EM Monitor - Emerging markets' response to the economic crisis

April 2020

Marketing Material

QE in emerging markets - A new era?

In the face of the current economic crisis, emerging markets (EM) are turning to QE for the first time. Our economists look at the measures announced so far and the associated risks.

Written by

Anjeza Kadilli

Senior Economist

Kiran Nandra

Head of Emerging Market Equities Management

Share this article

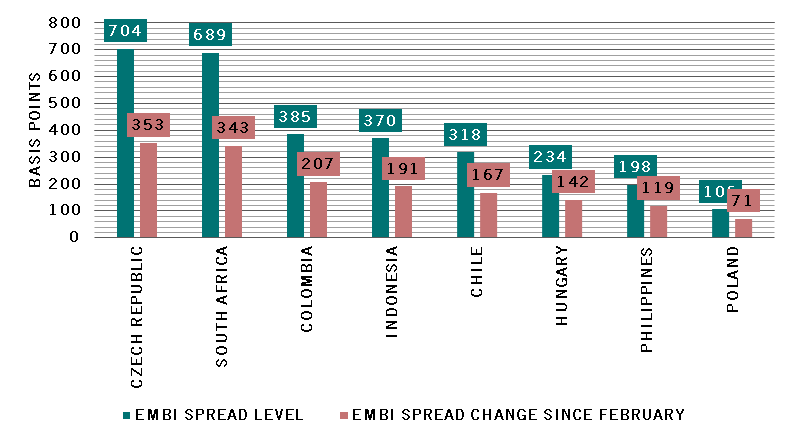

One of the effects of the Covid-19 crisis on EM economies has been the sharp rise in credit spreads (See Fig. 1). Central banks have reacted with the introduction of different measures, including QE, which is unprecedented for EM.

Widening EM spreads shows the magnitude of the shock

Fig.1 - EMBI spread level and change since early February (basis points)

Source: Pictet Asset Management, Bloomberg, data as at 08.04.2020

EM central banks stepping into unchartered territory

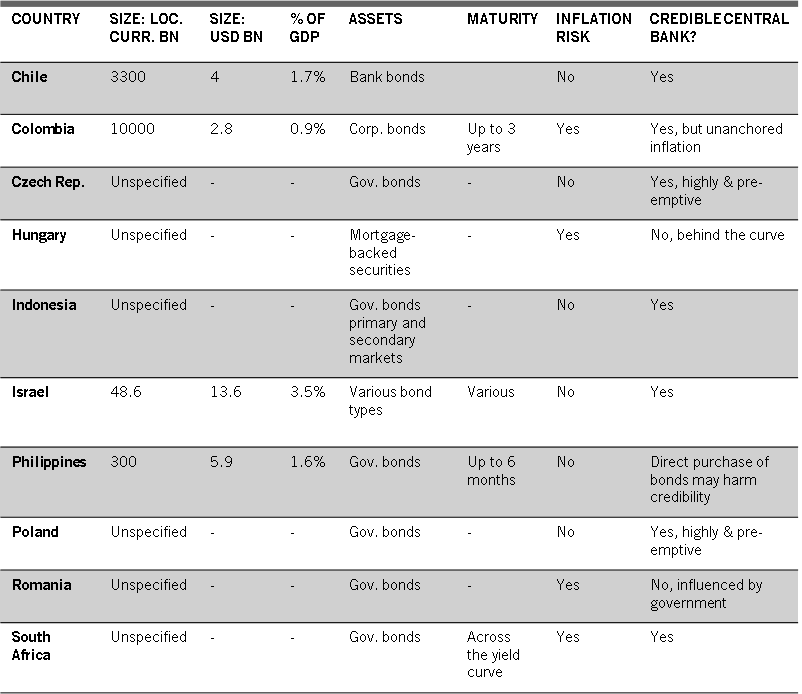

Chile, Colombia, the Czech Republic, Hungary, Indonesia, Israel, the Philippines, Poland, Romania and South Africa have announced QE measures to tackle the current economic crisis (see Fig.2).

Others are considering similar measures. In Brazil, it requires a modification of the country’s constitution, illustrating the exceptional character of these measures in the EM space.

EMs announcing diverse QE programmes

Fig.2 - Summary of QE programmes in Emerging Markets

Source: Pictet Asset Management, relevant central banks’ websites, 08.04.2020

What makes EM QE different?

In developed economies, QE has been used as a tool to lower the cost of funding once conventional tools were exhausted.

While the amounts are limited, the symbolic is strong

In EMs by contrast, the objective of the measures is to improve liquidity and keep markets functioning. The amounts associated to EM QE programmes so far remain limited, especially relative to GDP, but the symbolic of these measures is strong.

In the current scenario, most of the countries will combine QE with conventional tools.

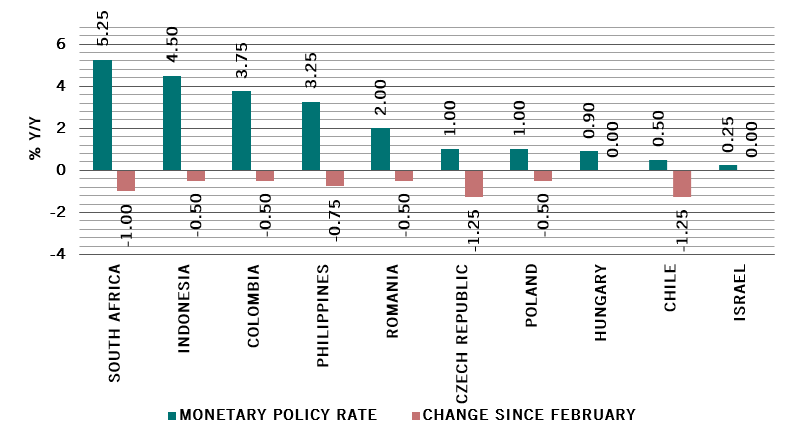

QE used in conjunction with policy rate cuts

Most EM central banks have already cut their policy rates (see Fig. 3).

EM central banks cut rates by up to 1.25% since February

Fig.3 – Monetary policy rate and change since early February

Source: Pictet Asset Management, Refinitiv, CEIC, Bloomberg; data as at 08.04.2020

Additional measures & the Philippines example

Additional measures include targeted longer-term refinancing operations, a cut of the reserve requirement ratio and other tools to improve liquidity.

The Central Bank of the Philippines is a good example. After two rate cuts of 25 and 50 basis points in February and March respectively, it announced a repurchase agreement of government bonds from the Treasury. It also slashed the Reserve Requirement Ratio (RRR) for universal and commercial banks from 600 to 400 basis points. It is exploring a similar cut for other banks and financial institutions. It has also remitted PHP 20 billion as advanced dividend to the central government to fight Covid-19.

QE in Emerging Markets – Testing central banks’ credibility

The new QE programmes will test the faith investors already have in central banks.

Beyond the objectives of helping the smooth functioning of markets, maintaining liquidity, reducing financing cost for governments and firms and helping raise inflation if appropriate (which is not the case for most), EM central banks are exposing themselves to a real test of credibility.

The first test will be to clarify the size and duration of these QE programmes, which are rarely specified.

The first test for central banks will be the definition of clear conditions.

Their credibility will also depend on their independence from governments.

QE will likely lead to inflationary pressures where measures are financed by money printing and long-lasting. It could also lead to an artificial increase in asset prices, beyond those assets targeted by the measures. Here again central banks will need to demonstrate careful management of these side effects.

One advantage for EMs is that QE is more efficient if the policy rate is not in the zero-lower bound, which is the case for most as illustrated in Fig. 3.

Drastic times call for drastic measures. In response to the Covid-19 crisis, EMs are introducing QE measures for the first time. These present short-term benefits but also long-term drawbacks if not well managed. They will be a real test of central banks' credibility.

THE VIEW FROM OUR EMERGING MARKETS EQUITY TEAM

By Kiran Nandra, Senior Product Specialist

Like the EM central banks referred to in the above section, the Reserve Bank of India (RBI) has announced a 75 bps rate cut, a temporary moratorium on loan repayments and a cut in the RRR.

But can the RBI do more if needed?

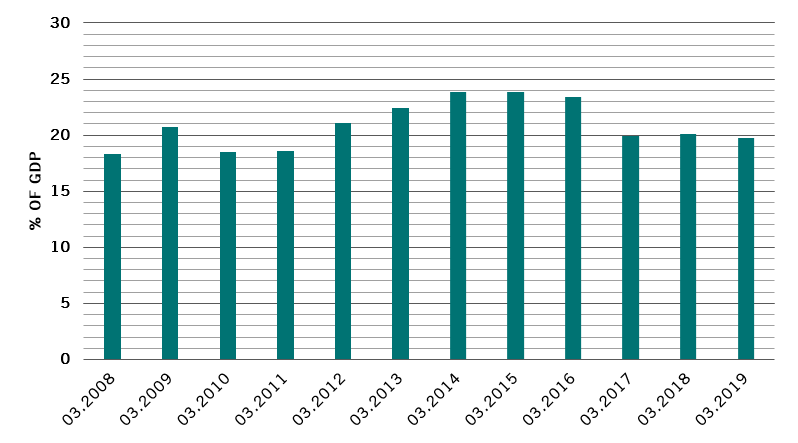

We believe the answer is yes. There’s often a balancing act between QE and the currency. In India’s case, the rupee has held up relatively well, which is good news given EMs' historical reliance upon dollar-denominated debt. What’s more, India is minimally exposed on this front with a highly manageable external debt/GDP ratio of c. 20 per cent (see chart below).

Our focus remains on companies with strong fundamentals. The recent sell-off and uncertainty are also providing opportunities, such as consumer names which have historically been too expensive but that now look attractive.

Anjeza Kadilli joined Pictet in 2015. She is an Senior Economist in Pictet Asset Management’s Economic Analysis team where she conducts macroeconomic analysis of emerging markets. Anjeza holds a PhD in Econometrics from the University of Geneva - where she also obtained an MSc and BSc in Economics. During her PhD, Anjeza spent time at the University of Southern California, Riksbank and HEC Montreal as a visiting scholar.

About

Sabrina Khanniche

Sabrina Khanniche joined Pictet Asset Management in 2011. She is a Senior Economist, Lead on Eurozone and MEA.

Before joining Pictet, she was with Groupama Asset Management during four years as a Financial Engineer in charge of the analysis and modelling of hedge fund risks. In this regard, she published and presented her work in international academic conferences.

Sabrina holds a Master and a PhD in Economics from the University of Paris West Nanterre La Défense.

About

Nikolay Markov

Nikolay Markov joined Pictet Asset Management in 2013. He is a Senior Economist, Lead on CEE and Other advanced economies.

Before joining Pictet, he was working in the Monetary Policy Analysis Unit of the Swiss National Bank where he performed research on monetary policy rules for Switzerland. Prior to working at the Swiss National Bank he was a teaching and research assistant at the University of Geneva and participated in international academic conferences.

Nikolay holds a PhD in Economics from the University of Geneva and obtained a PhD program certificate from the Swiss National Bank doctoral institute in Gerzensee.

About

Lola Saugy

Lola Saugy joined Pictet Asset Management in 2018 as part of the firm’s Graduate Programme. She is now a Quantitative Economic Analyst within the Economic Analysis team in Geneva. Lola holds a Master of Science in Applied Mathematics from the Ecole Polytechnique Fédérale de Lausanne. She did her master thesis at Harvard University in the field of biostatistics, as a visiting scientist.

About

Kiran Nandra

Kiran Nandra joined Pictet Asset Management in 2016. She is the Head of EM Equities Management and Senior Client Portfolio Manager for the Emerging Equities team.

Previously, Kiran worked at Wellington Management where she was most recently a Portfolio Specialist.

She joined Wellington in 2003 in a Relationship Management role before becoming a Research Analyst covering European and Latin American banks.

Kiran graduated from University College London with an LLB (Honours) degree in Law and has an MBA from The University of Chicago Booth School of Business.

Share this article

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user navigation and to collect statistical data. To refuse the use of cookies, change your settings or for more information, please click on the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.