investment opportunities in short-term investment grade credit

April 2020

Marketing Material

Defensive investments, redefined

Money market funds are a good option for investors seeking to shore up their defences. Here’s why combining them with short-term investment grade bonds might be a shrewder move.

Written by

Raymond Sagayam

Chief Investment Officer - Fixed income

Stéphane Rüegg

Head of Product Management and Development

Share this article

It’s a perfectly rational move.

As the economy grinds to a halt with around a third of the global population in lockdown, investors of all stripes – whether they’re corporate treasurers, pension managers or insurers – are building up holdings of safe assets.

Their main priority – as is often the case whenever the financial skies darken – is the return of capital rather than the return on it.

The default option for the defensive-minded is money markets. And for good reason. The closest thing to cash, money market funds invest in liquid government and quasi-government instruments that hold their capital value. Such funds are also among the most tightly regulated of all investment vehicles.

For all their advantages, though, money market funds require investors to make a hefty sacrifice: yield. With official interest rates across the developing world close to – and in some cases, below – zero, the return on cash-like securities trails inflation. Custody charges are an additional cost, further eroding the value of capital invested.

In many cases, this is a price worth paying for security.

Yet for investors that still require regular income, money markets funds are no panacea. This is where a complementary allocation to short-maturity investment grade corporate bonds might help.

Although less liquid and more volatile than cash, high-grade, short-maturity corporate bonds1 compare favourably to money markets on several fronts.

To begin with, they offer a yield that provides more than sufficient compensation for the additional risks they carry.

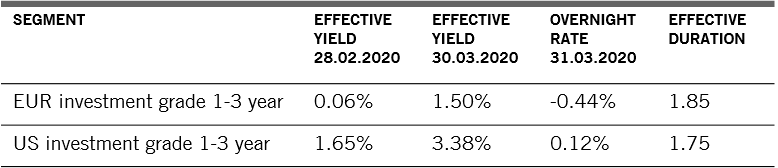

Indeed, compared to cash, shorter maturity bonds are as cheap as they have been in many years (see table).

Big moves in valuation

Yield moves in US and European short-term credit

Source: Pictet Asset Management, Refinitiv

Perhaps the most glaring testament to the market’s detachment from fundamentals is an unusual shift in the shape of the yield curve. An incongruity that has emerged in the wake of the coronavirus-inspired sell-off, yields on short-term corporate bonds have climbed sharply above those offered by longer-maturity debt.

This inversion, which has occurred in both US and European markets, has in part been caused by investors selling their most liquid bonds simply to raise cash.

But an inverted curve is increasingly at odds with fundamental trends.

Normally, when yields on longer-dated corporate bonds are below those of shorter-dated securities, it suggests companies might struggle to service their debts – and in as little as a few months. The last time the curve inverted in the same way was in 2009, during the depths of the sub-prime mortgage crisis.

But just as a wave of defaults didn’t materialise then, there is little to indicate investment-grade companies will find themselves in severe financial difficulty this time round, either.

The main reason is ample monetary stimulus.

In recent weeks, both the US Federal Reserve and the European Central Bank have unveiled unprecedented measures to stabilise corporate lending and protect otherwise sound businesses from the damage caused by the coronavirus.

According to our calculations, some 50 to 60 per cent of US short-maturity corporate bonds and about 25 per cent of their European equivalents are eligible for purchase under central banks’ extended quantitative easing programmes.2

Having both the Fed and ECB as buyers of last resort offers prospective bond investors an additional benefit – lower volatility. Indeed, the volatility of shorter-dated bonds – never high in the first place – could fall below the historic norm over the next few years. That can only enhance their defensive qualities.

Another advantage that corporate debt enjoys over money markets is the variety of investments available. Companies issuing short-maturity debt operate across all major industries – including ‘defensive sectors’ such as health care, telecommunications and utilities, which tend to do well when economic conditions are weak. In both the US and Europe, health care, telecom, utility and consumer staples firms account for around a fifth of the bond market.3

For Europe-based corporate treasurers and insurance firms, short-term corporate bonds have an added attraction. The investible universe has suddenly expanded.

For the first time in years, non-US investors can buy US fixed income assets and hedge any unwanted exposure to the US dollar at a favourable price. That’s because the cost of the currency hedge has fallen steeply. As the Fed has cut rates more aggressively than the ECB, the cost of insuring against unwanted swings in the dollar-euro exchange rate has plummeted, taking the hedged US bond yield – the yield after the hedging cost – into positive territory. (Click here for more on the mechanics of currency hedging.)

None of this is to say that short-term corporate bonds should be considered a cash substitute. Lending money to companies – even for short periods – is inherently riskier than lending to governments in the developed world.

Nevertheless, for investors that need income and whose time horizons stretch to one to three years, short-term corporate debt can be a valuable addition to a ‘defensive’ allocation.

Raymond Sagayam joined Pictet Asset Management in 2010 as Head of Total Return Fixed Income. In January 2017 he was appointed Chief Investment Officer of Fixed Income.

Before joining Pictet, Raymond was a Managing Director with Swiss Re Asset Management, head of dollar and euro investments, focusing on credit relative value strategies. Before that, he worked for Bank Brussels Lambert (ING) trading US Credit. He has traded credit across all major geographies and began his career at ING Barings in Emerging Markets in 1997.

Raymond holds a Bachelor's in Economics from the London School of Economics & Political Science (LSE) and Master's in Contemporary Theology in the Catholic Tradition from Heythrop College, University of London. He is also a Chartered Financial Analyst (CFA) charterholder.

About

Stéphane Rüegg

Stéphane Rüegg is Head of Product Management and Development. He joined Pictet Asset Management in 2013 as a Client Portfolio Manager in the Fixed Income team, covering European credit investment grade and high yield.

Before joining Pictet, he was a client portfolio manager with Amundi in Singapore and Paris. Stéphane started his career in 1999 as fixed income risk manager at Credit Agricole Indosuez. From 2004 to 2008 he was head of risk control of the global fixed income team at Amundi in London.

Stéphane holds a Master’s degree in Business Administration from Ecole supérieure de commerce de Paris and a master in political sciences from Institut d'études politiques de Paris.

Share this article

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user navigation and to collect statistical data. To refuse the use of cookies, change your settings or for more information, please click on the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.