stimulus on such a scale would transform what is currently a very large output gap1 into a very large output surplus, giving rise to unusually high levels of inflation.

However, this time the trigger for the stimulus delivered was an extremely deep and violent shock to growth, especially in the services sector. True, the size of the fiscal package is huge but the size of the shock to economic growth last year was unprecedented in peace time. So far government spending has just managed to keep the economy afloat but output is yet to catch up with pre-pandemic levels. Moreover the pace of recovery is unlikely to be sustained as fiscal spending is set to decrease dramatically from 2022 onwards. At most, thus, the output surplus is likely to reach 3 per cent – a level perhaps not seen since the early 1980’s, but still unlikely to de-anchor long term inflation expectations beyond current levels.

The second source of inflation anxiety is money supply. Growth across short-term deposits and cash (M1) as well as longer-term deposits (M2) has dwarfed pretty much any period since the Second World War. However, that’s no reason to panic. The correlation between money supply and inflation has been extremely low over the last 40 years.

Furthermore, the growth in monetary aggregates has been accompanied by a collapse in money velocity, or the rate at which money is exchanged in the economy. This is a consequence of the pandemic: both businesses and consumers continue to prefer to hold large sums of cash, which we believe are unlikely to be put to use in the economy in their entirety. (US households, for example, plan to spend just 25 per cent of their latest stimulus cheques; with the rest either saved or used to pay down debt, according to a New York Fed survey.)

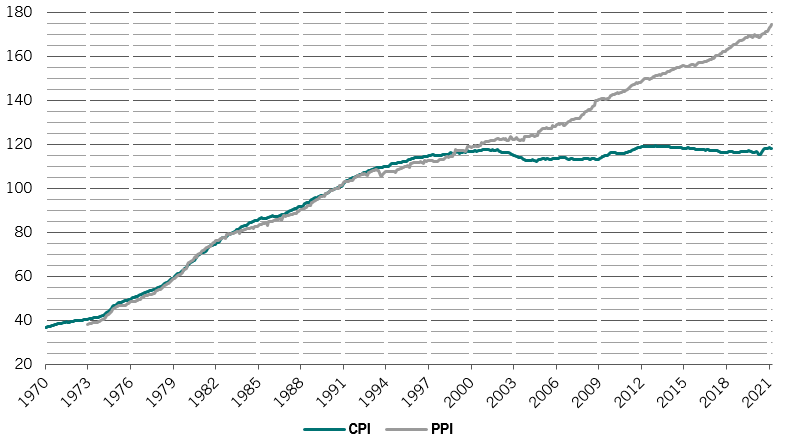

Surging commodity prices are also feeding concerns about inflationary pressures. These were key sources of inflation in the 1980s and early 1990s. Since then, the correlation between the producer prices for goods and those charged to consumers has broken down (see chart) as the importance of goods prices in consumer inflation in general has declined in favour of services. So it is by no means a given that inflation in commodities and other raw materials is going to automatically translate to higher consumer prices.

Source: Pictet Asset Management, Minack Advisors. Data as of March 2021.

Whatever “should” happen to growth and inflation, Covid remains a major uncertainty that could yet upend the consensus view. Another unknown are US tax hikes, which could potentially dampen some of the inflationary pressures.

All told, that makes accurate forecasts very difficult. Broadly, there are three main scenarios:

Same old, same old scenario – A repeat of what we have seen in the last decade, with monthly consumer price increases averaging 0.1-0.14 per cent, meaning that US inflation would still be below the US Federal Reserve’s 2 per cent target level in two years’ time. In this scenario, longer maturity US Treasuries and developed market high grade credit should outperform. The dollar could depreciate significantly, which would benefit emerging market (EM) local currency debt. The asset class is currently pricing in a major inflation overshoot in the developed world. If that does not happen, the medium and long maturity bonds in these markets should rebound.

Fed scenario – The US central bank sees inflation averaging 0.2 per cent per month. That would only get inflation to the 2 per cent target by July 2023, with a possible eventual overshoot to around 2.5 per cent thereafter. This scenario is pretty much in-line with current market positioning, but we would expect a continuation of the compression trade, in other words one that sees high yield credit and EM hard currency debt outperforming, EM corporate bonds doing quite well and some European peripheral debt outperforming German bunds. The dollar should also hold up well, supported by unusually high fiscal spending in the US versus the rest of the world.

Inflation scare – The high inflation scenario sees it rising by on average 0.25 per cent per month. Inflation may then start to move beyond the Fed’s comfort zone and, if it reaches around 3 per cent, the central bank may feel the need to slam on the brakes and hike rates aggressively. The last thing the Fed wants to do is to de-anchor inflation expectations – it has enough credibility to afford a small overshoot and then just for a limited period of time. Since inflation expectations have been steadily anchored at around 2 per cent, the correlation between bond yields and stocks has been positive which allows the Fed to control conditions with only small tweaks limiting the amount of uncertainty and volatility that it adds to the markets. This is something that has been earned through many years of credible inflation-targeting policy and we doubt the Fed would want to risk that.

Our base case scenario lies somewhere between one and two, with the third scenario representing a not-insignificant tail risk. This is where we are using some hedging positions.

Chinese renminbi bonds are a particularly interesting option in this respect. China wants to establish the renminbi as a stable alternative to the dollar, so we would think renminbi bonds could be a very good diversifier against this inflation scare scenario in the rest of world. Recent flows data suggests that it’s a trade that is already quite popular, but we still think China is ahead of the cycle versus the rest of world; its credit markets are showing a tightening of conditions – trends from which renminbi bonds should continue to benefit over the medium term.

Commodity currencies2 should also hold up well in case of an inflation scare, as should curve flattening positions and medium-maturity inflation-linked bonds in the US (TIPS). The overall mood will likely be risk-off, which should support the dollar.

Whatever happens to inflation, we believe there are enough dislocations in global bond markets to generate attractive real returns over the coming years. Uncertainty brought by the pandemic and unorthodox fiscal and monetary policies is here to stay. The key is to identify the risks and the opportunities and balance your portfolio between the scenarios.

read more about our approach to absolute return fixed income

Andres Sanchez Balcazar joined Pictet Asset Management’s Fixed Income team in 2011 and is Head of Global Bonds. Before joining Pictet, he was a senior portfolio manager for Western Asset Management Company LTD for six years. During this time he was responsible for global, European and absolute return fixed income portfolios. Previously, he worked for five years as a global and European portfolio manager with Merrill Lynch Investment Managers. Andres started his career in 1997 at Banco de la Republica de Colombia, where he provided macroeconomic analysis on the US, Europe and Japan. Andres holds a degree in Economics from Universidad de los Andes and a Master's in Management from HEC Paris. He is also a Chartered Financial Analyst (CFA) charterholder.

Share this article

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user navigation and to collect statistical data. To refuse the use of cookies, change your settings or for more information, please click on the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.